Download

1 / 6

80 likes | 409 Views

What is a one time close? What is a two time close?<br>Those are just two of the different types of construction loans that you can choose from when acquiring a home loan. Discover the benefits of each and figure out which one might work best for you and your home. For information on construction loans, visit http://www.novahomeloans.com/loan-info/our-loan-programs/construction-loans/.<br>And check out the other home loan programs to choose from at http://www.novahomeloans.com/loan-info/our-loan-programs/.

E N D

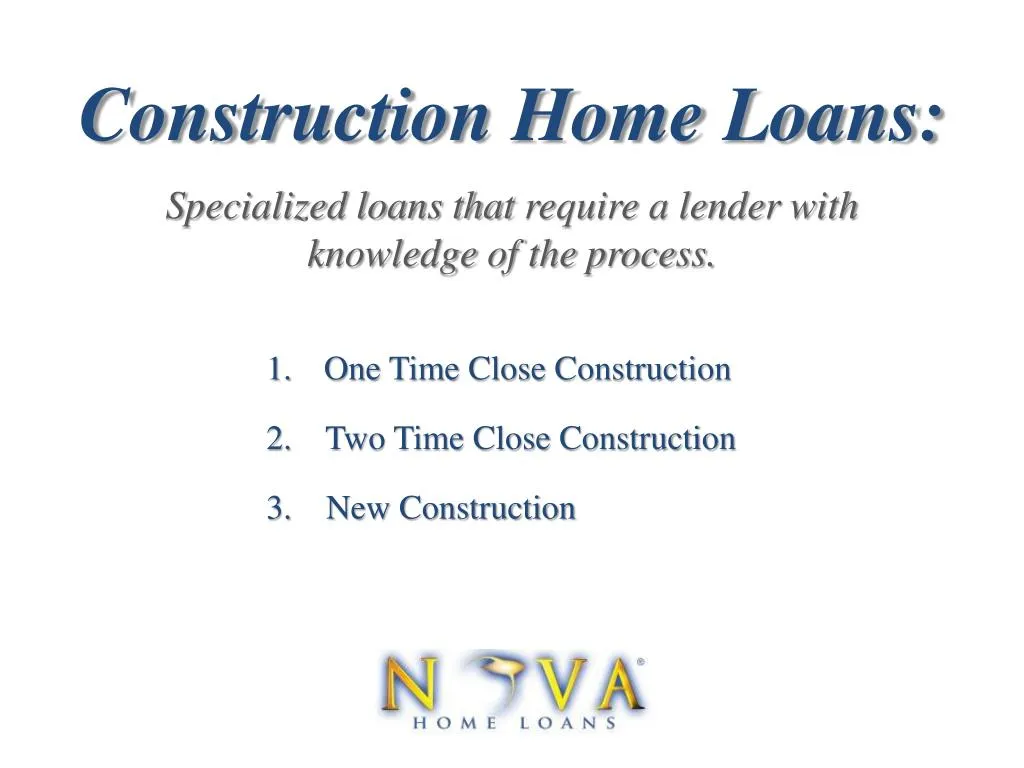

Specialized loans that require a lender with knowledge of the process. Construction Home Loans: One Time Close Construction 2. Two Time Close Construction 3. New Construction

When rates are low it's the ideal time to take advantage of the One Time Close Construction Loan. Your rate will never change from the beginning of construction through the life of the loan. And, you pay only one set of closing costs. 1. One Time Close Construction Loans

When interest rates are on the rise, it's usually better to do a Two Time Close Construction Loan because the initial loan covers only the cost of construction and can be configured as an "interest only" loan. 3/1 or 5/1 ARMs (Adjustable Rate Mortgages, fixed for 3 or 5 years), are usually recommended for this purpose because they traditionally carry a lower interest rate. Lower interest rates help to keep payments low during the construction process. 2. Two Time Close Construction Loans

With a Two Time Close construction loan, you are charged with 2 sets of closing costs, one for the construction loan and another for the permanent loan. However, some lenders will waive costs on the construction loan if you commit to doing the permanent loan with them. With a Two Time Close, you also have the option to lock your permanent rate at the time the construction loan is originated, with a "float down" option. At the end of construction, you have the option of choosing the locked rate or the current rate for your permanent loan, whichever is lower. Two Time Close Construction Continued

Construction loans used for new homes generally pay the builder or general contractor in installments or "draws", as each previously agreed upon stage of construction is satisfactorily completed. Interest is paid by the borrower on these construction funds as they are dispersed. After completing a project, the construction financing is usually converted into a permanent, long-term mortgage. 3. New Construction Loans

Construction loans may also be the most appropriate choice for extensive remodeling projects because in most cases, they provide the owner with more money than can be accessed from the home's equity through a Cash-Out Refinance. Other Considerations