Download

1 / 1

10 likes | 23 Views

<br>What are your eCheck API requirements? : https://blog.agilepayments.com/what-are-your-echeck-api-requirements<br>If you're part of a SaaS dev team or a stakeholder and have determined that your application has a need for an eCheck API, have you defined your requirements? eCheck transactions, also known as ACH transactions, are a powerful payment modal for many SaaS applications.<br>

E N D

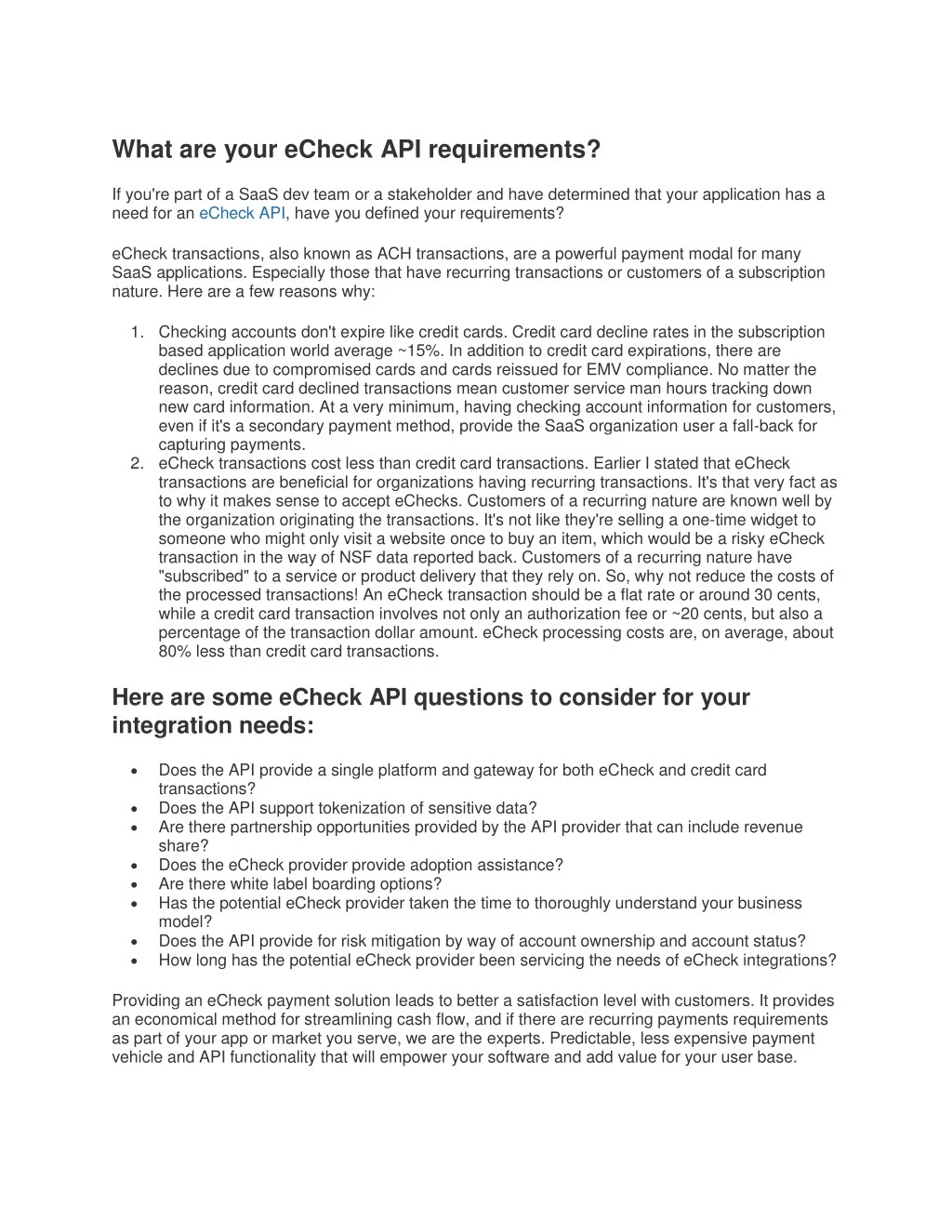

What are your eCheck API requirements? If you're part of a SaaS dev team or a stakeholder and have determined that your application has a need for an eCheck API, have you defined your requirements? eCheck transactions, also known as ACH transactions, are a powerful payment modal for many SaaS applications. Especially those that have recurring transactions or customers of a subscription nature. Here are a few reasons why: 1.Checking accounts don't expire like credit cards. Credit card decline rates in the subscription based application world average ~15%. In addition to credit card expirations, there are declines due to compromised cards and cards reissued for EMV compliance. No matter the reason, credit card declined transactions mean customer service man hours tracking down new card information. At a very minimum, having checking account information for customers, even if it's a secondary payment method, provide the SaaS organization user a fall-back for capturing payments. 2.eCheck transactions cost less than credit card transactions. Earlier I stated that eCheck transactions are beneficial for organizations having recurring transactions. It's that very fact as to why it makes sense to accept eChecks. Customers of a recurring nature are known well by the organization originating the transactions. It's not like they're selling a one-time widget to someone who might only visit a website once to buy an item, which would be a risky eCheck transaction in the way of NSF data reported back. Customers of a recurring nature have "subscribed" to a service or product delivery that they rely on. So, why not reduce the costs of the processed transactions! An eCheck transaction should be a flat rate or around 30 cents, while a credit card transaction involves not only an authorization fee or ~20 cents, but also a percentage of the transaction dollar amount. eCheck processing costs are, on average, about 80% less than credit card transactions. Here are some eCheck API questions to consider for your integration needs: Does the API provide a single platform and gateway for both eCheck and credit card transactions? Does the API support tokenization of sensitive data? Are there partnership opportunities provided by the API provider that can include revenue share? Does the eCheck provider provide adoption assistance? Are there white label boarding options? Has the potential eCheck provider taken the time to thoroughly understand your business model? Does the API provide for risk mitigation by way of account ownership and account status? How long has the potential eCheck provider been servicing the needs of eCheck integrations? • • • • • • • • Providing an eCheck payment solution leads to better a satisfaction level with customers. It provides an economical method for streamlining cash flow, and if there are recurring payments requirements as part of your app or market you serve, we are the experts. Predictable, less expensive payment vehicle and API functionality that will empower your software and add value for your user base.