Download

1 / 20

0 likes | 20 Views

Gain valuable insights into the latest trends and outlook for the global fixed income market in March 2024. Explore global economic trends, commodity and food indexes, inflation forecasts, and 10-year sovereign yield movements in key economies. Stay informed to make informed investment decisions.<br>

E N D

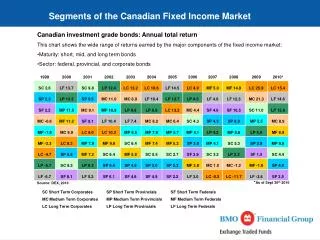

An Overview and Outlook on the Fixed Income Market March 2024 1

Global economic activity picking up JPMorgan Global PMI Global GDP by Sector Manufacturing PMI Services PMI 60.0 58.0 56.0 54.0 52.3 52.0 50.3 50.0 48.0 46.0 Jun-21 Jun-22 Jun-23 Aug-21 Aug-22 Dec-22 Aug-23 Dec-21 Dec-23 Apr-21 Apr-22 Apr-23 Oct-21 Oct-22 Oct-23 Feb-21 Feb-22 Feb-23 Feb-24 Source: Bloomberg Source: JP Morgan Economic activity is picking up from its near-term lows but expected to remain moderate in the medium term ▪ 3

Commodity & Food Index Bloomberg Commodity Index (USD) FAO Food %YoY 150 43.0 140 38.0 33.0 130 28.0 120 23.0 110 18.0 100 13.0 90 8.0 3.0 80 -2.0 70 -7.0 60 -12.0 50 -17.0 40 -22.0 Nov-20 Feb-19 Feb-20 Feb-21 Feb-22 Feb-23 Feb-24 Nov-19 Nov-21 Nov-22 Nov-23 May-19 May-20 May-21 May-22 May-23 Aug-21 Aug-19 Aug-20 Aug-22 Aug-23 Oct-19 Oct-20 Oct-21 Oct-22 Oct-23 Jan-19 Jan-20 Jan-21 Jan-22 Jan-23 Jan-24 Apr-19 Apr-20 Apr-21 Apr-22 Apr-23 Jul-21 Jul-19 Jul-20 Jul-22 Jul-23 The commodity complex has been range-bound due to weak manufacturing sector and low demand impulse from China. Shift in global rate expectations & near-term supply dynamics will be important in near term. ▪ Global food prices remained well behaved ▪ Source: Bloomberg 4

Inflation continues to moderate US UK Japan Eurozone Canada Peak CPI (%) Jan'24 CPI (%) 12.0 10.0 11.1 10.6 8.0 9.1 8.1 6.0 Oct’22 Oct'22 4.0 Jun'22 Jun’22 4.3 4.0 2.0 3.1 2.9 2.8 2.2 Jan’23 0.0 -2.0 Jul-21 Sep-21 Jul-22 Sep-22 Jul-23 Sep-23 Mar-21 Mar-22 Mar-23 Jan-21 Jan-22 Jan-23 Jan-24 May-21 May-22 May-23 Nov-21 Nov-22 Nov-23 US UK Japan Eurozone Canada ▪ Inflation continues to moderate from its peak levels across major economies. ▪ The “finalmile” of getting inflation to target down may require a higher economic impact. Central banks may cut rates but still not go all the way to pre-Covid levels till they foresee inflation moving sustainably below their “targets” Source: Bloomberg 5

10Y Sovereign yield movement in key economies Bonds fell on push back against the timing of rate cuts ▪ Source: Bloomberg, Data as of last trading day of respective months 6

Financial conditions continue to remain easy GS US Financial Conditions Index Market Implied Policy Rate Forecasts 4.9 101.0 100.8 4.7 100.6 4.5 100.4 100.2 4.3 100.0 4.1 99.8 99.6 3.9 99.4 3.7 99.2 3.5 99.0 30-Oct 15-Jan 22-Jan 29-Jan 16-Oct 23-Oct 4-Dec 14-Aug 21-Aug 28-Aug 12-Feb 19-Feb 26-Feb 11-Sep 18-Sep 25-Sep 5-Feb 6-Nov 1-Jan 8-Jan 31-Jul 2-Oct 9-Oct 18-Dec 7-Aug 4-Sep 13-Nov 20-Nov 27-Nov 11-Dec 25-Dec 12-Feb 19-Feb 26-Feb 15-Jan 22-Jan 29-Jan 28-Aug 14-Aug 21-Aug 16-Oct 23-Oct 30-Oct 5-Feb 11-Sep 18-Sep 25-Sep 4-Dec 6-Nov 1-Jan 8-Jan 31-Jul 4-Sep 2-Oct 9-Oct 7-Aug 13-Nov 20-Nov 27-Nov 11-Dec 18-Dec 25-Dec Quantum of rate cuts pushed back as economic data remains strong ▪ Source: Bloomberg 7

