Download

1 / 17

170 likes | 421 Views

Current Asset Management (Chapter 7) (Chapter 6 – pages 143 – 145). Working Capital Management Current Asset Investment Policy Temporary and Permanent Current Assets Zero Working Capital Cash Management Marketable Securities Accounts Receivable Management Inventory Management.

E N D

Current Asset Management(Chapter 7)(Chapter 6 – pages 143 – 145) • Working Capital Management • Current Asset Investment Policy • Temporary and Permanent Current Assets • Zero Working Capital • Cash Management • Marketable Securities • Accounts Receivable Management • Inventory Management

Working Capital Management: An Overview • Gross Working Capital -(Current Assets) • New Working Capital - (Current Assets - Current Liabilities) • Working Capital Management • Involves investing in current assets and financing of current assets:

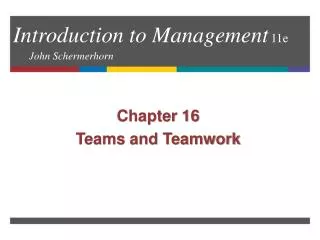

Current Asset Investment Policy • Everything else remaining the same, higher levels of current assets mean lower risk and lower expected return • Lower Risk • Greater ability to meet short-run obligations. • Lower Return • Cash and marketable securities typically yield low returns. Furthermore, when current assets are increased, additional financing costs will be incurred thereby lowering returns. • Lower levels of current assets result in opposite effects.

Alternative Current Asset Investment Policies Current Asset (millions of $) Conservative - low risk Moderate Aggressive - high risk Sales (millions of dollars)

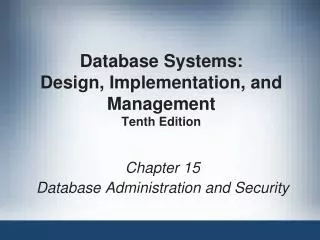

Temporary vs. Permanent Investmentin Current Assets • Temporary Investment - Commonly, firms experience short-run fluctuations in current assets. For example, retail department stores will have high levels of inventory around Thanksgiving. In January, the inventory should be low. • Permanent Investment - Firms always have some minimum level of investment in current assets (i.e., a permanent investment). As a firm grows over time, the level of permanent current assets also grows (e.g., a supermarket chain with 70 stores will have more permanent inventory than a chain with 4 stores).

Temporary and Permanent Current Assets Millions of dollars Temporary Fluctuations in Current Assets Permanent Current Assets Time Period

Cash Management: An Overview • Beginning Cash Balance + Cash Inflows - - - Speed Up - Cash Outflows - - - Slow Down = Ending Cash Balance - Desired Cash Balance = Surplus or Shortage • If Surplus: Pay off short-term debt or buy marketable securities • If Shortage: Short-term borrowing or sell marketable securities

Desired Cash Balance: • Precautionary Demand - Satisfy possible, but as yet indefinite cash needs. • Speculative Demand - Build up current cash balances in anticipation of future business costs being lower. • Risk Preferences • Compensating Balances • Transactions Demand - Cash needs arising in the ordinary course of doing business.

Float • Much of cash management is oriented towards managing the float. • Mail Float • Time lapse from the moment a customer mails a remittance check until the firm begins to process it. • Processing Float • Time required for the firm to process remittance checks before they can be deposited in the bank.

Float (Continued) • Transit Float • Time necessary for a deposited check to clear through the commercial banking system and become usable funds to the company. • Disbursing Float • Funds available in the firm’s bank account until its payment check has cleared through the system.

Electronic Funds Transfer • Substantially reduces float • Some Examples: • Automated teller machines • Direct deposit of payroll checks • Paying the supermarket and others with bank cards.

Lock-Box System • Customers mail remittance checks to P.O. Box. • Local bank processes and deposits checks directly into the company’s account. • Reduces mail and processing float. • Also reduces transit float if lock-box is located near Federal Reserve Bank or branches.

Marketable Securities • The marketable securities portfolio is typically used for temporary investments of excess cash, or as a substitute for cash (i.e., near cash). Therefore, securities in the portfolio are generally safe, short-term, and highly liquid. • Treasury Bills • Short-term obligations of the federal government with maturities of 91 days to a year. They are traded on a discount basis in bearer form. Not taxable at state and local levels, but taxable at the federal level. • Commercial Paper • Unsecured promissory notes issued by large corporations in amounts of $25,000 or more (No active secondary market).

Marketable Securities Continued • Negotiable Certificates of Deposit (CDs) • Offered by financial institutions (e.g., banks, S&Ls). Those big business is interested in have $100,000 minimums. • Banker’s Acceptance: Generally arise out of foreign trade. • Importer (buyer) issues a promise to pay a certain amount to the exporter (seller). • A bank accepts the promise, and commits itself to pay the amount when due. • Exporter (seller) can now sell this acceptance in the marketplace at a discount (a price that is less than the promised amount).

Accounts Receivable Management • Major Decisions • Credit Standards • Credit Terms • Collection Policy • Credit Standards: Will they pay as agreed? • Credit Scoring • Credit Reports • Past Experience • Financial Analysis • Debt Ratios, Liquidity Ratios, Profit Ratios

Accounts Receivable Management(Continued) • Credit Terms • Example: 2/10, net 30 • Collection Policy • Standard Operating Procedures • Be professional, firm, and do not bluff. • Vary procedures with slow payers. • Evaluating Collection Efforts • Average Collection Period, Bad Debt to Sales Ratio, Aging Accounts Receivable, Receivables to Assets Ratio, Credit Sales to Receivables Ratio.

Inventory Management(Covered in Detail in Production Management) • Basic Costs Associated With Inventory • Carrying Costs • storage, insurance, cost of capital used • Ordering Costs • placing orders, shipping and handling • Costs of Running Short • lost sales, reduced customer goodwill • Objective • Minimize total costs associated with managing inventory.