Download

1 / 18

180 likes | 420 Views

What We'll Cover. Issues Faced by Clients with Existing Deferred Annuities . Travelers Life

E N D

1. Annuity Funded Life Helping Your Clients with

Life Insurance & Annuities Welcome slide

Speaker introduces his or herself.

This is one of a series in Travelers Life & Annuity�s Selling with Success.

Today we are going to focus on utilizing annuities and life insurance in conjunction with one another in a concept often known as Annuity Funded Life.

Annuities and life insurance are often thought of as mutually exclusive. Each is viewed as handling a specific asset of a client�s planning needs. Both are life insurance based contracts, but Annuities have come to be viewed as handle accumulation for retirement, while life insurance is viewed as offering death protection. However, in many cases they can work together to provide for a client and client�s family in a manner better than they can individually. How, we�ll look at other aspects of these two contracts � the annuity�s distribution aspects and life insurance as a tool for wealth replacement. The two together can offer, with proper planning, potentially much more to a client�s heirs and potentially without income taxes and potential without estate taxation.

We�ll talk about the features that each type of contract provides and how they can work together.

Welcome slide

Speaker introduces his or herself.

This is one of a series in Travelers Life & Annuity�s Selling with Success.

Today we are going to focus on utilizing annuities and life insurance in conjunction with one another in a concept often known as Annuity Funded Life.

Annuities and life insurance are often thought of as mutually exclusive. Each is viewed as handling a specific asset of a client�s planning needs. Both are life insurance based contracts, but Annuities have come to be viewed as handle accumulation for retirement, while life insurance is viewed as offering death protection. However, in many cases they can work together to provide for a client and client�s family in a manner better than they can individually. How, we�ll look at other aspects of these two contracts � the annuity�s distribution aspects and life insurance as a tool for wealth replacement. The two together can offer, with proper planning, potentially much more to a client�s heirs and potentially without income taxes and potential without estate taxation.

We�ll talk about the features that each type of contract provides and how they can work together.

2. First, let�s focus on the specific areas we�ll be covering today.

We�ll talk about how many clients with existing deferred annuities are not doing the full range of planning with their annuity contracts and the issues that they potentially face as a result. Then we�ll see how additional planning with an annuity and life insurance combination can help both a client and their heirs. We�ll look at a couple typical client situations and talk about their tax issues and how numbers might appear for a client with and without planning.

And, we�ll spend some time on the support that Travelers Life & Annuity can provide for you in working with your clients on these issues.

First, let�s focus on the specific areas we�ll be covering today.

We�ll talk about how many clients with existing deferred annuities are not doing the full range of planning with their annuity contracts and the issues that they potentially face as a result. Then we�ll see how additional planning with an annuity and life insurance combination can help both a client and their heirs. We�ll look at a couple typical client situations and talk about their tax issues and how numbers might appear for a client with and without planning.

And, we�ll spend some time on the support that Travelers Life & Annuity can provide for you in working with your clients on these issues.

3. What About Life & Annuities Annuities

Useful for retirement planning

Offer tax deferred growth

Wide range of distribution options

Life Insurance

Premiums purchase death benefit

Risk borne by life insurance company

In some client situations these can be used together? Let�s spend a moment talking about life insurance and annuities. Each has traditionally had their place with clients.

Annuities � have typically been used as tax-deferred accumulation vehicles. Even with recent changes in the tax law annuities may still be appropriate, if the client has a sufficiently long enough time horizon. Most clients have used annuities specifically for accumulation and few annuities are being annuitized. Most annuities, however, have a number of attractive distribution options � these include annuitization and withdrawals. While these vary from annuity contract to annuity contract, most annuities offer enough options that a client can find an approach that meets their planning needs.

Life Insurance � has traditionally been used to provide a death benefit. In exchange for premium payments, an insurance company offers to pay a death benefit based on a client�s age, health, and performance of a contract�s underlying investments. That death benefit is, when properly handled, received free of income taxation. Additionally, where it is owned outside of a client�s estate it can also be received free of estate taxation. Here we�ll use the life insurance death benefit as a wealth replacement tool.

The proper ownership of life insurance, and the right use of an annuity can be a powerful pair of financial instruments in doing client planning.Let�s spend a moment talking about life insurance and annuities. Each has traditionally had their place with clients.

Annuities � have typically been used as tax-deferred accumulation vehicles. Even with recent changes in the tax law annuities may still be appropriate, if the client has a sufficiently long enough time horizon. Most clients have used annuities specifically for accumulation and few annuities are being annuitized. Most annuities, however, have a number of attractive distribution options � these include annuitization and withdrawals. While these vary from annuity contract to annuity contract, most annuities offer enough options that a client can find an approach that meets their planning needs.

