Download

1 / 2

20 likes | 73 Views

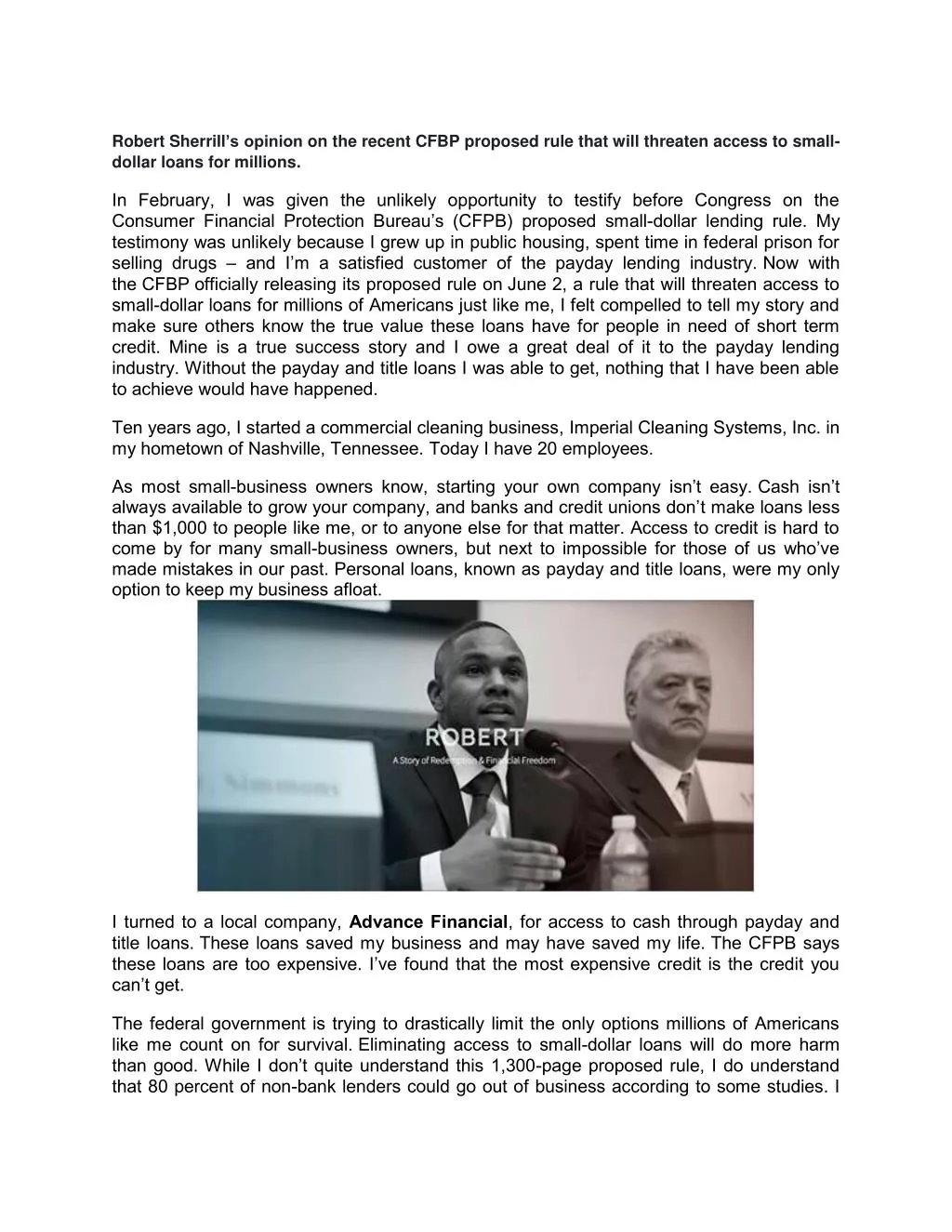

One of our AF247 former customers, Robert Sherrill, was recently featured in an article for The Hill.

E N D

Robert Sherrill’s opinion on the recent CFBP proposed rule that will threaten access to small- dollar loans for millions. In February, I was given the unlikely opportunity to testify before Congress on the Consumer Financial Protection Bureau’s (CFPB) proposed small-dollar lending rule. My testimony was unlikely because I grew up in public housing, spent time in federal prison for selling drugs –and I’m a satisfied customer of the payday lending industry. Now with the CFBP officially releasing its proposed rule on June 2, a rule that will threaten access to small-dollar loans for millions of Americans just like me, I felt compelled to tell my story and make sure others know the true value these loans have for people in need of short term credit. Mine is a true success story and I owe a great deal of it to the payday lending industry. Without the payday and title loans I was able to get, nothing that I have been able to achieve would have happened. Ten years ago, I started a commercial cleaning business, Imperial Cleaning Systems, Inc. in my hometown of Nashville, Tennessee. Today I have 20 employees. As most small-business owners know, starting your own company isn’t easy.Cash isn’t always available to grow your company, and banks and credit unions don’t make loans less than $1,000 to people like me, or to anyone else for that matter. Access to credit is hard to come by for many small-business owners, but next to impossible for those of us who’ve made mistakes in our past. Personal loans, known as payday and title loans, were my only option to keep my business afloat. I turned to a local company, Advance Financial, for access to cash through payday and title loans. These loans saved my business and may have saved my life. The CFPB says these loans are too expensive. I’ve found that the most expensive credit is the credit you can’t get. The federal government is trying to drastically limit the only options millions of Americans like me count on for survival. Eliminating access to small-dollar loans will do more harm than good. While I don’t quite understand this 1,300-page proposed rule, I do understand that 80 percent of non-bank lenders could go out of business according to some studies. I

also understand that our communities will suffer and people like me will have nowhere to go for accessible credit. What about my privacy? The CFPB wants to put my records in a government database for a mere $200 loan. Why should I and the people like me be singled out? The payday loans I have gotten are quick, easy and confidential. The CFPB intends to strip all of that away. In March, I also testified before Congress about my experience with the payday loan industry. I sat next to a CFPB representative who admittedly had never even been inside a payday loan store. The CFPB claims to be a “21st-century data driven agency” looking to take a “market based approach” to regulation. When I think of a “market based approach” in my business, I think about talking to the customers and finding out what they want. That’s how I effectively meet the needs of my business. Maybe the CFPB should talk to people like me who are being served in this market. Let me assure you, the individuals who frequent those stores often struggle to make ends meet, but they don’t need the government to make that struggle even more difficult. Any Member of Congress needs to understand the impact this will have on their constituents. You want to take their only option for credit away from them? They will find a way to fill the need. As I said when I testified, “If you don’t have it, you need to go out and get it.” Without companies that are licensed, we will be forced to go to an unregulated lender, or back on the streets. Robert Sherrill is a minority business owner and the CEO of Imperial Cleaning Systems, Inc. in Nashville, Tennessee. Source: http://thehill.com/blogs/congress-blog/economy-budget/286718-what-payday-loans-mean-to- me