Download

1 / 9

160 likes | 890 Views

Money Multiplier M = m MB (Money Supply = multiplier x Monetary Base, where MB = Currency + Reserves) Deriving Money Multiplier R = RR + ER , (Reserves = Req. Res. + Excess Res.) RR = r D, (Req. Res. = reserve ratio x Deposits) R = ( r D ) + ER

E N D

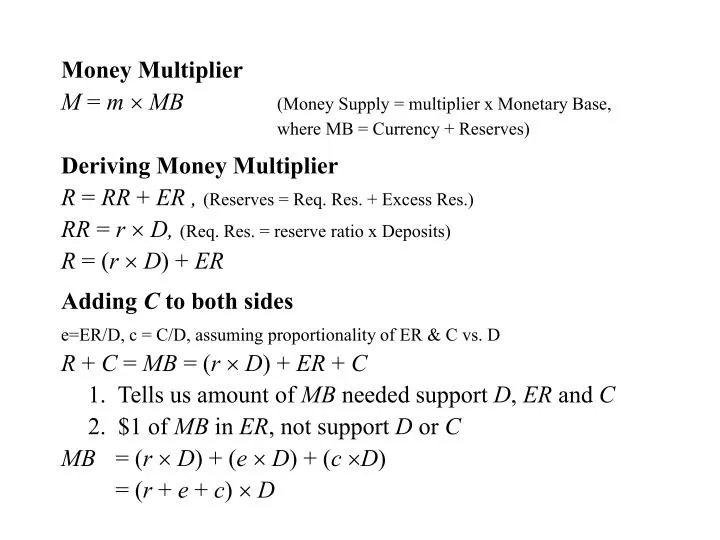

Money Multiplier M = mMB (Money Supply = multiplier x Monetary Base, where MB = Currency + Reserves) Deriving Money Multiplier R = RR + ER , (Reserves = Req. Res. + Excess Res.) RR = rD, (Req. Res. = reserve ratio x Deposits) R = (rD) + ER Adding C to both sides e=ER/D, c = C/D, assuming proportionality of ER & C vs. D R + C = MB = (rD) + ER + C 1. Tells us amount of MB needed support D, ER and C 2. $1 of MB in ER, not support D or C MB = (r D) + (e D) + (cD) = (r + e + c) D

1 D = MB r + e + c M = D + (cD ) = (1 + c) D 1 + c M = MB r + e + c 1 + c m = r + e + c m < 1/r because no multiple expansion for currency and because as DER Changes dm/dc, dm/de, dm/dr? Full Model M = m (MBn + DL), where MBn is non-borrowed MB and DL are discount loans

Determinants of e 1. i, relative Re on ER (opportunity cost ), e 2. Expected deposit outflows, ER insurance worth more, e Excess Reserves Ratio