Download

1 / 3

30 likes | 84 Views

GST- goods and services tax provision requiring transporters to carry an electronic way bill or e-way bill when moving goods between states will be implemented from February 1, to check evasion and boost revenue by up to 20%.

E N D

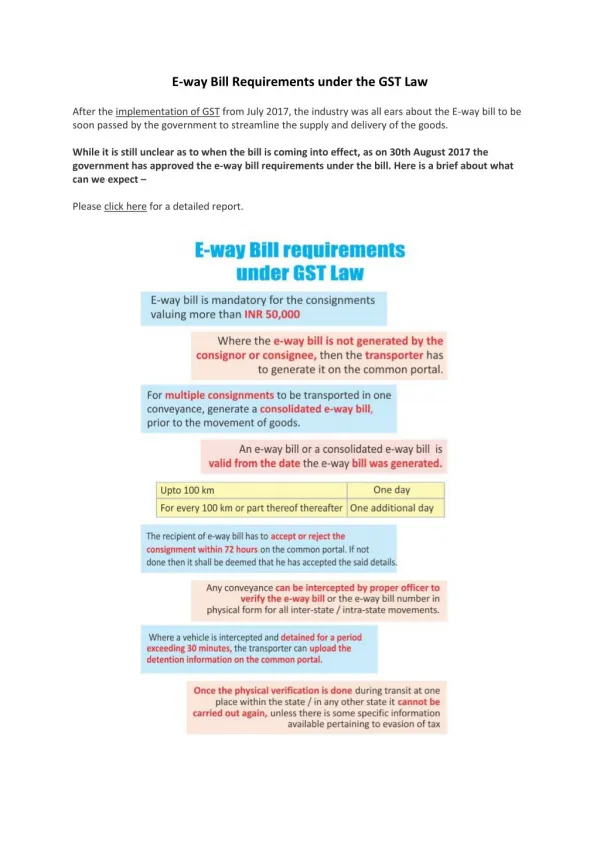

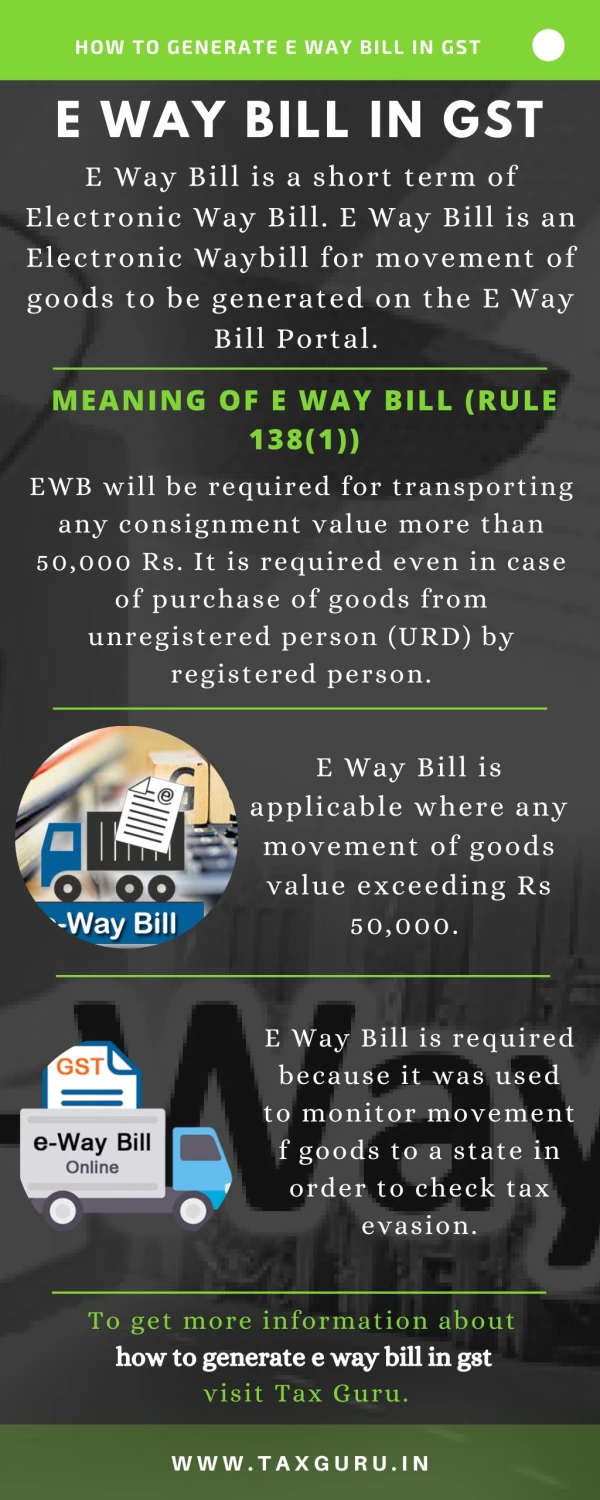

GST E-way Billing system GST- goods and services tax provision requiring transporters to carry an electronic way bill or e-way bill when moving goods between states will be implemented from February 1, to check evasion and boost revenue by up to 20%. After GST implementation from 1st July, the requirement was postponed due to an unready network. This was done even in the 17 states which in the Pre-GST era had an established electronic challan or e-way bill system, a top official said. Once the e-way bill system is implemented, tax avoidance would become difficult, as the government would have details of all goods in transit above the value of Rs 50,000 and could spot a mismatch if either supplier or purchaser does not file tax returns, he said.

The e-way bill for inter-state movement will be implemented from 1st February and for intra-state movement from 1st June. The official said states had been given the option of choosing when they want to implement the intra-state e-way bill between 1st February and 1st June. States had also been given the option to exempt movement of goods within 10 km radius, he said, adding all essential goods have been exempted from the requirement of carrying e-way bill. Besides plugging tax evasion, the e-way bill will boost revenues by 15% to 20%, he said. "The experience of states which had e-way bill system in pre-GST era showed a 15% to 20% rise in revenue," he said. The official said a pilot of e-way bill has been successfully run in Karnataka and the IT system is fully geared to meet any requirement. E-way bill is an electronic way bill for movement of goods which can be generated on the GSTN (common portal). Movement of goods of more than Rs.50,000 in value cannot be made by a registered person without an e-way bill. The e-way bill can also be generated or cancelled through SMS, he said. When an e-way bill is generated, a unique e-way bill number (EBN) is allocated