Download

1 / 3

80 likes | 113 Views

Read and understand the Concept of GST refund Step by Step <br>Visit our site to know more: https://www.mygstrefund.com/<br>

E N D

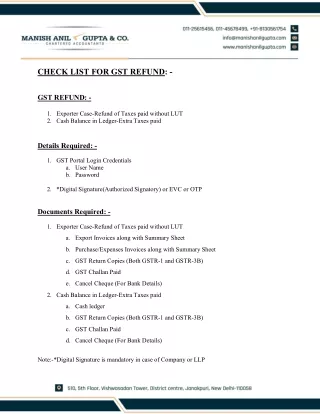

Brief Explanation of GST Refund The GST Refund Administration process requires the resident to follow elaborate advances, and submit records and proclamations at whatever point expected, to the GST specialists for ensuring a GST rebate. The limits under GST can be the cash balance in the electronic cash record kept in excess or cost paid unexpectedly or the gathered Data Tax cut (ITC) ill-suited to be utilized for charge portions due to zero-assessed bargains or modified charge structure. The designs wherein a GST rebate is ensured vacillate according to the kind of GST markdown being ensured. For instance, the markdown of IGST in conveys (with charge portion) can be ensured simply by declaring nuances in the GSTR-1 and GSTR-3B. While the rebate of cash paid more than the electronic cash record can be declared by applying structure RFD-01. Thus, the means or the association differs with the kind of GST markdown. Most recent Reports on GST Refund 05th July 2022 Citizens can avoid the Coronavirus pandemic period (first Walk 2020 and 28th February 2022) while working out as far as possible for recording GST Refund applications under Segments 54 or 55 of the CGST Act. first February 2022 Financial plan 2022 update-1. Segment 54 is changed to give that refund guarantee of any equilibrium in the electronic money record can be made in a specific structure and way endorsed. 2. As far as possible guarantee refunds by UN organizations are presently a long time from the last day of the quarter when supply was gotten rather than a half year. 3. The limitation to Refund citizens for charge defaults, that prior applied to unutilized ITC refunds, is currently reaching out to different sorts of refunds. 4. The important date to document the refund guarantee application for provisions to SEZ is explained in the new substatement (ba) of condition (2) of the clarification. first May 2021 Were as far as possible to pass orders for dismissing any refund guarantee completely or halfway falls between the fifteenth of April 2021 and the 30th of May 2021, it is expanded. The drawn-out time limit will be later of two dates: (1) 15 days after the answer to the notice OR (2) 31st May 2021 Moves toward presenting a refunds pre-application structure Rebate pre-application is a design that residents ought to wrap up to offer information about their business, Aadhaar number, individual cost nuances, convey data, use and theory, and so on. Residents ought to record this pre-application structure for an extensive variety of GST rebates. This design need not be checked and can't be adjusted once submitted. Thusly, the client ought to be wary while entering the nuances. The two phases drew in with recording the GST markdown pre-application structure according to the accompanying:

