Download

1 / 3

30 likes | 34 Views

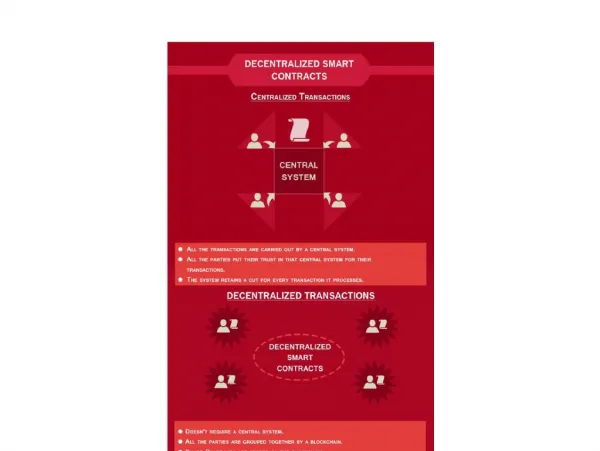

Smart contracts are agreements between two or more parties stored securely inside a blockchain. Smart contract development services include creating & implementing immutable and self-executing computer codes that facilitate contracts without intermediates.<br>

E N D

Smart Contracts - The Heart Of Blockchain Revolution A Smart Contract shows quick-witted intelligence in a bright and clever manner. They are also known to excel in academic aspects of life. Okay, now that was too easy! For the record, BTW that’s not what a Smart Contract is. A Smart Contract development is a self-executing contract that is actually a computer protocol intended to digitally facilitate the performance of a contract. These contracts help you to exchange anything of value in a conflict-free way without the need for the middle man. Now let us delve deeper to understand how smart contracts enhance the insurance process

How the Insurance industry can benefit from Smart Contracts: Blockchain technology improves the existing processes, which creates a great impact on the industry. Experts predicted that insurance industries will experience the most significant changes from smart contracts and Blockchain. This is mainly because smart contracts give autonomy, backup, speed, savings, safety, trust, and accuracy. With that being said, there are multiple ways in which smart contracts are useful in the insurance space. Reduce paperwork: This is pretty obvious already, but yes, when smart contracts are in you can save yourself from a ton of paperwork Through smart contracts everything is done through code on the blockchain network, so you can turn off the printer and cap your pens. These contracts is difficult, as they can exist on multiple ledgers. This can benefit insurance industries because there is less dependence on the interpretation of clauses. Also, these processes are quicker and cheaper, which results in a reduction in premium rates. Reduce Fraud Through Transparency: Smart Contracts make the fraudulent activity more difficult because all the data are encrypted on a shared ledger. This means that the document is visible to the public and every change in the contract is permanently recorded.

Even though the data are publicly viewed, the privacy of the parties involved in the contracts is maintained due to the encryption. This visibility adds a better level of transparency by allowing people to see what's going on in the data. Remove administrative barriers: This one is straightforward but worth mentioning because these are created by the individuals involved in the agreement. This allows for the parties to skip the administrative process. The timeline for a contract drawn up through administration is subject to the availability and constraints of the people in the administrative area. Instead, by creating the contract through the blockchain, that process can be eliminated entirely, allowing the process to run much smoother and more efficiently. Key takeaway: Many insurance sector participants are already working with DLT and smart contract development services; whereas others may be at an earlier stage of analysis of the use cases and technology. With smart contracts, insurers will be able to automate their policies and services, reduce administrative and claims processing costs, increase transparency, and prevent fraud. Blockchain Firm supports innovative endeavors and is ready to help implement blockchain technology and smart contracts in particular.