Life Insurance � has traditionally been used to provide a death benefit. In exchange for premium payments, an insurance company offers to pay a death benefit based on a client�s age, health, and performance of a contract�s underlying investments. That death benefit is, when properly handled, received free of income taxation. Additionally, where it is owned outside of a client�s estate it can also be received free of estate taxation. Here we�ll use the life insurance death benefit as a wealth replacement tool.

The proper ownership of life insurance, and the right use of an annuity can be a powerful pair of financial instruments in doing client planning.

4. The Life of an Annuity Let�s consider what happens to a client�s annuity. We see annuities as having two distinct phases.

First, there is the accumulation phase. The annuity takes in dollars and the funds grow on a tax deferred basis. The effect over time has the potential to be impressive. Many clients, even with recent market drops, have large amounts of growth accumulated in the annuities. This, often, is where clients end their planning with annuities.

Let�s consider what happens to a client�s annuity. We see annuities as having two distinct phases.

First, there is the accumulation phase. The annuity takes in dollars and the funds grow on a tax deferred basis. The effect over time has the potential to be impressive. Many clients, even with recent market drops, have large amounts of growth accumulated in the annuities. This, often, is where clients end their planning with annuities.

5. But there is a whole other side However, annuities have another component to their design. It�s the distribution phase. As I mentioned earlier. They can annuitize, under a variety of options (as permitted by their contract) or they can take withdrawals. Annuitization often offers a tax advantage because the exclusion ratio that offsets taxation on some of the distribution. Withdrawals, however, offer more flexibility.

Annuitization is often attractive because someone is liquidating their principal and earnings over a period of time (life, a term certain ,etc). That return of principal offers the ability to exclude a portion of most payments from taxation � something called the exclusion ratio. That exclusion ratio offers some advantages in the right situation and, if you elect life annuitization, the asset will disappear at a client�s death. Used correctly, that can offer a good planning opportunity By contrast, withdrawals offer potentially higher up front taxes, but much more flexibility as a client can start and stop the withdrawals as needed. If a client makes withdrawals during the accumulation phase (and most annuity contracts allow withdrawals of up to a certain percentage each year without a surrender charge) the client can maintain maximum flexibility in that he/she can turn on or turn off the income whenever they want. Note: that taxes will apply and if withdrawn before age 59 1/2 a 10% penalty tax will apply.

The key, however, is that your clients want to look at both phases of their annuity. If a client is going to use their annuity for retirement, great. They will be using both the accumulation and distribution phase.

If a client is NOT going to be using the annuity for retirement, then they still want to look at the distribution phase. While many purchase annuities for their death benefit, and resets, where a client is not going to be using an annuity for retirement � and they plan to pass their annuity value to their heirs � they may be in for a surprise. However, annuities have another component to their design. It�s the distribution phase. As I mentioned earlier. They can annuitize, under a variety of options (as permitted by their contract) or they can take withdrawals. Annuitization often offers a tax advantage because the exclusion ratio that offsets taxation on some of the distribution. Withdrawals, however, offer more flexibility.

Annuitization is often attractive because someone is liquidating their principal and earnings over a period of time (life, a term certain ,etc). That return of principal offers the ability to exclude a portion of most payments from taxation � something called the exclusion ratio. That exclusion ratio offers some advantages in the right situation and, if you elect life annuitization, the asset will disappear at a client�s death. Used correctly, that can offer a good planning opportunity By contrast, withdrawals offer potentially higher up front taxes, but much more flexibility as a client can start and stop the withdrawals as needed. If a client makes withdrawals during the accumulation phase (and most annuity contracts allow withdrawals of up to a certain percentage each year without a surrender charge) the client can maintain maximum flexibility in that he/she can turn on or turn off the income whenever they want. Note: that taxes will apply and if withdrawn before age 59 1/2 a 10% penalty tax will apply.

The key, however, is that your clients want to look at both phases of their annuity. If a client is going to use their annuity for retirement, great. They will be using both the accumulation and distribution phase.

If a client is NOT going to be using the annuity for retirement, then they still want to look at the distribution phase. While many purchase annuities for their death benefit, and resets, where a client is not going to be using an annuity for retirement � and they plan to pass their annuity value to their heirs � they may be in for a surprise.

6. Issue for those Not Planning to Tap Annuities The Double Tax Issue

Estate taxes - client

Income taxes � heirs

Erosion at top income brackets in the 70% range Let�s see what happens when an annuity is not annuitized. It faces what is commonly called a Double Tax.

