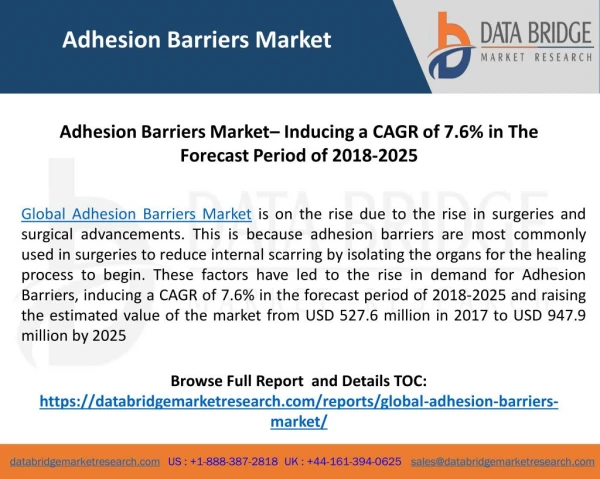

Global Adhesion Barrier Market – Analysis and Forecast (2018-2024)

Adhesion barrier is used to reduce the risk of internal adhesion formulation after the surgery. The global adhesion barrier market is growing at a significant rate, due to expanding geriatric population and surge in a number of surgeries. Different product contributed to the adhesion barrier market size. The market has witnessed high demand for synthetic adhesion barrier in the coming years due to its benefits such as bioabsorbable properties and cost-effectiveness, a huge amount of commercially accessible synthetic adhesion barriers and greater consumption of adhesion barrier by surgeons in several surgeries. Market Segmentation Insight by Product On the basis of product, the adhesion barrier market is subdivided into natural adhesion barriers and synthetic adhesion barriers. Of both products, synthetic adhesion barriers segment accounted the largest share and is expected to grow at the fastest rate in the adhesion barrier market, due to its benefits such as bioabsorbable properties, biocompatible, and cost-effectiveness, a huge amount of commercially accessible synthetic adhesion barriers and greater consumption of adhesion barrier by surgeons in several surgeries. The natural adhesion barriers are further subdivided into fibrin and collagen & protein. In addition, synthetic adhesion barriers are further subdivided into hyaluronic acid, polyethylene glycol, regenerated cellulose, and other synthetic adhesion barriers Insight by Formulation On the basis of formulation, the market is subdivided into film formulations, gel formulations, and liquid formulations. Escalating number of surgeries, clinical confirmation defending the safety and efficiency of these forms, and greater implementation of film form adhesion barrier by surgeons due to low cost are some of the factors responsible for the growth of the film formulation. Of all the formulation, the film formulation accounted foremost share in the adhesion barrier market. Insight by Application On the basis of application, the market is subdivided into gynecological surgeries, neurological surgeries, reconstructive surgeries, cardiovascular surgeries, urological surgeries, general/abdominal surgeries, orthopedic surgeries, and other surgeries. The mounting number of C-section, pelvic cancer, and hysterectomy surgeries, intensifying occurrence of conditions such as infertility and incontinence, and escalating implementation of film-form and gel-form adhesion barriers for open and laparoscopic gynecological surgeries are the factors growing the demand of gynecological surgeries application. Among all applications, the gynecological surgeries application accounted the largest share in the adhesion barrier market. Industry Dynamics Growth Drivers Expanding the geriatric population, mounting alertness about the medical inference of post-surgical adhesion formulation, and a surge in the number of surgeries and sport-related injuries are the primary growth drivers for the adhesion barrier market. For instance, according to the World Health Organization (WHO), globally in 2010 approximately 524 million people were aged 65 years and older and is expected to reach 1.5 billion in 2050. The mounting occurrence of chronic diseases owing to geriatric population, escalating and epidemiological shift from infectious to chronic diseases are also facilitating the growth for the adhesion barrier market. Owing to the mounting occurrence of chronic disease has resulted in the number of surgeries performed globally, which damages the tissues due to surgical trauma. The adhesion barriers are used in several surgical procedures to separate internal tissue and organ during the healing process. Challenges Disinclination regarding the usage of adhesion barriers amongst surgeons and strict regulations resultant in inadequate technological innovations are the major challenges for the growth of the adhesion barrier market. Industry Ecosystem Globally, the manufacturing companies trying to enter the adhesion barrier industry are required to maintain stringent regulatory standards. Moreover, the high level of capital requirement also poses a major barrier to the entry of new players. This offers an edge to the established players in the industry competition. Geographic Overview Geographically, North America is the largest adhesion barrier market as in the region the geriatric population is increasing. In addition, the mounting occurrence of chronic diseases, mounting healthcare expenditure, the surge in a number of surgical procedure, escalating number of soft tissue injuries, and firm healthcare services are also up surging growth of the North American adhesion barrier market. For instance, according to the U.S. Census Bureau, in 2012 approximately 43.1 million people were aged 65 years and older in the U.S. and is expected to reach 83.7 million in 2050. Asia-Pacific is observed to witness the fastest growth in the market, due to mounting healthcare expenditure. In addition, a mounting number of surgeries, and escalating medical tourism are also creating a positive impact on the adhesion barrier market growth in the region. Competitive Insight Key players in the adhesion barrier industry are catering to the demand of these devices by investing in technologically advanced products in their product portfolio across the globe. In October 2018, FzioMed, Inc. launched Oxiplex/IU in the European Union for intrauterine surgery to improve surgical outcomes by decreasing post-surgical adhesions. Johnson & Johnson, C. R. Bard, Inc., FzioMed, Inc., Sanofi, Anika Therapeutics, Baxter International, Inc., MAST Biosurgery, Integra LifeSciences Holdings Corporation, Getinge Group, and Betatech Medical are the key players offering adhesion barrier.

84 views • 6 slides