Download

1 / 2

20 likes | 25 Views

In the UK and in many other countries, when someone dies, their estate may be subject to tax. In most cases, that tax due is Inheritance Tax (IHT) which the family of the deceased pay on their u2018inheritanceu2019. However, in some cases, if the deceasedu2019s estate is extensive and incorporates overseas investments or properties, a family business or anything else that u2018earnsu2019 an income, Capital Gains Tax (CGT) may also be applicable.<br>How much tax on probate the family pays on a deceasedu2019s estate largely depends on its total value. The estate includes any pay-outs on life assurance policies, investment

E N D

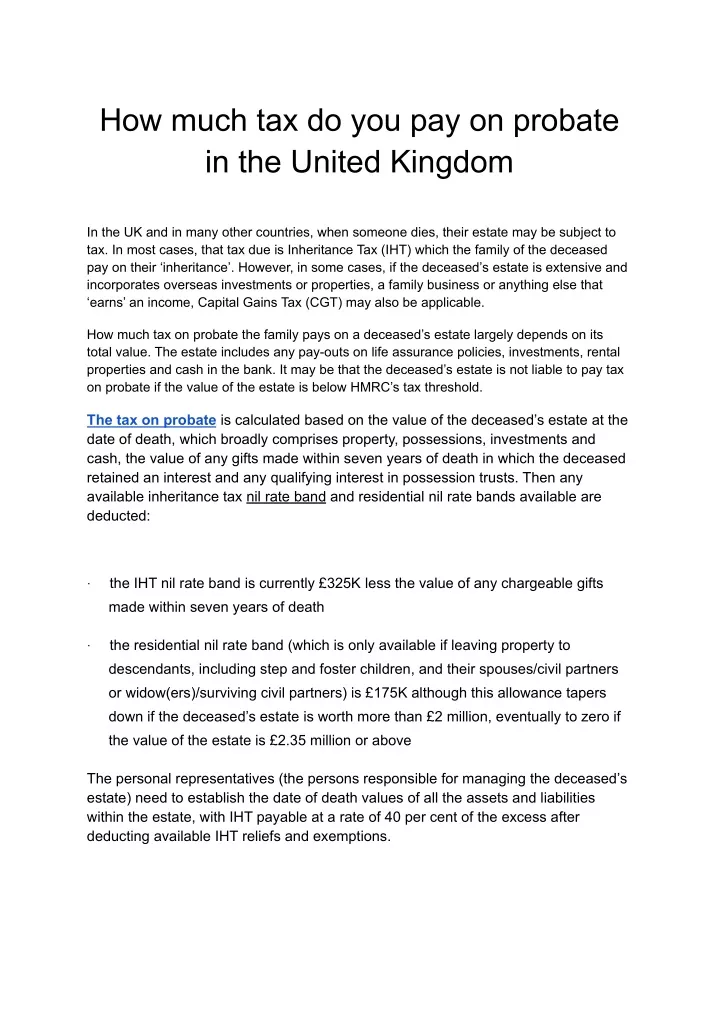

How much tax do you pay on probate in the United Kingdom In the UK and in many other countries, when someone dies, their estate may be subject to tax. In most cases, that tax due is Inheritance Tax (IHT) which the family of the deceased pay on their ‘inheritance’. However, in some cases, if the deceased’s estate is extensive and incorporates overseas investments or properties, a family business or anything else that ‘earns’ an income, Capital Gains Tax (CGT) may also be applicable. How much tax on probate the family pays on a deceased’s estate largely depends on its total value. The estate includes any pay-outs on life assurance policies, investments, rental properties and cash in the bank. It may be that the deceased’s estate is not liable to pay tax on probate if the value of the estate is below HMRC’s tax threshold. The tax on probate is calculated based on the value of the deceased’s estate at the date of death, which broadly comprises property, possessions, investments and cash, the value of any gifts made within seven years of death in which the deceased retained an interest and any qualifying interest in possession trusts. Then any available inheritance tax nil rate band and residential nil rate bands available are deducted: the IHT nil rate band is currently £325K less the value of any chargeable gifts · made within seven years of death the residential nil rate band (which is only available if leaving property to · descendants, including step and foster children, and their spouses/civil partners or widow(ers)/surviving civil partners) is £175K although this allowance tapers down if the deceased’s estate is worth more than £2 million, eventually to zero if the value of the estate is £2.35 million or above The personal representatives (the persons responsible for managing the deceased’s estate) need to establish the date of death values of all the assets and liabilities within the estate, with IHT payable at a rate of 40 per cent of the excess after deducting available IHT reliefs and exemptions.

Married couples and civil partners can transfer their assets tax free to the surviving partner. The personal representatives of the surviving partner, the second to die, can then utilise the proportion of any unused nil rate band allowances of their predeceased partner. The recipient of a gift made by the deceased within seven years of death is primarily responsible for paying any IHT on the gift.