1 / 9

90 likes | 96 Views

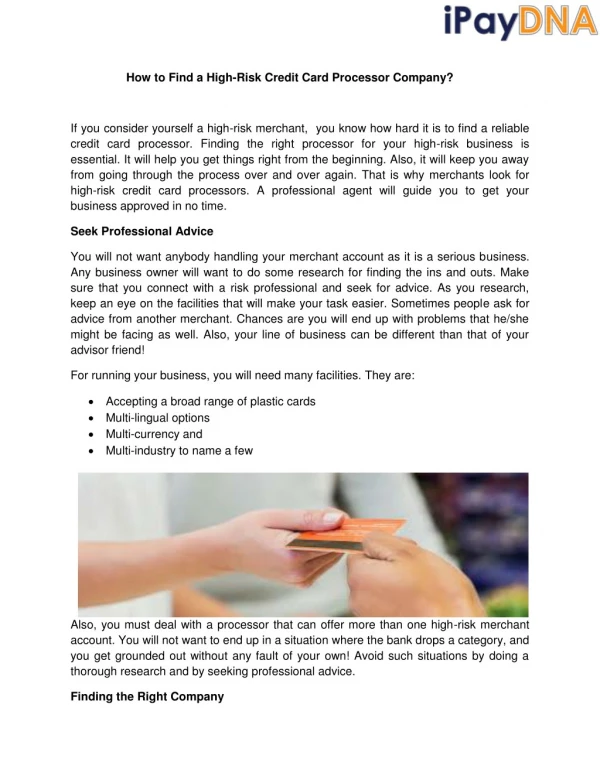

PayCly provides the most authentic and generic payment solutions to merchants. Our High-Risk Payment Processor allows you to control your annual and monthly transactions. We ensure timely payment settlement so that the merchant never have with delays.<br><br>For more details:- <br>Contact us: info@paycly.com <br>Visit Here: https://paycly.com/

E N D

High-Risk Payment Processor for Providing Delightful Payment Processing Experience to Merchants Omni-channel payment processing is becoming a crucial company strategy as consumers demand more convenient and flexible purchasing options. We now live in the digital era. Our cell phones are always with us in our hands or our pockets, and they have irreversibly changed the way we interact with the world, including how we purchase. Consider the most recent important purchase you made. Did you go to the store and purchase whatever was on the shelf? Or did you have a more tumultuous encounter? The following scenario is pretty prevalent these days: You go to the store, look up competitor prices on your phone, go home, do some more research, see a few advertisements on social media, and then decide to buy the thing online. This customer journey isn't just for B2C customers. B2B buyers are increasingly having comparable complex experiences, in which they connect with a company at multiple touch points before making a purchase.

Increased Customer Satisfaction with Multi-Channel Processing Consumer expectations have evolved as a result of the shifting purchasing process. They want to interact with a brand or organization in a consistent manner across numerous platforms and touch points. This mentality, crucially, extends to payments. Consumers want the freedom to pay where and how they choose, whether it's in a store, on their phone, online, or elsewhere. Businesses must be clever enough to gather payments anytime clients exhibit buying intent, independent of sales channel if they wish to prosper in the modern era. This is when omnichannel processing comes into play. Customers get a better experience when businesses use an omnichannel strategy. Customers have a consistent and unified brand experience across all platforms. They can easily navigate between the various touch points, whether it's checking out the brand's social media profile or going to the store. All of these pleasant experiences have strengthened the company's credibility and trustworthiness. PayCly provides the most authentic and generic payment solutions to merchants. Our High-Risk Payment Processor allows you to control your annual and monthly transactions. We ensure timely payment settlement so that the merchant never have with delays.

What's the Difference Between a Payment Processor and a Payment Gateway? You may have heard the terms payment processor and payment gateway as a small business owner. Do you know the difference between them, although they both play a vital role in payment processing? To completely appreciate the distinctions between payment processing and a payment gateway, you must first become familiar with all of the major players, their functions, and how they interact. ● Credit Card Network: First Data is a site where everything comes together for credit card processing and charge collection. ● Merchant Acquiring Bank: The bank that provided the merchant with a merchant account from which he or she can withdraw funds. The Customer: The person who swipes or keys in their card. The merchant: The Company that receives payment in exchange for goods or services delivered to a consumer. The ERP/accounting software: The tool that a company employs to track and report financial activities. Issuing Card Bank: The bank that issued the credit card to the consumer. For example, a Visa can be issued by any of many local or national banks, such as Chase or Wells Fargo. ● ● ● ● First, we must comprehend the essential elements of payment processing. The following are the key players in every credit card transaction:

Which Do I Need: A Payment Processor or a Payment Gateway? Businesses who want to handle payments within their ERP/accounting software or eCommerce store should use a payment gateway. A basic merchant account may be the best option if you don't utilize accounting software or operate an internet store. If you're looking for a merchant account, look for one that offers flat-rate or interchange-plus pricing, no contracts, PCI compliance, next-day financing alternatives, chargeback management, and 24/7 in-house customer service. A payment gateway is the best option if you want to streamline your payment acceptance and handle credit cards online. If you want to streamline your payment acceptance and handle credit cards online. Make sure to choose a processor that has its proprietary payment gateway while shopping for a payment gateway. To achieve PCI compliance for small enterprises, the gateway should be designed by in-house software engineers, and client card information should be stored off-site.

What is a Chargeback? And is it Always Necessary to Fight Chargebacks? When a chargeback occurs, you may have an emotional reaction. You can be furious or upset and wish to retaliate. Unfortunately, chargebacks are structured to benefit cardholders rather than merchants, and in some situations, pouring time and money into fighting a chargeback will be futile. Are You Able to Find a Different Solution to Resolve the Conflict? A customer can file a chargeback if they never received the product, if it was damaged when it arrived, or if something went wrong. After a chargeback is filed, merchants have ten days to contact customers. You have ten days to work with the customer and come up with a different solution. Customers are usually satisfied with an exchange or refund. You could also be able to offer them further discounts. You can win the battle before it even starts if you can settle the situation and reverse the chargeback.

What is a Chargeback? And is it Always Necessary to Fight Chargebacks? While chargebacks are inconvenient, they aren't always worth fighting. You must consider the benefits and drawbacks of disputing a chargeback. Is this a case of friendly fraud? Is your case likely to be successful? Will you devote too much time and effort to combating it? Is your name, money, or merchant account on the line? Is there another method to solve the problem? You'll be able to select when to dispute chargebacks based on the answers to these questions. PayCly is substantially gaining momentum in the market for providing High-Risk Payment Processor to merchants. In many cases, we have surpassed the merchant's expectations and provided the relevant payment processing solutions. We provide good and worthy returns for your hard-earned money.

Contact Us Now For Payment Gateway Solutions 7 Temasek Boulevard, #12-07 Suntec Tower 1, Singapore, 038987 info@paycly.com https://paycly.com