Download

1 / 20

230 likes | 352 Views

Treatment of Uncertainty in Economics (I). Economics 331b. This week. Dynamic deterministic systems Dynamic stochastic systems Optimization (decision making) under uncertainty Uncertainty and learning Uncertainty with extreme distributions (“fat tails”).

E N D

Treatment of Uncertaintyin Economics (I) Economics 331b

This week • Dynamic deterministic systems • Dynamic stochastic systems • Optimization (decision making) under uncertainty • Uncertainty and learning • Uncertainty with extreme distributions (“fat tails”)

Deterministic dynamic systems (no uncertainty) Consider a dynamic system: • yt = H(θt , μt ) where yt = endogenous variables θt = exogenous variables and parameters μt = control variables H = function or mapping.

Deterministic optimization Often we have an objective function U(yt ) and want to optimize, as in max ∫ U(yt )e-ρtdt {μ(t)} Subject to yt = H(θt , μt ) As in the optimal growth (Ramsey) model or life-cycle model of consumption.

Stochastic dynamic systems (with uncertainty) Same system: • yt = H(θt , μt ) θt = random exogenous variables or parameters Examples of stochastic dynamic systems? Help?

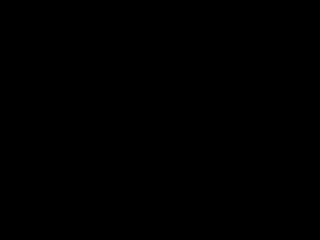

Which is stock market and random walk? T=year 0 T=year 60

Examples: stock market and random walk Random walk US stock market

How can we model this with modern techniques? Methodology is “Monte Carlo” technique, like spinning a bunch of roulette wheels at Monte Carlo

How can we model this with modern techniques? Methodology is “Monte Carlo” technique, like spinning a bunch of roulette wheels at Monte Carlo System is: • yt = H(θt , μt ) So, • You first you find the probability distribution f(θt ). • Then you simulate (1) with n draws from f(θt ). • This then produces a distribution, g(yt ).

YEcon Model An example showing how the results are affected if we make temperature sensitivity a normal random variable N(3, 1.5).

How do we choose? • We have all these runs, ytI , ytII , ytIII ,… • For this, we use expected utility theory. max ∫ E[U(yt )]e-ρtdt Subject to yt = H(θt , μt ) and with μt as control variable. • We usually assume U( . ) shows risk aversion. • This produces an optimal policy.

SCC 2015 So, not much difference between mean and best guess. So we can ignore uncertainty (to first approximation.) Or can we? What is dreadfully wrong with this story?

What is dreadfully wrong with this story? The next slide will help us think through why it is wrong and how to fix it. It is an example of • 2 states of the world (good and bad with p=0.9 and 0.1), • and two potential policies (strong and weak), • and payoffs in terms of losses (in % of baseline utility or income).