Download

1 / 12

0 likes | 34 Views

While the convenience and speed of card payments are undeniable, merchants must navigate a complex web of credit card payment processing fees and rates. Visit us at: https://webpays.com/best-credit-card-payment-companies.html

E N D

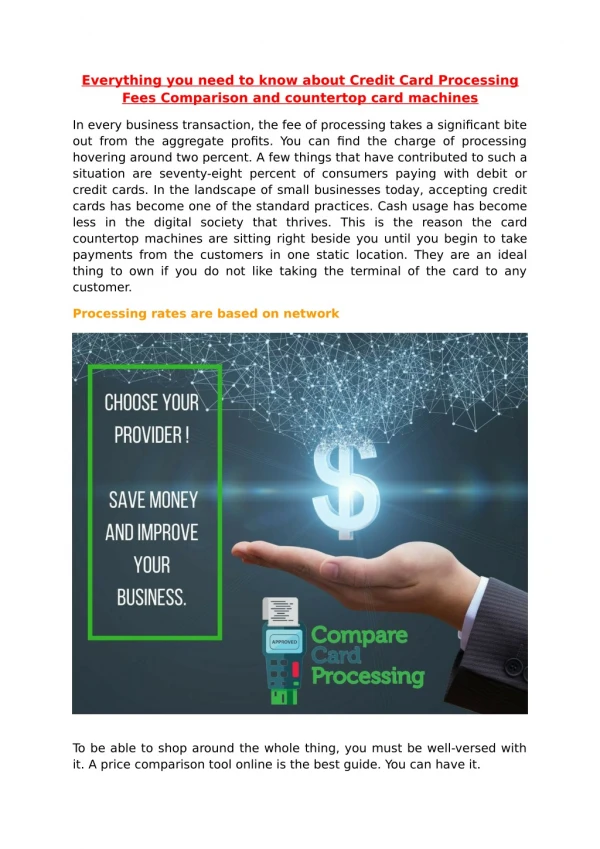

An Introduction In the ever-evolving landscape of commerce, credit card transactions have become a staple for businesses of all sizes. While the convenience and speed of card payments are undeniable, merchants must navigate a complex web of credit card payment processing fees and rates. These charges, imposed by payment processors, financial institutions, and card networks, play a crucial role in the overall cost of accepting credit card payments. In this comprehensive guide, we'll delve into the common credit card payment processing fees and rates charged by some of the best credit card payment companies that businesses encounter, demystifying the intricacies of the payment ecosystem.

1. Interchange Fees: The Foundation of Transaction Costs Interchange fees are at the core of credit card processing costs. Set by card networks like Visa, Mastercard, and Discover, these fees are paid by the acquiring bank (merchant's bank) to the issuing bank (customer's bank) for each transaction. Interchange fees are influenced by factors such as card type, transaction method (swiped, keyed, or online), and the level of risk associated with the transaction.

2. Assessment Fees: Contributions to Card Network Maintenance Card networks charge assessment fees, which are typically a percentage of the transaction value. These fees contribute to the maintenance and development of the card network infrastructure. Merchants pay these fees to the card networks, and they vary based on the type and size of the business.

3. Merchant Account Fees: Gateway to Payment Processing To accept credit card payments, merchants need a merchant account. Merchant account fees encompass various charges, including account setup fees, monthly fees, and statement fees. Acquiring banks or payment processors impose these fees to cover the administrative costs associated with maintaining merchant accounts.

4. Transaction Fees: The Cost of Each Swipe or Dip For every credit card transaction, merchants incur transaction fees. These fees cover the processing of each individual transaction and can vary based on factors such as the type of card (debit or credit) and how the transaction is processed (swiped, dipped, or keyed).

5. Monthly Statement Fees: Keeping Track of Finances To receive a monthly summary of their credit card processing activity, merchants often pay monthly statement fees to the best credit card payment companies. This fee covers the cost of generating and sending detailed statements, providing a breakdown of transactions, fees, and other relevant information.

6. Chargeback Fees: Addressing Disputes and Reversals Chargebacks occur when a customer disputes a transaction, leading to a reversal of funds. Chargeback fees are imposed by payment processors to cover the administrative costs associated with managing the dispute resolution process. Merchants may also face financial consequences if chargeback rates exceed acceptable thresholds.

7. PCI Compliance Fees: Safeguarding Cardholder Data Payment Card Industry Data Security Standard (PCI DSS) compliance is crucial for protecting cardholder data. Merchants that accept credit card payments must adhere to PCI standards, and some processors charge PCI compliance fees to cover the costs of maintaining a secure payment environment.

8. Batch Processing Fees: Settling Daily Transactions At the end of each business day, merchants settle their credit card transactions in a process known as batch processing. Some processors charge batch processing fees, covering the costs associated with settling and reconciling daily transactions.

Conclusion In the complex landscape of credit card payment processing levied by the best credit card payment companies, understanding common fees and rates is essential for businesses seeking financial efficiency and success. By navigating the fee landscape strategically, negotiating rates, and implementing best practices, merchants can optimize their credit card payment processing operations and enhance their overall financial well-being. As the payment ecosystem continues to evolve, businesses that stay informed and proactive in managing credit card processing fees will be better positioned for sustained growth and success in the competitive marketplace.