First, for clients who will owe an estate tax, there will be an estate tax on the value of the annuity.

Secondly, these annuities will ALWAYS face an income tax on any appreciation over the investment in the contract. Either your client � as owner will pay this income tax, or their heirs will pay the tax. And � without special post-mortem elections, the heirs will have to take funds out of the annuity within 5 years after a client�s death � in effect, front loading the tax. Unlike other assets that jump up to the date of death value, annuities do not receive this benefit. It�s the price they pay for the years of tax deferred growth.

At top tax brackets, this can approach 70% erosion of the annuity value. Here, we are showing a simple example to show what happens to an annuity where there have been years of tax deferred appreciation. In this case, out of a $1,000,000 annuity the heirs will, collectively, only net $350,000 � that�s 65% erosion in this example. Even with tax rates dropping, the erosion is still significant. And � clients who have estate tax problems today are likely to continue to have those problems as there is currently is no permanent estate tax repeal.Let�s see what happens when an annuity is not annuitized. It faces what is commonly called a Double Tax.

First, for clients who will owe an estate tax, there will be an estate tax on the value of the annuity.

Secondly, these annuities will ALWAYS face an income tax on any appreciation over the investment in the contract. Either your client � as owner will pay this income tax, or their heirs will pay the tax. And � without special post-mortem elections, the heirs will have to take funds out of the annuity within 5 years after a client�s death � in effect, front loading the tax. Unlike other assets that jump up to the date of death value, annuities do not receive this benefit. It�s the price they pay for the years of tax deferred growth.

At top tax brackets, this can approach 70% erosion of the annuity value. Here, we are showing a simple example to show what happens to an annuity where there have been years of tax deferred appreciation. In this case, out of a $1,000,000 annuity the heirs will, collectively, only net $350,000 � that�s 65% erosion in this example. Even with tax rates dropping, the erosion is still significant. And � clients who have estate tax problems today are likely to continue to have those problems as there is currently is no permanent estate tax repeal.

7. Your Clients Have a Choice The Annuity is going to face income tax one way or another

In your clients hands

In their heirs hands

This becomes the planning approach

Take income today

Use after-tax amounts to reposition the asset However, your clients have a choice. They don�t need to let their heirs see this steep erosion. Rather than continue to view the annuity as an accumulation vehicle, they can look at it with another approach.

These annuities will fact income taxation sooner or later. Either in the hands of your clients or in the hand of their heirs. Since the appreciation is going to be taxed anyway � why not expose it to taxes a little at a time and then use the after-tax proceeds to do additional planning.

Let�s see how this works.

However, your clients have a choice. They don�t need to let their heirs see this steep erosion. Rather than continue to view the annuity as an accumulation vehicle, they can look at it with another approach.

These annuities will fact income taxation sooner or later. Either in the hands of your clients or in the hand of their heirs. Since the appreciation is going to be taxed anyway � why not expose it to taxes a little at a time and then use the after-tax proceeds to do additional planning.

Let�s see how this works.

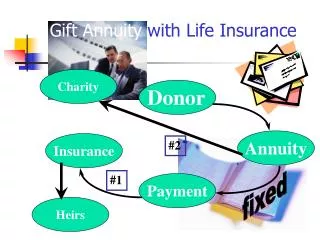

8. Classic Case Here, we start with an annuity that as accumulations built up in it. Rather than allow it to continue to accumulate, without planning we begin to make distributions to the client who owns the annuity. Those distributions can be via withdrawals or annuitization � whatever best suits your client�s situation.

In either event, your client pays income taxes on these distributions. However, these are clients that did not need these annuities or their income. So, they take these after-tax amounts and gift them away, to their family or to a trust.

Here, we start with an annuity that as accumulations built up in it. Rather than allow it to continue to accumulate, without planning we begin to make distributions to the client who owns the annuity. Those distributions can be via withdrawals or annuitization � whatever best suits your client�s situation.

In either event, your client pays income taxes on these distributions. However, these are clients that did not need these annuities or their income. So, they take these after-tax amounts and gift them away, to their family or to a trust.

9. Classic Case Here, the client makes gifts of the after-tax amounts to an irrevocable trust. The trustee, in turn, purchases a life insurance policy on your client�s life. Those gifts pay the annual premiums on the life insurance contract.

When the trustee collects the death proceeds, it can make distributions to the client�s heirs. If your client elected to take withdrawals. Any annuity tax remains can also be distributed out to your client�s heirs.

Here, the client makes gifts of the after-tax amounts to an irrevocable trust. The trustee, in turn, purchases a life insurance policy on your client�s life. Those gifts pay the annual premiums on the life insurance contract.

