Download

1 / 5

50 likes | 64 Views

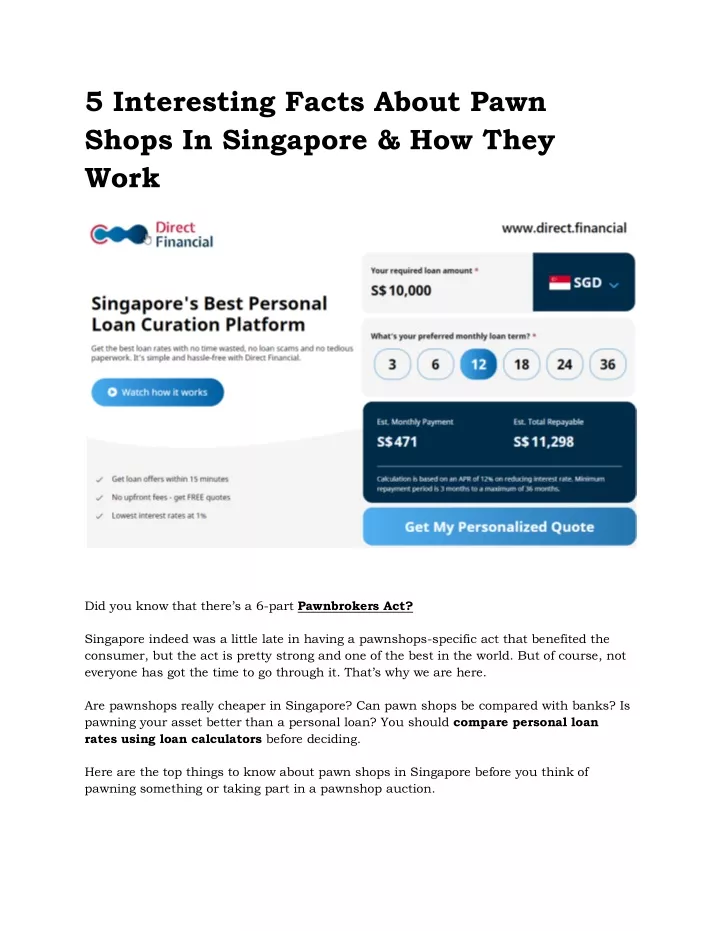

Get the best personal loan rates in Singapore with no time wasted, no loan scams and no tedious paperwork. Personal loan<br>in Singapore simple and hassle-free with Direct Financial.<br>

E N D

5 Interesting Facts About Pawn Shops In Singapore & How They Work Did you know that there’s a 6-part Pawnbrokers Act? Singapore indeed was a little late in having a pawnshops-specific act that benefited the consumer, but the act is pretty strong and one of the best in the world. But of course, not everyone has got the time to go through it. That’s why we are here. Are pawnshops really cheaper in Singapore? Can pawn shops be compared with banks? Is pawning your asset better than a personal loan? You should compare personal loan rates using loan calculators before deciding. Here are the top things to know about pawn shops in Singapore before you think of pawning something or taking part in a pawnshop auction.

Heads up – the ride will be bumpy! Make sure you carefully understand the implications because there’s nothing worse than a nasty shock later such as knowing that you have to pay much more than the loan amount if you delay. 1. Pawnshops do have interest rates Yes, there are fees. You cannot redeem the item you hock at a pawn shop for the same amount you received as a loan. Pawnshops charge an interest. The interest rate is usually 1% for the first month and 1.5% for consecutive months. This interest rate is better than credit cards, which charge starting from 2% but worse than a personal loan – which is typically set at 1%. Note that if you keep something pawned for 6 months, then the total interest you pay becomes 8.5%. You should only pawn something for the short term. The problem comes in when you cannot repay on time. When you miss a repayment, personal loans become your cheaper option. 2. Getting a loan from pawning is much easier Hocking an item in a pawn shop and receiving a loan is much easier and faster than applying for a personal loan or acquiring a loan from a licensed moneylender. There’s also much less paperwork involved –in most cases, you’d only need identification, a good pledge (the item that you pawn or hock), and the original papers of the item being pawned, if applicable. No CPF documents or minimum income hassles. The pawnshop system in Singapore is very conducive as well as accepting of foreigners – who need to have a significantly higher annual income to apply for most credit cards relative to Singaporeans or permanent residents. Pawnshops are a great way to acquire a loan for these people. 3. Here’s what happens if your item goes into auction

