Download

1 / 12

190 likes | 853 Views

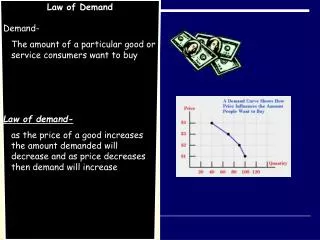

Law of Demand. When all other things are equal, as prices increase, the quantity demanded decreases due to the income effect and substitution effect. Price is the cause, changes in quantity demanded is the effect. Price and quantity have an inverse relationship when discussing demand.

E N D

Law of Demand • When all other things are equal, as prices increase, the quantity demanded decreases due to the income effect and substitution effect. • Price is the cause, changes in quantity demanded is the effect. • Price and quantity have an inverse relationship when discussing demand.

Law of Supply • All other things being equal, as prices increase, the quantity supplied increases because producers have a greater willingness and ability to bring products to market. • Price is the cause, changes in quantity supplied is the effect. • Price and quantity have a direct relationship when discussing supply.

Market Price • The market price is the price at which the quantity demanded and the quantity supplied are equal to one another. • If supply and demand are equal there is obviously no surplus nor shortage. The makes the market price the ideal price or the “happy place” • Both producers and consumers benefit when a market can achieve “equilibrium.”

Change in Demand(shifts in the demand curve) • Change in demand occurs when demand changes at each and every price in the market. Something other than price becomes the cause of changes in quantity being demanded at each price. • Possible causes: • Seasonal changes • Change in the # of consumers • Changes in cost or availability of related products • Change in income • Trends, tastes, preferences or fads • Future expectations

Change in Supply(shifts in the supply curve) • Change in supply occurs when supply changes at each and every price in the market. Something other than price becomes the cause of changes in quantity being supplied at each price. • Possible causes: • Change in the cost of inputs • Change in the number of producers • Change in technology

Price Controls • Normally, the government in a market economy will allow the consumers and producers to interact and establish the market price without intervention. • There are, however, instances where the government feels it is in the best interest of the society to intervene on behalf of the consumers or even on behalf of the producers.

Price Ceilings • Intervention on behalf of the consumer. • The market price is thought to be too high. • A price cap or ceiling is put in place to keep the price below the market price. • Price ceilings create shortages.

Price Floors • Intervention on behalf of the producer. • The market price is thought to be too low. • A price floor is put in place to keep the price above the market price. • Price floors create surpluses.

Elasticity • Measure of responsiveness to price changes. • According to the laws of demand, quantity demanded responds to price changes. • Elasticity measures that response. • The greater the response to a price change the more elastic a product is.

Elasticity • Measure of responsiveness to price changes. • Why does it matter? • It helps in the decision making process for establishing prices. For instance you would expect the quantity demanded to increase when you decrease the price, right? But, will the increase in quantity demanded be enough to recover the decrease in price? • Another example of the usefulness of understanding the concept of elasticity is when price controls should be used. The extent of shortages and surpluses caused by price controls is determined by the elasticity of the product involved. • For consumers! If consumers have some understanding of the elasticity of a product one can determine whether a sale on that product makes an opportune time for a purchase.

Elasticity • Characteristics of the product combine determine the product’s elasticity. • Expense of the product. • Is the product a necessity or luxury? • Are there many substitutes available for the product? • Can you delay the purchase of the product?

Elasticity • Measuring elasticity • PEoD = (% Change in Quantity Demanded) (% Change in Price) • If PEoD > 1 then Demand is Price Elastic (Demand is sensitive to price changes) • If PEoD = 1 then Demand is Unit Elastic(one for one change) • If PEoD < 1 then Demand is Price Inelastic (Demand is not sensitive to price changes) Finding % change new-original/original