When the trustee collects the death proceeds, it can make distributions to the client�s heirs. If your client elected to take withdrawals. Any annuity tax remains can also be distributed out to your client�s heirs.

10. Classic Case And � if there are any amounts left in the annuity (typically where the client has been taking withdrawals) those amounts will be subject to the Double Tax, BUT, any remaining amount can also go to the heir.

The upshot is that the heirs are able to receive the death proceeds AND, possibly, some annuity value.And � if there are any amounts left in the annuity (typically where the client has been taking withdrawals) those amounts will be subject to the Double Tax, BUT, any remaining amount can also go to the heir.

The upshot is that the heirs are able to receive the death proceeds AND, possibly, some annuity value.

11. What is Your Result You have made a client happy

Shown the benefit of planning with their annuities

Shown how life insurance can be used as an asset replacement tool

Heirs are happy So where does this leave you and your client. Without sounding overly glib � everyone can be satisfied.

You�re happy because you�ve shown your client how planning with the annuity they might not have otherwise tapped, can help them through the use of distributions used to purchase life insurance.

Your client is happy because they see that they have the potential to provide more to their heirs.

And � even if they do not realize it today � the heirs are happy. They will never see the impact of double taxation on their parent�s death.So where does this leave you and your client. Without sounding overly glib � everyone can be satisfied.

You�re happy because you�ve shown your client how planning with the annuity they might not have otherwise tapped, can help them through the use of distributions used to purchase life insurance.

Your client is happy because they see that they have the potential to provide more to their heirs.

And � even if they do not realize it today � the heirs are happy. They will never see the impact of double taxation on their parent�s death.

12. Ideal Client Age 60 or older

Annuity(ies) not needed for retirement

Has a potential estate tax problem

Estate of $3,000,000 or above

Let�s take a moment to see who is an ideal client.

The typical client will own one or more deferred non-qualified annuities that have appreciation and are expected to grow.

Clients should be age 60 or older. Why? There are two reasons. First, clients in their 60�s will have a better sense than younger clients if they need these assets for retirement or not. Also, clients over age 59 � have much more flexibility in taking distributions from their annuity.

Needless to say, these are clients who don�t need these existing* deferred annuities for retirement.

This concept can work for any client that does not need their annuity for retirement. However, where a client has a potential estate tax problem, the impact of double taxation can make lack of distribution planning more acute. Here, we are showing a $3,000,000 estate. Why? Even though the exemption equivalent is scheduled to increase over the balance of this decade, before the law sunsets and reverts to its old form, clients with estates of this size even with modest estate growth, are likely to continue to see some level of estate taxation.

Any size life insurance policy and design might be utilized with this concept, but the funds coming from the annuity should generally be large enough to generate a death benefit sufficient to replace the lost annuity value. This will assure that the annuity is removed from their estate and its value is replaced in the hands of the heirs. To the extent the annuity withdrawals can support larger death benefits, this concept is even more attractive.

*Note: A potential tax trap exists if a client simultaneously purchases an annuity and a life insurance policy from the same company. This simultaneous purchase can result in the income taxation of the life insurance death benefit.Let�s take a moment to see who is an ideal client.

The typical client will own one or more deferred non-qualified annuities that have appreciation and are expected to grow.

Clients should be age 60 or older. Why? There are two reasons. First, clients in their 60�s will have a better sense than younger clients if they need these assets for retirement or not. Also, clients over age 59 � have much more flexibility in taking distributions from their annuity.

Needless to say, these are clients who don�t need these existing* deferred annuities for retirement.

This concept can work for any client that does not need their annuity for retirement. However, where a client has a potential estate tax problem, the impact of double taxation can make lack of distribution planning more acute. Here, we are showing a $3,000,000 estate. Why? Even though the exemption equivalent is scheduled to increase over the balance of this decade, before the law sunsets and reverts to its old form, clients with estates of this size even with modest estate growth, are likely to continue to see some level of estate taxation.

Any size life insurance policy and design might be utilized with this concept, but the funds coming from the annuity should generally be large enough to generate a death benefit sufficient to replace the lost annuity value. This will assure that the annuity is removed from their estate and its value is replaced in the hands of the heirs. To the extent the annuity withdrawals can support larger death benefits, this concept is even more attractive.

*Note: A potential tax trap exists if a client simultaneously purchases an annuity and a life insurance policy from the same company. This simultaneous purchase can result in the income taxation of the life insurance death benefit.

