Download

1 / 20

200 likes | 526 Views

Utility Tariff Bonds. NARUC Accounting and Finance Meeting Sharon Bonelli, Managing Director October 10, 2007 Jackson Hole, WY. What is Securitization?. A form of debt financing that involves: Legally isolating a pool of financial assets

E N D

Utility Tariff Bonds NARUC Accounting and Finance Meeting Sharon Bonelli, Managing Director October 10, 2007 Jackson Hole, WY

What is Securitization? • A form of debt financing that involves: • Legally isolating a pool of financial assets • Repackaging the asset cash flows into a liability structure • Creating securities that are backed by those assets • Providing for loss protection on those assets • Selling the securities to investors in the capital market • Common securitization asset classes: CMBS, RMBS, CDO, ABS www.fitchratings.com

Utility Tariff Bonds Defined • Bonds backed by “tariff property” which represents the right to collect a per kilowatt-hour tariff from a utility’s retail electric customers • Tariff property is established to fund a specific purpose, ie. costs to transition to a competitive market, environmental projects, etc. • The tariff property is a future flow (a “regulatory asset”), reflecting revenues from future customer billings • Bond structure incorporates conventional securitization features and additional features based on unique nature of the collateral www.fitchratings.com

Conventional ABS vs. Utility Tariff Bonds * Credit cards, auto loans, student loans, etc. www.fitchratings.com

Transaction structure www.fitchratings.com

Corporate Bonds vs. Utility Tariff Bonds www.fitchratings.com

Environmental projects Monongahela Power Co./Potomac Edison Co. (2007) Wisconsin legislation passed Louisiana legislation passed Hurricane recovery costs Florida Power & Light Co. (2007) Entergy Gulf States Inc. (2007) Cleco (expected 2007) Any utility purpose - Idaho legislation passed Bankruptcy reorganization Pacific Gas and Electric Co. (2005) Tariff Bond Structure Adaptable to New Applications www.fitchratings.com

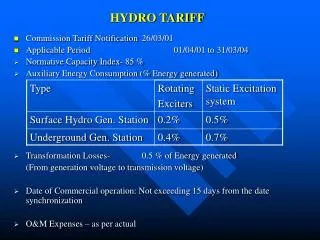

Tariff Bond Market Characteristics • Fitch has rated $39.8 billion of utility tariff bonds since 1995 (99% of issuance volume) • 40 transactions currently outstanding • Since late July, secondary bond spreads have been widening across the ABS market more than traditional high grade utility bond market, including tariff bonds • Will the historically wider cost differential between ‘AAA’ utility tariff bonds relative to on-balance sheet utility debt return in the near term? www.fitchratings.com

Tariff Bond Spreads vs. ‘BBB+’ Corporate Bonds www.fitchratings.com

Tariff Bonds Have Stable Performance to Date • Tariff bonds are performing as expected • ‘AAA’ affirmed on all 40 rated transactions in August 2007 • Shortfalls mainly attributed to weather variance with true-ups effectively adjusting collections • Uninterrupted collections during servicer bankruptcies (NorthWestern, PG&E) www.fitchratings.com

ABS Tariff Bond Rating Criteria – Six key areas of focus • Legal and regulatory framework • Transaction structure • Utility as servicer • Credit analysis • Self-generation and alternate technologies • Cash flow models and stress cases www.fitchratings.com

Rating Criteria: Legal & Regulatory Framework • Tariff established as a property right by law and regulatory order • Tariff established as irrevocable; state nonimpairment pledge • Nonbypassability • Legal true sale & bankruptcy remote issuer • Successor servicer provisions • True-up: annual, interim, nonstandard • Third party energy providers • Perfected, first priority lien in transition property granted to indenture trustee www.fitchratings.com

Rating Criteria: Transaction Structure • Time-tranched notes • Principal amortization schedule • Credit enhancement • True-up • Capital subaccount • Reserve subaccount • Overcollateralization subaccount www.fitchratings.com

Rating Criteria: Servicing • Consumption forecasting • Customer credit evaluation process • Collections policies • Billing and remittance procedures • Commingling of funds • Successor servicer www.fitchratings.com

Rating Criteria: Credit Analysis • Customer base • Concentrations • Historical performance • Cyclical & seasonal patterns; consumption variance • Tariff level • Self generation & alternate technologies • Cash flow analysis • ‘AAA’ stress case • Break-the-Bond stress case www.fitchratings.com

Tariff Bond Use Impact on Utility Corporate Credit www.fitchratings.com

Adjustments to Financial Statements for Tariff Bonds • Fitch’s power team adjusts financial statements to deconsolidate tariff bond debt related cash flows in its utility rating analysis, as follows: • Subtract interest and principal payments on tariff bonds from revenue line item • Add principal payment to depreciation and amortization line item • Add interest payment to interest expense line item • Subtract tariff bond debt from long term debt and current portion of long term debt on the balance sheet www.fitchratings.com

Related Research • “Rating Criteria for U.S. Utility Tariff Bonds”, August 30, 2007 • “U.S. Utility Tariff Bonds: Adaptability of an Asset Class,” Aug. 30, 2007 www.fitchratings.com