Download

1 / 45

450 likes | 774 Views

2. Overview. Topics to be addressed:First Order of Business = Maximizing Reimbursement Must Understand and Document the Revenue Cycle Financial and Operational Influences on ReimbursementReporting Tools and AnalysisStrategies to Position the Health Center to Maximize Revenue. 3. Establishing a culture of Revenue MaximizationSetting the Health Center up for Success

E N D

1. 1

2. 2

3. 3 Establishing a culture of Revenue Maximization

Setting the Health Center up for Success � operationally

Regular Reports and Monitoring

Intervening When Necessary

4. 4 Impact of Executive Management and Board While the day to day processes of the revenue cycle are performed by dedicated health center staff, executive management and the Board play a large role in determining the success of the process by:

Establishing the proper culture of billing and collection: health centers that have a clear mandate from the board through management to bill correctly and maximize reimbursement as an organization priority do a better job of billing and collection than those who do not. This mandate plays out in management and staff goals

Maintaining a balance of financial, operational and regulatory requirements

Maintaining the overall financial health of the health center and its revenue streams

Developing and monitoring processes; intervening where appropriate

5. 5

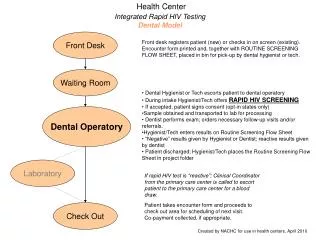

6. 6 The Revenue Cycle

7. 7

Strong internal control procedures/compliance with policies

Collection of proper billing information

Proper recording of revenue

Maintenance of subsidiary accounts receivable

Collection of information for management reporting

Satisfy Federal reporting requirements

8. 8

9. 9

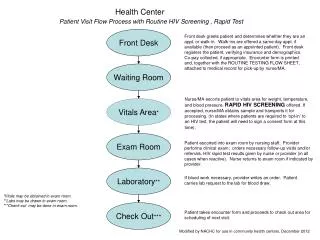

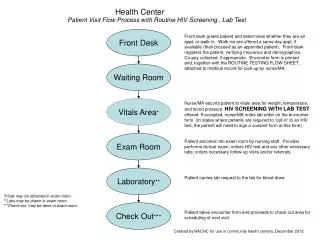

The billing cycle should include procedures at:

Front desk

Registration

Exam room (by provider)

Cashier/Appointment scheduling/Check-out

Billing

Patient accounts

Billing Cycle Procedures

10. 10

11. 11

12. 12

13. 13

14. 14

15. 15 Reporting on Patient Services Revenue and Patient Receivables On a regular basis, the finance department should produce basic reports to:

Properly Monitor the Accounts Receivable

Evaluate Collection Efforts

Monitor Billing Efforts

Maximize Collections

Evaluate if the process is working

Different levels of reporting are required based on the users:

Board of Directors

Finance Committee

Management

16. 16 High level results may be indicative of problems in the revenue cycle:

Is the Health Center making or losing money?

Is there a negative net worth?

How is working capital doing?

Are there reserves?

Cascading Down the Analysis

17. 17

18. 18 The Health Center must constantly analyze its position before it�s in trouble.

If the Health Center is making money or has a comfortable cash position, is that enough?

NO! That does not mean that it is maximizing revenue. How can we help the help center thrive, not just survive?

The billing cycle must be constantly analyzed through a standard set of clear, understandable reports.

19. 19 Board of Directors:

Commonly review monthly reports �in total�

Days in Accounts Receivable, Net

Bad Debt as a Percentage of Net Patient Services Revenue

Visit Payor Mix Analysis

Visits by Provider

Revenue Per Visit

Measures commonly compared against:

Prior periods � year over year

Budget

Industry norms � collection percentage, days in A/R, Payor Mix

Strategic or Annual Operating Plan

Reporting on Patient Services Revenueand Patient Receivables

20. 20

21. 21

22. 22 Sample Board of Directors Report on Activity

23. 23 Finance Committee:

Commonly review similar measures/ratios as Board of Directors, both in total as well as by individual payor.

Patient Receivable Agings, both in total and by payor

If significant Medicaid managed care activity:

Change in member mix and capitation revenue by actuarial class

Managed care member utilization analysis

Reporting on Patient Services Revenue and Patient Receivables

24. 24

25. 25

26. 26

27. 27 Executive Management:

Revenue report (charges, adjustments, payments)

Adjustments by payor source and type of adjustment

Aged accounts receivable reports:

In total

By payor source (and carrier/plan)

In detail

Special reports to monitor activity of billing staff

Denial report

CFO should be monitoring at least bi-weekly

28. 28

29. 29 Reasons why revenue decreases while visits increase: Analyzing Trends in Revenue

30. 30 Analyzing Shifts in Payor Mix

31. 31

32. 32

33. 33 Trends to watch for

Overall financial instability (e.g., losing money, negative fund balance)

Abnormally high bad debt percentage � or a trend of increasing bad debt

Medicaid or other payor audit results in large recoupment of payments, resulting from inaccurate coding and documentation

Days in self-pay receivables > 365

Days in Medicaid receivables > 100

Large shift in total volume, up or down

Big swings in payor mix

34. 34 Trends to watch for:

Shifts in net revenue per visit

High denial rates

Milestones/benchmarks in the billing cycle aren�t being met

Days in Medicaid receivables are higher than target

Inaccurate or incomplete coding and documentation

35. 35

36. 36 Billing and revenue strategies are intended to improve the billing and collections process in the Health Center and encourage the effective use of staff who perform these functions.

Common goals and objectives achieved through billing and revenue strategies:

Increased patient revenue.

Improved collections rates.

Reduced medical coding errors.

Cost savings of doing it right the first time.

37. 37

38. 38

39. 39

40. 40

41. 41 Eligibility/preauthorization

Claims timeliness

Complete information

Accurate information

On appropriate forms

In compliance with managed care contract/from provider manual

42. 42 Definition: Consolidating billing functions that may reside within individual sites.

Benefits: Health Centers can facilitate communication, standardize work processes, obtain economies of scale, and enhance quality control.

Select implementation tasks:

Review current billing functions organization-or network-wide.

Analyze current productivity standards.

Conduct cost-benefit analysis based on changes from decentralized to centralized billing functions including changes in �personal service� and �other than personal service� costs and savings.

Develop new policies and procedures.

43. 43

44. 44 Strategies to avoid denials

45. 45