13. Now, let�s take a moment a see what Travelers Life & Annuity can offer you by way of support with Annuity Funded Life.Now, let�s take a moment a see what Travelers Life & Annuity can offer you by way of support with Annuity Funded Life.

14. Support from Travelers Life & Annuity Client presentation

Client materials

Strong Advanced Sales support

Provides you with back-up on the concept We offer you a wide range of support for these concepts. These range from Model Client Pre-Approach letters to both client and producer one pagers. These client pieces are appropriate for mailings or presenting at meetings. All are available through the Travelers Life & Annuity producer website, your internal wholesalers and your Travelers Life & Annuity Senior Vice President.

We offer you several other tools. These include a primer we call a Quick Guide that offers you classic client cases, examples of ideal clients and even a Q & A highlighting the questions clients are most likely to ask and the typical response. We also offer you a short one sided fact finder that allows you take take notes in preparing the client presentation on Annuity Funded Life insurance. Finally, we also offer you a Step by Step IRD calculator - an Excel spreadsheet that let�s you determine how the estate and income tax erosion works. This is something you can access through the Travelers Life & Annuity producer website. We offer you a wide range of support for these concepts. These range from Model Client Pre-Approach letters to both client and producer one pagers. These client pieces are appropriate for mailings or presenting at meetings. All are available through the Travelers Life & Annuity producer website, your internal wholesalers and your Travelers Life & Annuity Senior Vice President.

We offer you several other tools. These include a primer we call a Quick Guide that offers you classic client cases, examples of ideal clients and even a Q & A highlighting the questions clients are most likely to ask and the typical response. We also offer you a short one sided fact finder that allows you take take notes in preparing the client presentation on Annuity Funded Life insurance. Finally, we also offer you a Step by Step IRD calculator - an Excel spreadsheet that let�s you determine how the estate and income tax erosion works. This is something you can access through the Travelers Life & Annuity producer website.

15. Customized Client Presentations We also offer a complete profession client presentation package that dovetails with the Travelers Life & Annuity life insurance illustration systems. With this you can prepare a high quality professional report for your client that explains the effect of no planning and the impact of planning with life insurance. You saw sections of some pages in this presentation. However, there is much more � including plain English explanations for clients, flow charts and graphs � all to help you in your work with your clients.

We also offer a complete profession client presentation package that dovetails with the Travelers Life & Annuity life insurance illustration systems. With this you can prepare a high quality professional report for your client that explains the effect of no planning and the impact of planning with life insurance. You saw sections of some pages in this presentation. However, there is much more � including plain English explanations for clients, flow charts and graphs � all to help you in your work with your clients.

16. What�s Next? Review your book of business

Identify potential clients

Work with the tools offered through Travelers Life & Annuity Sit down and think about your client base. How many of them own deferred annuities?

How many of these clients are well off enough that they don�t need to take distributions from these annuities, or are taking distributions from these annuities, but really don�t need the income.

Then, sit down and look at the tools you have available to you through Travelers Life & Annuity to work with your clients.

Sit down and think about your client base. How many of them own deferred annuities?

How many of these clients are well off enough that they don�t need to take distributions from these annuities, or are taking distributions from these annuities, but really don�t need the income.

Then, sit down and look at the tools you have available to you through Travelers Life & Annuity to work with your clients.

17. What We Covered So what did we cover today.

First we spoke about the issues clients � or more specifically their heirs � will face if they not do distribution planning with their existing deferred annuities. We looked at the taxation these annuities might face without planning and we examined the impact of redeploying these assets into a life insurance policy, via gifts to their family or a trust.

We looked at some examples and saw how, for some clients, the impact can be significant and often significant well into their years.

Then, we examined the tools that Travelers Life & Annuity has available to you � both for your personal use and client approved materials.

This is [FILL IN NAME OF SPEAKER] thanking you for Travelers Life & Annuity. We hope you enjoyed this edition of selling with Success. We invite you to join us for other, future, sessions to see what opportunities we can provide to you for your work with your clients.So what did we cover today.

First we spoke about the issues clients � or more specifically their heirs � will face if they not do distribution planning with their existing deferred annuities. We looked at the taxation these annuities might face without planning and we examined the impact of redeploying these assets into a life insurance policy, via gifts to their family or a trust.

We looked at some examples and saw how, for some clients, the impact can be significant and often significant well into their years.

Then, we examined the tools that Travelers Life & Annuity has available to you � both for your personal use and client approved materials.

This is [FILL IN NAME OF SPEAKER] thanking you for Travelers Life & Annuity. We hope you enjoyed this edition of selling with Success. We invite you to join us for other, future, sessions to see what opportunities we can provide to you for your work with your clients.

18. Important Disclosure