Download

1 / 3

0 likes | 6 Views

In New York, navigating the intersection of health insurance and divorce requires careful consideration. Divorce often impacts health insurance coverage, leaving individuals in need of new arrangements. Understanding the legal implications and available options is crucial for ensuring uninterrupted access to healthcare during this transition. From exploring COBRA benefits to assessing eligibility for Medicaid, individuals must proactively manage their health insurance needs amidst the divorce process.

E N D

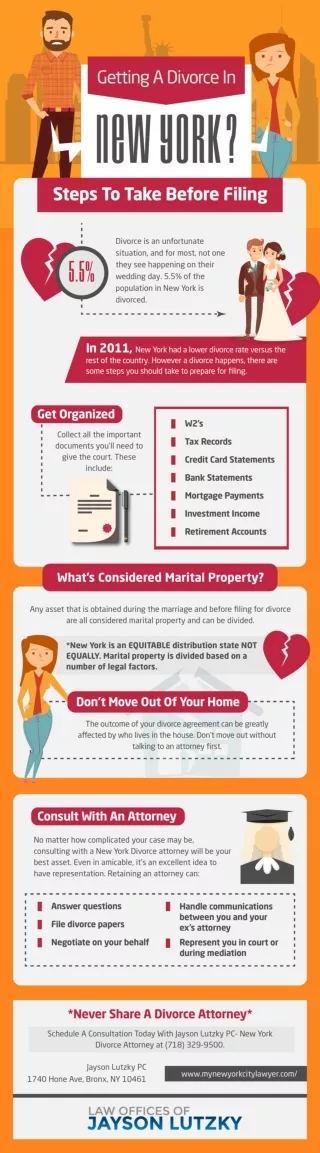

Navigating Divorce: The Crucial Role of Health Insurance Planning in New York In the intricate landscape of divorce proceedings, couples are confronted with a multitude of considerations demanding careful attention. Amidst the emotional turmoil and logistical hurdles, one crucial facet frequently sidelined is the strategic planning of health insurance. In New York, renowned for its complex divorce laws, comprehending the ramifications for health coverage assumes paramount importance. Health Insurance and Divorce in New York requires meticulous attention to ensure adequate protection amidst the dissolution of marital ties. Article: Divorce proceedings in New York entail numerous decisions, from asset division to child custody arrangements. However, amidst these crucial discussions, the matter of health insurance planning is often sidelined. Yet, neglecting this aspect can lead to significant consequences for both parties involved. First and foremost, understanding the existing health insurance coverage is essential. In many marriages, one spouse may be covered

under the other’s employer-sponsored plan. During divorce proceedings, this coverage can become a point of contention. It’s crucial to ascertain the terms of coverage, including whether it extends to the spouse post-divorce, and for how long. Moreover, New York law stipulates certain requirements regarding health insurance coverage during and after divorce. Depending on the circumstances, the court may mandate one spouse to maintain coverage for the other, particularly if there are children involved. Failure to adhere to these requirements can result in legal complications down the line. One common scenario is the need for COBRA coverage. Under federal law, individuals have the option to continue their existing health insurance coverage for a limited period after certain qualifying events, such as divorce. However, COBRA coverage can be costly, and it’s imperative to explore alternative options to avoid financial strain. Another consideration is the availability of health insurance through the New York State of Health marketplace. Following divorce, individuals may qualify for special enrollment periods, allowing them to enroll in a new plan outside of the standard open enrollment period. Understanding these options and deadlines is crucial for maintaining uninterrupted coverage. Additionally, divorcing couples must consider the long-term implications of health insurance decisions. For instance, if one

spouse has pre-existing medical conditions, securing adequate coverage post-divorce is paramount. Failing to address these concerns during proceedings can lead to future disputes and financial hardship. Furthermore, health insurance planning intersects with other aspects of divorce, such as spousal support and asset division. The cost of health insurance premiums may influence these discussions, particularly if one spouse is responsible for covering the other’s healthcare expenses. Therefore, a comprehensive approach to divorce planning must incorporate health insurance considerations. In some cases, divorcing couples may opt for alternative dispute resolution methods, such as mediation or collaborative divorce. During these processes, health insurance planning can be addressed in a more amicable and cooperative manner, leading to mutually beneficial outcomes. In conclusion, health insurance planning is a critical component of divorce proceedings in New York. By understanding the implications of existing coverage, exploring alternative options, and addressing long-term concerns, divorcing couples can mitigate potential challenges and ensure the continuation of adequate healthcare coverage for all parties involved.