Download

1 / 6

60 likes | 72 Views

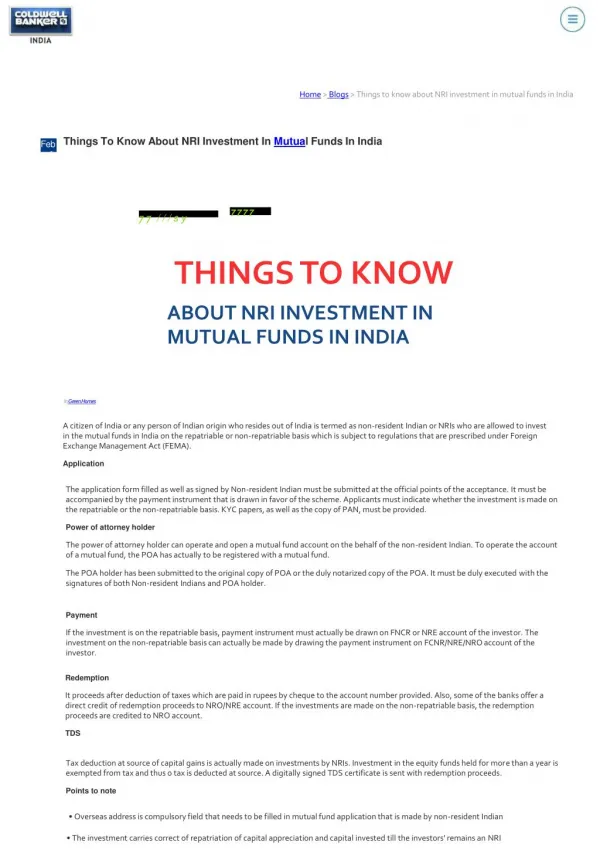

NRIs can also successfully apply for mutual funds in India from abroad. Here are a few things you need to know!

E N D

Introduction • In the recent years, mutual funds have been making their way to the top as one of the most popular instruments for investment in India. Mutual funds not only help in increasing profits over a long-term, but also give new earning members an opportunity to effectively save their money and secure a financial fund for their future. However, it is not only the domestic citizens of the country who can grasp this opportunity. Nowadays, NRIs can also successfully apply for mutual funds in India from abroad. • Although different circumstances might lead people out of the country- be it education or career prospects- every NRI drams of coming back one day and spending their retirement at home. Thus, mutual funds offer a great way to initiate an early financial planning for every Non-Resident Indians.

First off, there are certain rules are and guidelines that you must be aware of. In this context, investors from abroad need to abide by certain rules laid down by the FEMA or Foreign Exchange Management Act to activate their NRI investment services. You should know that the Asset Management Companies or AMCs in India do not accept foreign currency investments. • Thus, in order to make transactions, you must first create a Non-Resident External rupee (NRE), Non-Resident Ordinary rupee (NRO), or Foreign Currency Non-Resident (FCNR) account with an Indian bank.

Following this, you must decide if you want to carry out the transactions and investments by yourself or through a Power of Attorney. Although you have the option of investing and reviewing your portfolio through normal banking channels by yourself, it is much easier to just nominate a power of attorney (PoA). • Your PoA will be authorized by the bank to execute certain functions and take calls in your absence.

Next, you have to present certain documents as part of KYC, which essentially includes passport size photographs and certified copies of your passport, PAN card and bank statements. Along with that, you also have to submit documents legitimizing your residence outside India. Sometimes a fund house may also request for an in-person verification, for which you have to visit the nearest Indian Embassy in your residence country. • While investing, you may choose to deposit your money through a cheque or a draft. In that case, you have to attach a Foreign Inward Remittance Certificate (FIRC) or a letter authorized by the bank to confirm your fund-source.

Mutual funds are an amazing tool to diversify one’s portfolio. Within mutual funds, you may choose to allocate your money in debt funds, hybrid funds or even equity funds. Even if your risk-tolerance is low, you can still enjoy comparatively higher rates of interest by investing in any of the fixed income options like long-term debt funds in India. What’s more, nowadays you can also opt for the more convenient option of investing online. This allows every investor- domestic and NRIs- to track, review and analyze their portfolio on the go. • For overseas citizens, it is also possible to take advantage of other added benefits. To reap more revenues, make sure you regularly check the exchange rates of both your resident and home countries. If the value of the INR falls in comparison to the resident country’s currency value, investors can expect more returns during that time. You have the opportunity of getting higher returns even after factoring in any possible depreciation.