Domestic Growth remains strong Figures in % ▪ The second advance estimate for GDP growth in FY24 has been increased to 7.6% y/y from 7.3% previously (FY23: 7.0%) ▪ This implies 6.4% GDP growth in the final quarter (Q4 FY24) from 8.4% in Q3 FY24. ▪ Industrial healthy at ~11% vs 13.6%, reflecting healthy corporate profit growth. GVA growth has remained ▪ Services GVA growth has also picked up to a healthy 7.4% y/y vs 6.9%, with a broad- based performance across construction, public administration, transport and communication’, financial/ real estate services. ‘trade, hotels, and Source: MOSPI, BoFA, CLSA; Comm – Communication, Prof – Professional, Ser - Services 9

Household Consumption Expenditure Survey – Key Takeaways Average Nominal MPCE (INR) Rural Urban 1999-00 2004-05 2009-10 2011-12 2022-23 7000 6459 % Share of Cereals in avg MPCE % Share of Food in avg MPCE % Share of Cereals in avg MPCE % Share of Food in avg MPCE 6000 5000 CAGR: 8.5% 3773 22.23 59.4 12.39 48.06 1999-00 4000 2630 3000 17.45 53,11 9.63 40.51 2004-05 CAGR: 9.2% 1984 2000 1430 13.77 56.98 8.16 44.39 2009-10 1105 1054 855 579 1000 486 10.75 52.9 6.66 42.62 2011-12 0 6.92 47.47 4.51 39.7 2022-23 Rural Urban ▪ Consumption growth has declined between 2011-12 and 2022-23. CAGR of nominal Rural (9.2%) and Urban consumption (8.5%) is lower than 13.8% and 13.2% for the 2005-2012 period, respectively ▪ Average spending on food and beverages as a percentage of total monthly spending of a household declined from 52.9% in 2011- 12 to 46.4% in rural households, and from 42.6% in 2011-12 to 39.2% in urban households in 2022-23 ▪ Inflation could be lower by 30-40 bps if the new weights from HCES are applied Source: RBI, BoFA; MPCE – Monthly Per-capita Consumer Expenditure 10

Domestic Inflation Rates CPI and Core CPI Inflation (% YoY) CPI Diffusion Index 7.79 70% 7.44 7.41 8.0 6.83 7.5 60% 6.52 7.0 50% 6.5 5.72 5.69 5.55 40% 6.0 5.02 5.2 5.1 4.87 4.87 5.0 5.5 30% 4.7 4.6 4.31 5.0 20% 4.0 4.5 4.0 10% 3.5 0% 3.0 Jan-19 Jan-15 Jan-16 Jan-17 Jan-18 Jan-20 Jan-21 Jan-22 Jan-23 Jan-24 May-18 Sep-15 Sep-16 Sep-17 Sep-18 Sep-19 Sep-20 Sep-21 Sep-22 Sep-23 May-15 May-16 May-17 May-19 May-20 May-21 May-22 May-23 Jun-22 Jul-22 Jun-23 Jul-23 Sep-23 Sep-22 Aug-22 Aug-23 Dec-22 Dec-23 Mar-22 Apr-22 Mar-23 Apr-23 Oct-22 Jan-23 Oct-23 Jan-24 May-22 May-23 Q4FY24E Q1FY25E Q2FY25E Q3FY25E Q4FY25E Feb-23 Nov-22 Nov-23 Weight of Constinuents >= +5% RBI Estimates CPI Core CPI ▪ Consistent broad-based easing in core inflation and significant softening in commodity prices ▪ Core inflation, however, may remain moderate with manufacturing firms in RBI surveys expecting softening in the growth of input costs and selling prices ▪ The impact of the food supply shocks is likely to be absorbed by the fiscal ▪ Adequate buffer stocks for cereals and pro-active supply side interventions by the Government may keep food price pressures under check Source: Bloomberg, RBI, MOSPI, UTI Research 11

India Credit & Deposit Growth Non-food Credit Growth (%y/y) Deposits Growth (%y/y) Non-food Credit Growth (%y/y) ex HDFC Deposits Growth (%y/y) ex HDFC 21.0% 19.0% 17.0% 15.0% 13.0% 11.0% 9.0% 7.0% 5.0% 3.0% Source: Axis Capital Research; ex HDFC – excluding HDFC 12

