Download

1 / 13

150 likes | 743 Views

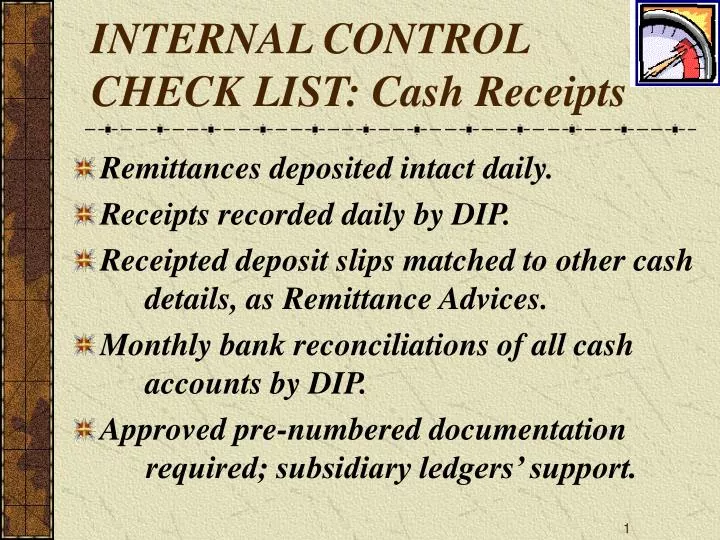

INTERNAL CONTROL CHECK LIST: Cash Receipts Remittances deposited intact daily. Receipts recorded daily by DIP. Receipted deposit slips matched to other cash details, as Remittance Advices. Monthly bank reconciliations of all cash accounts by DIP.

E N D

INTERNAL CONTROL CHECK LIST: Cash Receipts • Remittances deposited intact daily. • Receipts recorded daily by DIP. • Receipted deposit slips matched to other cash details, as Remittance Advices. • Monthly bank reconciliations of all cash accounts by DIP. • Approved pre-numbered documentation required; subsidiary ledgers’ support.

INTERNAL CONTROL CHECK LIST: Cash Receipts • Credit memos & non-cash credits (e.g., bad debt write-offs) properly authorized. • Approved documentation & security codes required for computer inputs to Cash, A/R and Inventory. • Sales Tabulations reviewed, approved, and reconciled to Customer Orders and Unfilled Orders Files, Unbilled shipments. • Cash & Sales Tabulations compared to plans & budgets, etc.

Cash Receipts Audit Objectives • Existence & completeness • Presentation & disclosure • Bank overdrafts • Restricted balances • Compensating balances

Audit Evidence & Procedures for Cash Receipts • Bank confirmation • Bank reconciliation • Cutoff bank statement • Cash receipts cutoff tests • Proof of cash • Analysis of interbank transfers • Vouch receipt before & after year-end

Beware of Kiting! Kiting—recording a bank transfer as a deposit in the receiving bank while failing to show a deduction from the bank account on which the transfer check is drawn.

Warning Signs • Bartered advertising • Inflated sales/fictitious accounts receivable • Inadequate loan loss reserves • Early revenue recognition

Audit Program Summary for Cash Receipts Transactions • Prepare a Proof of Cash for test month(s). • Trace cash receipts from/to A/R subsidiary records, deposit list detail, bank statements, Cash Receipts tabulations. • Tie-in details’ totals to General Ledger. • Test for kiting, lapping, window dressing. • Verify authorizations for non-cash credits to Accounts Receivable. • Write memo with your opinion.

AUDIT PROGRAM: Cash (1/4) • Test prescribed controls for legal, procedural & policy compliances. • Observe counts of all cash funds & signed receipt for same (workpaper in ink); tie-in to G/L. • Prove all Bank Reconciliations for all accounts of the year & tie-in to G/L. • Test mathematics of Reconciliations.

AUDIT PROGRAM: Cash (2/4) • Request cut-off bank statements & compare details to reconciliations. • Test year-end cut-off procedures & consistency with accounts receivable. • Test for inactive accounts, lapping, kiting & window dressing, using Interbank Transfers work papers. • Verify pre-numbering where applicable.

AUDIT PROGRAM: Cash (3/4) • Mail positive confirmations to all banks used during the year. • List and investigate all exceptions. • Tie-in all non-cash details (e.g., notes) to appropriate work papers. • Calculate related accruals. • Consider second, third requests. • Consider an FYE “Proof of Cash.”

AUDIT PROGRAM: Cash (4/4) • Perform analytical procedures & calculate significant ratios, trends. • Scanfor and investigating the unusual. • Analyze for fraud if control absent or weak, or as deemed necessary. • Clear all exceptions; project sampling. • Writea memo with your opinion.

AFTER ALL CAPITONS, the In-charge CPA will… • Review for GAAP consistency and/or violations. • Consider materiality, potential for fraud, misleading data. • Make decisions as to Presentations, Footnotes, Disclosures. • Draft the Audit Report.