Download

1 / 4

40 likes | 58 Views

When my friend, Tony started to reach his mid 50u2019s, the old back injuries heu2019d sustained decades ago, playing college football, started to flare up & get worse. Patrice, his wife, had been in Healthcare for her whole career & just knew as they got older & injuries & age caught up with them that theyu2019d end up forking over quite a bit of money to pay for medical bills. Theyu2019d done what most Americans do, & had a good career & funded a 401K for a few decades, but the reality is, itu2019s just not enough when you factor in health issues & unexpected expenses. They knew they needed extra financing and chose to get a Reverse Mortgage. They planned to find financial backup so that they could be prepared for anything that might come up.u202f <br>

E N D

THE ULTIMATE GUIDE TO REVERSE HOME MORTGAGE When my friend, Tony started to reach his mid 50’s, the old back injuries he’d sustained decades ago, playing college football, started to flare up & get worse. Patrice, his wife, had been in Healthcare for her whole career & just knew as they got older & injuries & age caught up with them that they’d end up forking over quite a bit of money to pay for medical bills. They’d done what most Americans do, & had a good career & funded a 401K for a few decades, but the reality is, it’s just not enough when you factor in health issues & unexpected expenses. They knew they needed extra financing and chose to get a Reverse Mortgage. They planned to find financial backup so that they could be prepared for anything that might come up.

Likewise, if you’re hitting your retirement years and you don’t want to, or can’t touch your lifetime savings yet, a reverse mortgage might be a lifesaving option for you like it was for Tony & Patrice.

Let me explain a little more what a reverse mortgage is, and how it works. WHAT IS A REVERSE MORTGAGE? A reverse mortgage is an FHA insured loan allowing homeowners who are 62 years and above to get financing with no monthly repayments. Seniors can take advantage of a reverse mortgage and pay off a normal mortgage or use the equity in their home to finance their retirements. While a Conventional loan lets the homeowners access funds to purchase a property, a reverse mortgage works oppositely. This means that a reverse mortgage will let you withdraw a portion of the equity in a property that you already own, & there’s no repayment required on the reverse mortgage provided the homeowner keeps living in that property. HOW DOES A REVERSE MORTGAGE WORK? How much can you borrow? Although we’ve explained that reverse mortgage allows you to borrow against your home’s equity, you may not be able to borrow the full value of your property! But don’t let that discourage you, our friendly & knowledgeable Loan Officers go out of their way to find as many options as they can to help you get the financing you need. The amount that can be borrowed depends on the following: Current interest rates Age of the youngest borrower or the eligible nonborrowing spouse The appraised property value The FHA set reverse mortgage limit How will the amounts borrowed be paid out? The options for how to accept the borrowed funds vary depending on a few things. If the homeowner opts for a fixed interest rate, then they’ll be limited to receiving a single disbursement or a lump sum payment. But if you chose a reverse mortgage with a variable interest rate, then some of the options include: Equal monthly payments so long as the property is a primary residence or at least one of the homeowners live in the property. Equal monthly payments for a fixed period of months that can be agreed upon ahead of time Choose a line of credit until the amount is exhausted Combination of line of credit plus fixed monthly payments for a set length of time Reverse mortgage repayment info

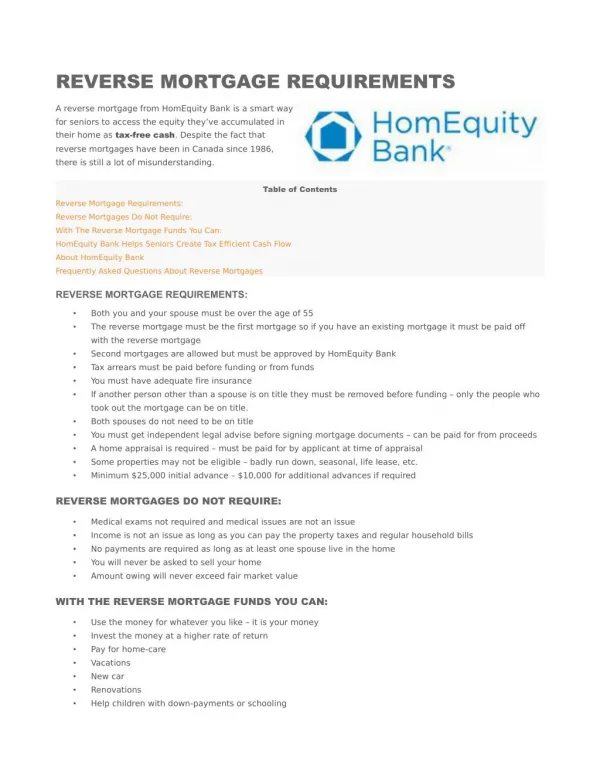

The money borrowed via a reverse mortgage does not need to be repaid until the homeowner has passed on, or when the homeowner lives away for a period exceeding nine months or opts to move out. Note that the homeowner is protected from paying more than the amount borrowed in case the property value increases. If the property value at repayment time is higher than the amount borrowed, you or your heirs can keep the difference. WHAT DO I HAVE TO DO TO QUALIFY FOR A REVERSE MORTGAGE? Now that you understand a little better what the reverse mortgage is, you’re probably wondering how to apply for one. Like I mentioned above, you do need to be 62 or older, but even if your spouse isn’t 62 yet, you can still apply for one! There are some additional requirements, such as: Prove that you own the property outright Agree to pay off any outstanding mortgage balances Property must be your primary residence and remain your primary residence. Keep up on the property taxes, homeowner’s insurance premiums, resident association fee’s and other obligations, such as maintenance & whatnot. WHAT MAKES A REVERSE MORTGAGE A BETTER OPTION COMPARED TO DIFFERENT HOUSING LOANS? The borrower is not obliged to make monthly repayments towards the loan balance The funds can be used on different living expenses, as debt repayment or even paying your healthcare expenses It is a convenient option if you are looking for the best approach for financing your retirement Non borrowing spouse is allowed to live in the home after the borrower is dead Enjoy quick disbursement, as requirements are less strict compared to conventional Utah home mortgage options Are you looking for the best Reverse home mortgage lenders in Utah? Come to Staples Group for quick and efficient reverse mortgage application process. View & DOwnload Source https://www.staplesgroupmortgage.com/the-ultimate-guide-to-reverse-home-mortgage/