So, you couldn’t repay and the item you hocked ended up being in the auction. Assume the pawnshop paid you S$15,000 for a piece of jewellery that you pawned and you failed to repay the amount with interest in the specified time period. The item will now be auctioned off. But what if it fetches more than the amount that was loaned to you? If the jewelry sold for S$18,000, let’s say, then the surplus S$3,000 is yours, after any fees or pending interest payment. That’s the good thing about pawning. Nobody is trying to rip you off even if you don’t have full claim to the item. 4. Buying gold from pawnshops is surprisingly better A goldsmith can be a much costlier option than your local pawn shop in many cases. For example, some pawn shops operate under the Gross Margin Scheme – which means that they don’t have to include GST in the prices of their products. Instead, their GST is based on their total profits. This makes the item’s price cheaper in pawn shops. Apart from that, pawnshops generally charge less than goldsmiths for a variety of reasons. Primary among them is the fact that the gold in pawnshops is secondhand. That might also be a dealbreaker for many. You won’t get the packaging in many cases, for example, which can make things irritating for collectors. But all in all, a pawn shop is a great place to buy gold from. 5. Pawnshops have been accumulating wider social acceptance and penetration Did you notice that pawnshops today look a lot more fancy and eye-catching? There are no more metals bars all around it. Historically, pawn shops in Singapore used to be synonymous with the last resort. You had to be very poor or bankrupt even to go to a pawn shop. It was quite an embarrassing thing not many years ago.

However, pawn shops have shown that they are a great place to get loans and acquire short-term capital from. There’s no shame or guilt. Slowly but steadily, pawn shops have been increasing their acceptance in society. As per government records, as of August 1, 2021, there are 241 registered pawn shops in all of Singapore. You can use the Singapore Pawnbrokers’ Association website to find a pawn shop in your part of the town. You can also use this platform to search by pin code, though their directory doesn’t include all pawn shops. 6. Don’t use pawn shops to sell items Pawnshops are specifically not meant to be used as a liquidation tool. If you have an expensive item, you have two mutually exclusive ways to go about it: 1. Pawn the item in a pawn shop. Get a loan against it. Repay the loan with interest as soon as possible and get your item back. 2. Sell it directly and get the money. Why shouldn’t you use pawn shops are a typical marketplace? Well, you will most definitely get a lower value than the maximum sale value through the right channels. For example, if you wish to sell your gold jewelry then it’s better to consult a goldsmith who will give you better rates, or if you have to sell a watch then consult a used watch buyer for a much better offer. Pawnshops are strictly for acquiring loans against valuable items and repaying said loans. When should you go to a pawn shop? Let’s try to make the picture clearer. You should only go to a pawn shop if your repayment is inconsistent. For example, if you’rebetween jobs or unemployed, or perhaps in a bad financial state lately such that you cannot ensure timely repayments. These are the ideal conditions to consult with a licensed pawnbroker. The biggest loss you can sustain is the loss of the pledge. Let’s create a likely scenario.

You pawn a fancy watch. After 4-5 months, you couldn’t make a single repayment. Your watch is auctioned off. End of the debt. You can always pay off a pawnbroker’s loan with the loss of your pledge. That’s why the loan amount is typically 60-80% of the actual market or sale value of the pawned item because they’re also buying uncertainty. If you are confident of repayments then perhaps it’s better to be a little more patient and acquire a personal loan instead. The only plausible explanation to go for a pawn shop even if you can make repayments on time is if you have a bad credit score – a factor that hardly matters to a pawnbroker. Wrapping up That’s it. Hopefully, you now understand the workings of pawnshops in Singapore. You also know when you should go for a pawnbroker and when not to. Here’s a few questions to run through before finding a pawnshop: Always make sure that you understand the terms of the pawn. For example, what’s the interest rate, and how does it increase over time? What’s the maximum period before your pledge will be auctioned off? It also helps to do a little research on your pledge for the going price at pawn shops before you head out to one. There will be a tad bit of bargaining involved. It helps to know everything about the item you’re about to pawn. It will help you to confidently quote higher and point out the qualities or selling points when bargaining. If you have formal documentation and paperwork, packaging, proof of ownership, or any added document-based perks including warranties then arrange them neatly with the item for a higher loan amount. Well-documented and well-presented items often fetch higher prices, both for the loans and during auctions. Direct Financial hopes that this article has helped you understand more about pawn shops in Singapore. We hope to educate readers more about various financial products and services. Read more about us here.