Download

1 / 5

50 likes | 273 Views

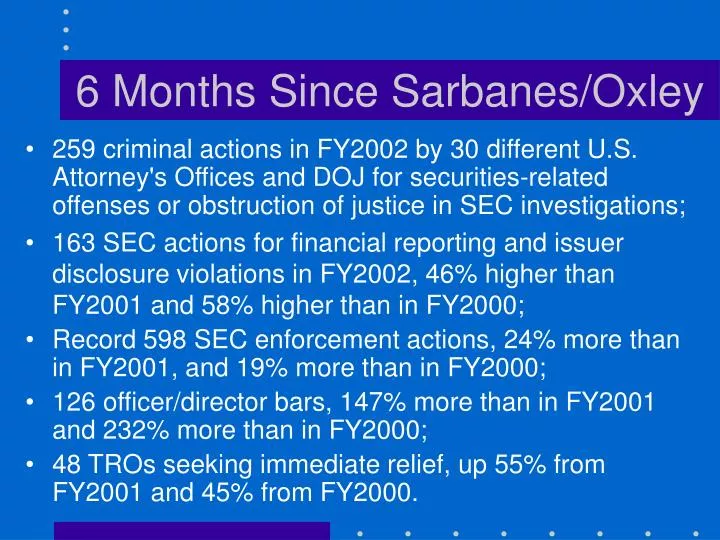

6 Months Since Sarbanes/Oxley. 259 criminal actions in FY2002 by 30 different U.S. Attorney's Offices and DOJ for securities-related offenses or obstruction of justice in SEC investigations;

E N D

6 Months Since Sarbanes/Oxley • 259 criminal actions in FY2002 by 30 different U.S. Attorney's Offices and DOJ for securities-related offenses or obstruction of justice in SEC investigations; • 163 SEC actions for financial reporting and issuer disclosure violations in FY2002, 46% higher than FY2001 and 58% higher than in FY2000; • Record 598 SEC enforcement actions, 24% more than in FY2001, and 19% more than in FY2000; • 126 officer/director bars, 147% more than in FY2001 and 232% more than in FY2000; • 48 TROs seeking immediate relief, up 55% from FY2001 and 45% from FY2000.

Future of Enforcement More Resources and Better Coordination: • DOJ Corporate Fraud Task Force (DOJ, FBI, Treasury, DOL, USPIS, SEC, CFTC, FERC, FCC) • U.S. Attorney ($9m in FY04 for new fraud prosecutors) • FBI ($16m in FY04 for new fraud agents) • SEC (47% increase in FY03 & 17% increase in FY04) • State Attorneys General • District Attorneys • State Securities Regulators • NYSE/Nasdaq/Other SROs

DOJ Charging Principles • Factors used to decide whether to prosecute: • Nature and seriousness of offense • Pervasiveness of wrongdoing in corporation • Corporation’s history of similar conduct • Company’s voluntary disclosure and cooperation • Existence and adequacy of compliance program • Corporation’s remedial actions • Collateral consequences of prosecution • Adequacy of prosecuting only individuals for crime • Adequacy of civil or regulatory enforcement actions

SEC’s New Enforcement Model In evaluating charging decisions, Enforcement Division looks at 4 factors: • Self-policing: Did company establish effective compliance procedures? • Self-reporting: Did company conduct thorough review of misconduct, and promptly and completely disclose to regulators? • Remediation: Did company dismiss or appropriately discipline wrongdoers, and improve internal controls? • Cooperation: Did company provide SEC staff with all information on timely basis?

What Actions Should Be Taken? • Make sure you have necessary compliance programs in place (general code of conduct and ethics, money laundering, FCPA, insider trading, antitrust, environmental, export/import controls, OSHA, etc.) • Director & Officer education and training • Internal financial reporting system for executive officer certification • Corporate Responsibility Officer • Internal systems for handling dissenters & whistleblowers