Download

1 / 4

0 likes | 4 Views

A good credit score is a golden passport to financial independence. It opens reduced loan interest rates, therefore making dream homes or cars more reasonably priced. An excellent credit score makes life somewhat more straightforward and more reasonably priced, like having a VIP ticket to the financial world.<br><br>https://fraud.net/

E N D

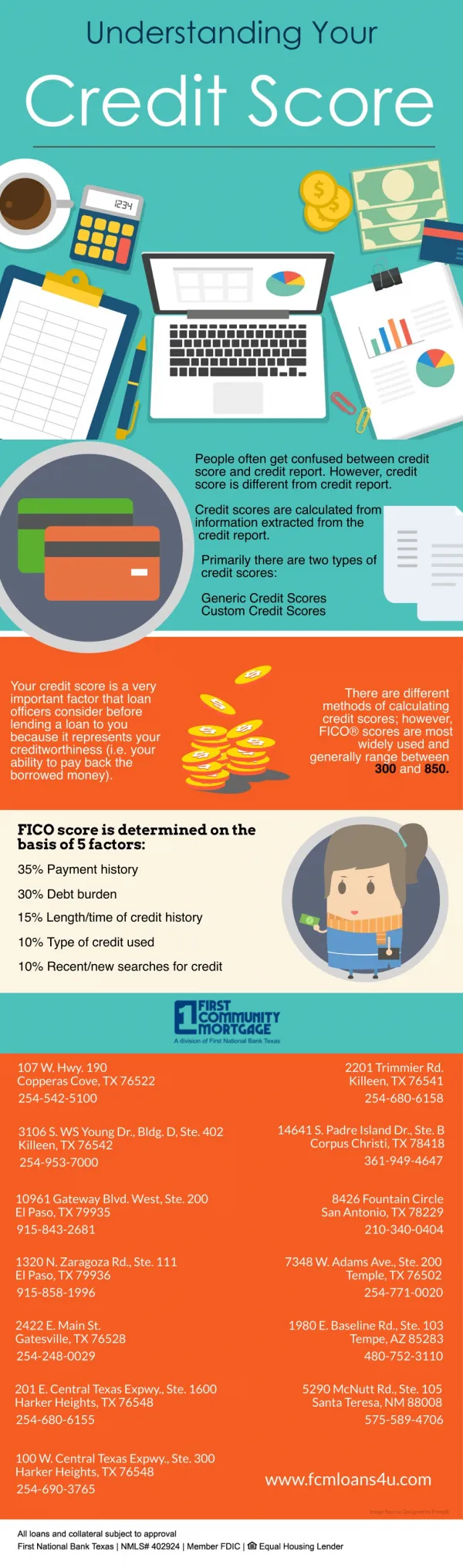

4 Reasons First Payment Default Can Harm Your Credit Score A good credit score is a golden passport to financial independence. It opens reduced loan interest rates, therefore making dream homes or cars more reasonably priced. An excellent credit score makes life somewhat more straightforward and more reasonably priced, like having a VIP ticket to the financial world. Many individuals are unaware, however, of exactly how delicate that score is, particularly in the early years of credit growth. One late payment or one mistake may set off a chain reaction that affects your financial situation for years to come. Consider it as beginning a new career: you want to leave a positive impression throughout the initial few weeks and months. That applies also to your credit score. Like a blemish on a perfect white blouse, that first payment default might be a significant setback. It may tell lenders you are unreliable, which will make them reluctant to provide you with loans in the future. Higher interest rates, late fines, and even harm to your capacity to rent an

apartment or get a loan might also follow from it. Let's explore the four main reasons for the great importance of that initial payment and how it could influence your financial destiny. 1.First Payment Default Leads to Immediate and Significant Score Drop View your credit score as a financial responsibility report card. Lenders evaluate this picture of your handling of borrowed money to determine your dependability as a borrower. Lenders closely review your credit score to assess your creditworthiness. A high credit score denotes your prudent borrowing behavior; a low score shows you could be a riskier bet. Now, the first payment default can say a lot about the way you handle your finances, which could affect your credit score. This is a clear mark that will significantly lower your whole score. Credit scoring systems give payment history great weight; hence, even one mistake may cause your score to drop. This is so because lenders see first-time delay as a severe red indicator that can point to increased future missed payments. This action can leave a wrong impression that may not be easy to overcome. Thus, it is essential to have a perfect credit record in order to achieve your financial stability and dreams. Even if it is a bit owing, always pay your payments on time. To keep on top of your money, set reminders, program payments, or use budgeting tools. Remember that a solid credit score serves as your ticket to better loan conditions, reduced interest rates, and more financial possibilities. The long-term return of this investment in your financial future is excellent. 2.A Bad Credit Report Your credit report is like a bit of a school report card but with considerably more weight—a permanent record of your financial activity. It shows lenders how conscientious you are with money by tracking your borrowing and payback behavior. Thus, first payment default is like having a sizeable lousy mark on your report card that would show up to landlords, possible lenders, and even some companies. Consider it as a financial footprint you carry about wherever. Your report will show this mark for years, which will long shadow your creditworthiness. It is like a constant reminder of that one time you made a mistake that made it more difficult to receive loans, rent an apartment, or even get specific employment. Late payments raise questions for lenders about your dependability with their money. Landlords may be reluctant to let you access their property, and some companies could even doubt your financial capacity. It is not just about securing a loan or apartment rental; a bad credit score may influence many aspects of your life. It may even affect utility deposits and insurance rates. Keeping up with your payments and maintaining a clean credit record is thus rather vital. It is very fundamental to your general financial situation and welfare.

3.Higher Interest Rates and Fees Lower credit scores translate into more borrowing expenses. Consider it as if your credit score were your reputation. Should your score be low, they see you as a riskier borrower—someone who may not be very consistent in returning what they owe. They, therefore, charge higher interest rates to offset that risk, just as a sheriff seeking a larger reward on a known bandit would do. This means you will pay more on anything you borrow—from credit cards to loans—including even items like insurance. Dream automobile you have been looking at? You should anticipate a more extensive monthly cost. You had to balance your credit card for a bit of time. Prepare yourself for those interest payments to really mount up. Paying a premium for everything simply because your credit score is not where it might be is like that. First payment default can increase interest rates over time, which might add a large sum in additional costs. Paying more for the same products someone with better credit might obtain for less seems like throwing money away. Building and maintaining a high credit score is thus quite crucial. It reflects your financial situation and may greatly influence your financial future. 4.Limited Access to Credit Your bad credit score can make it harder for you to get authorized for loans or new credit accounts. Consider your credit score as your financial report card; it indicates to lenders prior borrowing and repaying behavior that shows responsibility. Lenders may be reluctant to provide credit to someone

with a payment default or heavy debt when it is less than perfect. They consider it a danger, as you could not consistently return their money. Making a big purchase like a dream house or a new automobile may be rather taxing. Suddenly, that significant milestone might seem unattainable as you cannot get the required finance. Alternatively, you can have an unanticipated financial crisis involving a medical expense or essential house repair and want fast access to money. A bad credit score may significantly restrict your choices and cause you to feel trapped. However, it is not just about significant purchases or crises; a bad credit score may affect your financial life in a lot of different ways. On credit cards or loans, you may find yourself paying more in the long term if interest rates rise. Landlords may be reluctant to rent to you; even some companies review credit records throughout the employment process. Although it takes time and work, rebuilding your credit is an investment in your financial future that may provide doors to possibilities and provide peace of mind.