System Liquidity System Liqudity MIBOR 300000 8.0 250000 200000 7.5 150000 System Liquidity (INR Cr) 100000 7.0 50000 MIBOR (%) 0 -50000 6.5 -100000 -150000 6.0 -200000 -250000 5.5 -300000 -350000 -400000 5.0 25-Jan 11-Jan 18-Jan 22-Feb 2-Mar 9-Mar 6-Apr 4-May 1-Jun 8-Jun 6-Jul 16-Feb 23-Feb 10-Aug 17-Aug 24-Aug 31-Aug 15-Feb 29-Feb 14-Sep 21-Sep 28-Sep 8-Feb 12-Oct 19-Oct 26-Oct 2-Nov 9-Nov 4-Jan 2-Feb 9-Feb 1-Feb 16-Mar 23-Mar 30-Mar 13-Apr 20-Apr 27-Apr 13-Jul 20-Jul 27-Jul 5-Oct 7-Dec 11-May 18-May 25-May 15-Jun 22-Jun 29-Jun 3-Aug 7-Sep 16-Nov 23-Nov 30-Nov 14-Dec 21-Dec 28-Dec ▪ RBI has been intervening through fine tuning operations to stabilize call rates with repo & reverse repo operations Source: Bloomberg, Data as of Feb 2024 13

Fiscal Trend Monthly tax & fiscal details of the central government, March fiscal year ends (INR Bn) Jan’24YTD gross tax collections rose 14.5% YoY. Direct tax collections have remained robust as both corporate taxes (20% YoY) and income taxes (27% YoY) maintained their healthy growth. Change FYTD (Apr-Jan) Change ▪ Jan-24 Jan-23 % YoY 2024 27,062 15,358 7,556 7,483 11,665 1,751 2,290 2023 23,627 12,429 6,290 5,876 11,168 1,734 2,436 % YoY Gross tax revenues Direct taxes Corporation tax Income tax Indirect taxes Customs duty Excise duty Service tax GST Net tax revenues Non-tax revenues Non-debt capital receipts 2,237 1,011 339 627 1,222 169 265 1,920 771 208 535 1,146 149 258 16.5 31 63 17.1 6.6 13.4 2.8 44 6.5 12.7 55 119 14.5 24 20 27 4.4 1.0 (6.0) 148 8.9 11.3 46 (40) Net tax revenue in 10MFY24 was at 81% of FY2024RE (11.3% higher than 10M FY23) ▪ 1 1 4.7 1.9 787 1,499 257 739 1,330 166 7,620 18,798 3,381 342 6,997 16,887 2,309 572 Expenditure, contracted during the month on the back of lower capex. In Jan 2024, total expenditure contracted 14% YoY although in FYTD terms it grew 6%. ▪ 46 21 Change FYTD (Apr-Jan) Change Jan-24 Jan-23 % YoY 2024 22,521 33,547 26,335 7,212 11,026 2,809 2023 19,768 31,676 25,978 5,699 11,908 4,521 % YoY Total receipts Total expenditures Revenue expenditure Capital expenditure Fiscal deficit Primary deficit 1,802 3,005 2,530 476 1,203 468 1,517 3,496 2,696 799 1,978 1,400 18.7 (14.0) (6.2) (41) (39) (67) 13.9 5.9 1.4 27 (7.4) (38) Source: Kotak Economics Research 14

Trade deficit moderates Monthly foreign trade aggregates (US$ bn) Change % FYTD (Apr-Jan) Change (%) Date Jan-24 Jan-23 Dec-23 YoY MoM 2024 2023 YoY Exports 36.9 35.8 38.4 3.1 (3.8) 354 372 (4.9) Oil exports 8.2 7.7 6.9 6.6 19.3 64 81 (22) Non-oil exports 28.7 28.1 31.5 2.2 (8.9) 290 291 (0.2) Imports 54.4 52.8 58.2 3.0 (6.6) 561 601 (6.7) Oil imports 16.6 15.9 14.9 4.3 10.9 147 175 (15.9) Non-oil imports 37.8 37.0 43.3 2.4 (12.6) 414 427 (2.9) - Gold Imports 1.9 0.7 3.0 174 (37) 38 29 30 Trade Balance (17.5) (17.0) (19.9) (207) (229) Lower deficit on account of softer imports across sectors, potentially hinting at weaker activity momentum ▪ Source: Kotak Institutional Equities 15