Stage 1: Sign in to the GST door, go to the 'Organizations' tab, click on 'Limits' and select the 'Rebate pre-application structure' decision. Stage 2: On the page showed called 'Rebate pre-application structure', fill in the nuances asked, and click on 'Submit'. A certification of convenience will be displayed on the screen. The going with nuances ought to be represented: Nature of business - Producer, transporter exporter, dealer, and expert center Date of issue of IEC (only for exporters) - Those applying for a markdown by the righteousness of items (without a portion of obligation) ought to furnish the date of issue of the Import Ware Confirmation. The aadhaar number of the fundamental endorsed signatory is mandatory. Worth of products made in the FY 2019-2020 (only for exporters) - This ought to be enlisted at the GSTIN level and not the Holder level. Individual obligation paid in FY 2019-2020 Development evaluation paid in FY 20212022. Capital utilization and adventure made in FY 2019-2020 Markdown connection of IGST paid on an item of items (with charge portion) Conveys are considered as 'Zero-assessed supplies' under GST. Thus, the obligation paid (IGST and cess, if any) is equipped for a markdown by the exporter. Since the quantum of trades can be enormous in exporters, the GST entrance works with a less troublesome wrap-up of GST rebate. The same application in structure RFD-01 is normal for this present circumstance. Certain conditions ought to be satisfied by the exporter for a GST markdown. Above all else, Table 6A in GSTR-1 ought to be finished off with Conveyance bill nuances associated with exchange trades (with a portion of the cost) and recorded by the due date. Moreover, the layout nuances ought to be represented in thing 3.1 (b) of Table 3.1 of GSTR-3B, the related charge ought to be paid, and the return should be archived by the due date suggested by the GST guideline. In the item receipt data given under Table 6A of Design GSTR-1, the right, and complete conveyance bill number, moving charge date, and port code nuances ought to be given. It should be seen that convey trades carried out in a responsibility period ought to be reported in the GSTR-1 and GSTR-3B of a comparative significant cost period. Care ought to be taken to report the total of IGST and cess as a figure identical to or higher in Table 3.1 of GSTR-3B than Table 6A and Table 6B of GSTR-1. The GST authority considers the conveyance bill as a rebate application. The GST doorway sends exchange nuances to the ICEGATE as revealed on GSTR-1. In like manner, a certification that GSTR-3B was requested for the appropriate obligation period is sent. The Practices structure takes a gander at the information on GSTR-1 to the information on their conveyance bill and Item Broad Manifest (EGM) and a short time later handles the rebate. The ICEGATE structure will confer portion information to the GST entrance once the markdown portion has been credited to the residents' records. The GST door will give the information to the residents by SMS and email.

Pushes toward applying in structure RFD-01 for most kinds of GST markdown RFD-01 ought to be appealed to for the going with sorts of GST rebate claims: Overflow cash balance from the electronic cash record or excess charge portion. IGST is paid on the result of organizations (with a portion of obligation). Accumulated ITC as a result of items of work and items without a portion of the obligation. Gathered ITC on account of arrangements made to SEZ unit/SEZ engineer (without a portion of the cost). ITC gathered given upset charge structure (charge on inputs higher than an obligation on yields). Expecting a recipient of considered exchanges has paid the obligation on inner supplies that qualify as considered conveys and has ensured ITC for the cost paid in their electronic credit record, the recipient of these considered items is equipped for a rebate of the obligation total paid (on a condition that the supplier of such considered exchanges doesn't ensure a markdown). A charge is paid on arrangements made to SEZ units/SEZ engineers (with portion of the cost). A charge paid on an intrastate reserve later held as roadway supply as well as the reverse way around. In case a supplier of considered conveys paid charge on considered supplies without charging an assembling charge from the buyer of considered exchanges, then, at that point, he would be able to promise it as a markdown (on a proclamation that the recipient or buyer of such considered exchanges doesn't ensure a rebate). On account of Assessment or Impermanent Evaluation or Appeal or another solicitation. There is in like manner a plan for ensuring a rebate on 'Another ground' in RFD-01. Care ought to be taken to report unsurprising information on the sales in both GSTR-1, where it applies, and RFD-01. A statement by an endorsed clerk/cost accountant ought to be submitted along in unambiguous cases. Follow the underneath pushes toward recording a markdown application in RFD-01: Stage 1: Sign in to the GST door and go to the 'Organizations' tab, click on 'Limits' and select the 'Usage of rebate' decision. Stage 2: On the page that appears, select the legitimization for markdown or the sort of rebate and snap on 'Make markdown application'. Stage 3: Select the period for which a rebate is to be applied and select 'Yes' or 'No' on the trade box 'to report a nothing markdown'. n the occasion of nothing rebate application, the resident can sign or endorse the declaration and keep on recording using either DSC or EVC. This step isn't fitting in sorts of limits, for instance, excess money balance in the record, intrastate stock later held as parkway supply as well as the reverse way around, examination or transitory assessment or charm or another solicitation. Stage 4: Enter the nuances on the relevant page that gets shown, considering the sort of markdown picked in the past step. Type 1: Overflow cash balance in electronic cash record Type 2: Excess charge paid through GSTR-3B Sort 3: Accumulated ITC given results of work and items without a portion of evaluation Type 4: Gathered ITC due to arrangements made to SEZ unit/SEZ engineer (without a portion of the cost) Type 5: ITC assembled due to changed charge structure. For Following Issues Visit:- GST Refund Sanctioned but not Received. GST TDS Refund.