Download

1 / 21

220 likes | 828 Views

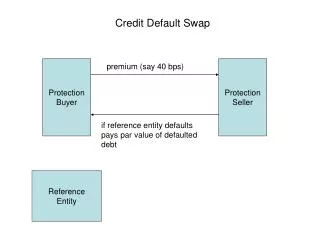

Credit Default Swaps. A Credit Default Swap (CDS) is a contract in which the writer offers the buyer protection against a credit event in a reference name for a specified period of time in return for a premium payment. Typical CDS cashflows

E N D

Credit Default Swaps • A Credit Default Swap (CDS) is a contract in which the writer offers the buyer protection against a credit event in a reference name for a specified period of time in return for a premium payment. • Typical CDS cashflows • The contract pays par in return for 100 nominal of debt if the reference name suffers a credit event before the maturity of the deal. • The buyer pays a premium quarterly in arrears.

CDS Structure Pre-default Quarterly premium in arrears Protection Buyer Protection Seller Post-default Defaulted debt of reference name Protection Buyer Protection Seller Par less fraction of premium

CDS Example Pre-default 314.486 bps quarterly in arrears Protection Buyer Protection Seller Post-default $1,000,000 Par GMAC Protection Buyer Protection Seller $1,000,000 plus fraction of premium

Par Asset Swap Example Market Fixed Coupon Credit Bond Cash=Bond Dirty Price Floating Floating payments +par at maturity Interest Rate Swap Desk AS Trading Desk Investor Fixed Par

CDS - Asset Swap Hedge Market Fixed Coupon Credit Bond Cash=Bond Dirty Price Quarterly premium in arrears and defaulted debt upon default Floating Floating payments +par at maturity Interest Rate Swap Desk AS Trading Desk Investor/ Protection Buyer Protection Seller Fixed Par Par less fraction of premium upon default

CDS - Asset Swap Hedge Example Market $10,000,000 Par GMAC 5 5/8s of 5/15/2009 $9,300,000+$42,187.50=$9,342,187.50 Floating 3M LIBOR+256.8 bps Floating 3M LIBOR+273.7bps 314.486 bps quarterly in arrears Interest Rate Swap Desk AS Trading Desk Investor/ Protection Buyer Protection Seller $10,000,000 par of GMAC debt on default event Fixed 5.45232% semi-annual $10,000,000 initially $10,000,000 less partial premium on default event

Initial Cashflows Market $10,000,000 Par GMAC 5 5/8s of 5/15/2009 $9,300,000+$42,187.50=$9,342,187.50 Interest Rate Swap Desk AS Trading Desk Investor/ Protection Buyer Protection Seller $719,881 $10,000,000 initially

Typical Periodic Cashflows Market $281,250 semi-annually LIBOR+$64,200 quarterly (approx. $200,000) LIBOR+$68,425 quarterly (approx. $204,200) $79,495 quarterly Interest Rate Swap Desk AS Trading Desk Investor/ Protection Buyer Protection Seller $272,616 semi-annually

Cashflows on Default Market $10,000,000 Par defaulted GMAC 5 5/8s of 5/15/2009 $10,000,000 Par defaulted GMAC 5 5/8s of 5/15/2009 or similar Interest Rate Swap Desk AS Trading Desk Investor/ Protection Buyer Protection Seller $10,000,000 less partial premium Unwind IR swap Unwind IR swap

Is the Protection Buyer Hedged? • Upon default, the protection buyer receives $10m from the protection seller and (assuming 40% recovery) delivers defaulted debt worth $4m. At the inception of the contract, the GMAC note was only worth $9.3m. So the buyer receives a net of $6m from the CDS, has really lost only 9.3-4=$5.3m. So the buyer has too much CDS. The correct hedge ratio is given by • In this case the protection buyer should buy $10m x (.93-.4)/(1-.4)=$8.9m notional CDS to be hedged.

CDS Basis • A number of factors observed in the market serve to make the price of credit risk that has been established synthetically using credit default swaps to differ from its price as traded in the cash market using asset swaps. • Identifying such differences gives rise to arbitrage opportunities that may be exploited by basis trading in the cash and derivative markets. This in known as trading the credit default basis and involves either buying the cash bond and buying a CDS on this bond, or selling the cash bond and selling a CDS on the bond. • The difference between the synthetic credit risk premium and the cash market premium is known as the basis. CDS Premium – Z-Spread = basis.

CDS Basis Market Basis=314.486-291.9=22.586 $10,000,000 Par GMAC 5 5/8s of 5/15/2009 Z-Spread=291.9 $930,000+$4,218.75=$934,218.75 Floating 3M LIBOR+256.8 bps Floating 3M LIBOR+273.7bps 314.486 bps quarterly in arrears Interest Rate Swap Desk AS Trading Desk Investor/ Protection Buyer Protection Seller Fixed 5.45232% semi-annual $1,000,000

CDS Basis • The basis is usually positive, occasionally negative, and arises from a combination of several factors, including • Bond identity: The bondholder is aware of the exact issue that they are holding in the event of default; however, default swap sellers may receive potentially any bond from a basket of deliverable instruments that rank pari passu with the cash asset. This is the delivery option held by the protection buyer. • Depending on the precise reference credit, the CDS may be more liquid than the cash bond, resulting in a lower CDS price, or less liquid than the bond, resulting in a higher price.