India Sovereign Curve 3M 6M 1Y 2Y 3Y 4Y 5Y 6Y 7Y 8Y 9Y 10Y 13Y 30Y 40Y 50Y 7.7 7.5 7.3 Yield (%) 7.1 6.9 29-Feb-24 31-Jan-24 28-Feb-23 6.7 6.5 20 1M Spread YoY Spread Change (Bps) 3 3 2 1 0 -2 -3 -3 -4 -4 -7 -7 -8 -8 -8 -10 -10 -11 -12 -20 -16 -28 -28 -28 -29 -30 -31 8Y -32 -33 6Y -40 -34 5Y -36 9Y 3M 6M 1Y 2Y 3Y 4Y 7Y 10Y 13Y 30Y 40Y 50Y Source: Bloomberg 16

Yields remained stable across the board on improved demand supply 3 YEAR RATES (%) 1 YEAR RATES (%) 8.48 8.46 8.62 8.42 8.40 7.97 7.89 7.88 7.91 7.80 7.77 7.35 7.32 7.33 7.15 7.11 7.06 7.03 G-SEC AAA AA T-BILL AAA AA 5 YEAR RATES (%) 10 YEAR RATES (%) 8.71 8.63 8.40 8.35 8.34 8.25 7.90 7.78 7.87 7.69 7.68 7.43 7.63 7.43 7.08 7.07 7.14 7.08 G-SEC AAA AA G-SEC AAA AA Feb-23 Jan-24 Feb-24 Source: Bloomberg, Data as on last business day of the respective months 17

Outlook ➢ With a robust view on growth and an uncertain outlook on inflation, the central banks may refrain from committing themselves to a pre-determined path ➢ Apart from near term money market instruments, bonds are more likely to be driven by the terminal rates than a change in stance or timing of the first-rate cuts ➢ With the broad phase of the repricing of expectations behind us, we believe it makes sense to look at the market construct and appropriate opportunities within the market segments ➢ With headline inflation expected to fall to 4.5% in FY25, the base case for 50-75 bps rate cuts in CY24 remains strong ➢ The high real yields today present a suitable opportunity for patient investors to experience high accrual as well as the possibility of participating in capital gains as the rate cycle turns ➢ Investors with a 6-12 months horizon can consider an allocation to low duration/ money market strategies given the considerable gap between overnight rate and money market rates (up to 12 months); Investors with more than 12 months investment horizon can consider allocation towards moderate duration (one-to-four year) categories 18

Disclaimer REGISTERED OFFICE: UTI Tower, ‘GN’ Block, Bandra Kurla Complex, Bandra E, Mumbai – 400051. Phone: 022 – 66786666. UTI Asset Management Company Ltd (Investment Manager for UTI Mutual Fund) Email: invest@uti.co.in. (CIN-L65991MH2002PLC137867). For more information, please contact the nearest UTI Financial Centre or your AMFI/NISM certified Mutual Fund Distributor (MFD) for a copy of the Statement of Additional Information, Scheme Information Document, and Key Information Memorandum cum Application Form. The information on this document is provided for information purposes only. It does not constitute an offer, recommendation, or solicitation to any person to enter any transaction or adopt any hedging, trading, or investment strategy, nor does it constitute any prediction of likely future movements in rates or prices or any representation that any such future movements will not exceed those shown in any illustration. Users of this document should seek advice regarding the appropriateness of investing in any securities, financial instruments, or investment strategies referred to in this document and should understand that statements regarding future prospects may not be realized. The recipient of this material is solely responsible for any action taken based on this material. Opinions, projections, and estimates are subject to change without notice. UTI AMC Ltd is not an investment adviser and is not purporting to provide you with investment, legal, or tax advice. UTI AMC Ltd or UTI Mutual Fund (acting through UTI Trustee Company Pvt. Ltd) accepts no liability and will not be liable for any loss or damage arising directly or indirectly (including special, incidental, or consequential loss or damage) from your use of this document, howsoever arising, and including any loss, damage or expense arising from, but not limited to, any defect, error, imperfection, fault, mistake or inaccuracy with this document, its contents or associated services, or due to any unavailability of the document or any part thereof or any contents or associated services. The information presented here is not an offer for sale within the United States of any security of UTI Asset Management Company Limited (the "Company"). Securities of the Company, including, but not limited to, its shares, may not be offered or sold in the United States absent registration under U.S. securities laws or unless exempt from registration under such laws. All complaints, regarding UTI Mutual Fund can be directed towards service@uti.co.in and for any unsatisfactory or lack of response visit www.scores.gov.in (SEBI SCORES portal) and /or visit https://smartodr.in/ (Online Dispute Resolution Portal). Mutual Fund Investments are subject to market risks, read all scheme related documents carefully. 19

Thank You 20 Mutual Fund Investments are subject to market risks, read all scheme related documents carefully.