and is available to the supplier, recipient, and the transporter, he added. Who should generate it and why? E-way bill can be generated by the consignor or consignee himself if the transportation is being done in own/hired conveyance or by railways by air or by Vessel. If the goods are handed over to a transporter for transportation by road, the bill will be generated by the transporter. Where neither the consignor nor consignee generates the e-way bill and the value of goods is more than Rs.50,000 it shall be the responsibility of the transporter to generate it. Purpose of e-way bill E-way bill is a mechanism to ensure that goods being transported comply with the GST Law and is an effective tool to track movement of goods and check tax evasion. Validity of e-way bill The validity of e-way bill depends on the distance to be traveled by the goods. For a distance of less than 100 Km the e-way bill will be valid for a day from the relevant date. For every 100 Km thereafter, the validity will be additional one day from the relevant date. The "relevant date" shall mean the date on which the e-way bill has been generated and the period of validity shall be counted from the time at which the e-way bill has been generated and each day shall be counted as twenty-four hours. What if goods cannot be transported within the period? In general, the validity of the e-way bill cannot be extended. However, Commissioner may extend the validity period only by way of issue of notification for certain categories of goods. Further, if under

circumstances of an exceptional nature, the goods cannot be transported within the validity period of the e-way bill, the transporter may generate another e-way bill after updating the details again. Cases where e-way bill is not required According to CBEC, there are some exceptions to e-way bill requirement. It said: "No e-way bill is required to be generated in the cases where goods being transported by a non-motorised conveyance; goods being transported from the port, airport, air cargo complex and land customs station to an inland container depot or a container freight station for clearance by Customs; and when Consignment value is less than Rs.50,000 among others." For more details please visit on: http://cargo365cloud.com/news