Download

1 / 6

0 likes | 12 Views

Before delving into specific health insurance plans, it's essential to recognize the unique healthcare needs that accompany the aging process. As seniors age, they often encounter a variety of health issues, ranging from chronic conditions to the need for specialized medical care. Health insurance plans for senior citizens are tailored to address these specific needs, providing coverage for hospitalization, prescription drugs, preventive care, and other essential medical services.<br>visit here-https://policychayan.com/health-insurance/health-insurance-plans-for-senior-citizens

E N D

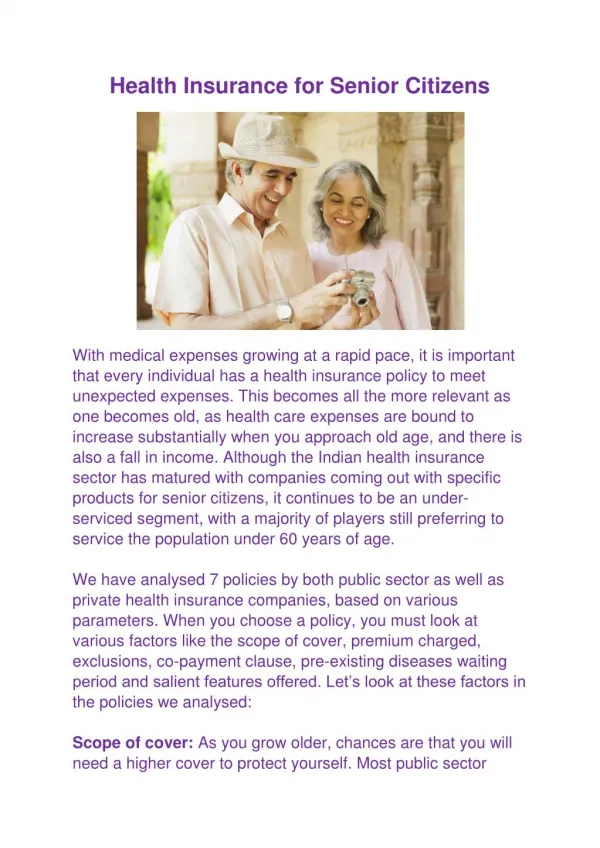

Navigating the Golden Years: A Comprehensive Guide to Health Insurance Plans for Senior Citizens Introduction: As individuals gracefully step into their golden years, the importance of health and well-being takes center stage. With age, the likelihood of facing medical challenges increases, making health insurance a crucial aspect of a senior citizen's financial and healthcare planning. In this article, we'll delve into the various health insurance plans designed specifically for senior citizens, offering comprehensive coverage to ensure a secure and healthy retirement. Understanding the Unique Healthcare Needs of Seniors:

Before delving into specific health insurance plans, it's essential to recognize the unique healthcare needs that accompany the aging process. As seniors age, they often encounter a variety of health issues, ranging from chronic conditions to the need for specialized medical care. Health insurance plans for senior citizens are tailored to address these specific needs, providing coverage for hospitalization, prescription drugs, preventive care, and other essential medical services. Medicare - The Backbone of Senior Healthcare: In the United States, Medicare stands as a cornerstone for healthcare coverage for individuals aged 65 and older. This federal health insurance program is divided into different parts, each catering to specific healthcare needs: 1.Medicare Part A (Hospital Insurance): Part A primarily covers inpatient hospital stays, skilled

nursing facility care, hospice care, and some home health care services. Most seniors qualify for premium-free Part A if they or their spouse paid Medicare taxes while working. 2.Medicare Part B (Medical Insurance): Part B covers outpatient care, doctor visits, preventive services, and some home health care. While Part B requires a monthly premium, it is essential for comprehensive healthcare coverage. 3.Medicare Part C (Medicare Advantage): Offered by private insurance companies approved by Medicare, Part C combines Part A and Part B coverage and often includes additional benefits, such as vision and dental coverage. Seniors must have Part A and Part B to enroll in a Medicare Advantage plan. 4.Medicare Part D (Prescription Drug Coverage): This part provides prescription drug coverage, which is crucial for seniors who rely on

medications to manage their health conditions. Part D plans are offered by private insurance companies and can be added to Original Medicare or included in some Medicare Advantage plans. Supplemental Insurance (Medigap): While Medicare covers a substantial portion of healthcare costs, it doesn't cover everything. To bridge the gaps in coverage, many seniors opt for Medigap plans. Medigap, or Medicare Supplement Insurance, is offered by private insurers and helps pay for out-of- pocket costs such as deductibles, coinsurance, and copayments. There are several standardized Medigap plans, each offering different levels of coverage, allowing seniors to choose the one that best suits their needs and budget. Health Maintenance Organization (HMO) and Preferred Provider Organization (PPO) Plans:

Apart from Medicare and Medigap, seniors can explore Medicare Advantage plans, which often come in the form of HMOs or PPOs. These plans are offered by private insurers and provide an alternative to traditional Medicare. HMOs typically require members to choose a primary care physician and obtain referrals to see specialists, while PPOs offer more flexibility in choosing healthcare providers but come with higher out-of-pocket costs. Long-Term Care Insurance: One often overlooked aspect of senior healthcare planning is long-term care. Long-term care insurance helps cover the costs associated with extended periods of assistance with daily activities, such as bathing, dressing, and eating. As seniors may require long-term care services due to chronic illnesses or disabilities, having this type of insurance can provide financial

relief and ensure access to quality care without depleting savings. Conclusion: Navigating the myriad of health insurance options for senior citizens can be overwhelming, but it is an essential aspect of securing a healthy and financially stable retirement. Understanding the unique healthcare needs of seniors and exploring the various insurance plans available, including Medicare, Medigap, Medicare Advantage, and long-term care insurance, allows individuals to make informed decisions tailored to their specific circumstances. By taking proactive steps to ensure comprehensive health coverage, seniors can enjoy their golden years with peace of mind, knowing they have the necessary support to face any health challenges that may arise.