Download

1 / 17

170 likes | 184 Views

Learn about short hedges and hedging with stock index futures to offset market losses and generate gains. Explore different hedging approaches and their impact on portfolio value.

E N D

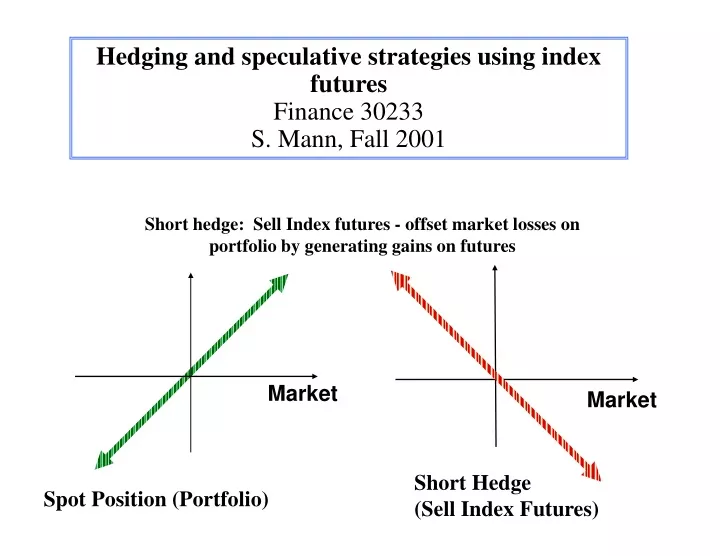

Hedging and speculative strategies using index futures Finance 30233 S. Mann, Fall 2001 Short hedge: Sell Index futures - offset market losses on portfolio by generating gains on futures Market Market Short Hedge (Sell Index Futures) Spot Position (Portfolio)

Example: Portfolio manager has well-diversified $40 million stock portfolio, with a beta of 1.20 Hedging with Stock Index futures 1 % movement in S&P 500 Index expected to induce 1.20% change in value of portfolio. Scenario: Manager anticipates "bear" market (fall in value), and wishes to hedge against possibility. One Solution: Liquidate some or all of portfolio. (Sell securities andplace in short-term debt instruments until "prospects brighten") • Broker Fees • Market Transaction costs (Bid/Ask Spread) • Lose Tax Timing Options (Forced to realize gains and/or losses) • Market Impact Costs • If portfolio large, liquidation will impact prices

Assume you hedge using the June 02 S&P 500 contract, currently priced at 920. The contract multiplier is $250 per point. Naive Short hedge: dollar for dollar Dollar for dollar hedge: find number of contracts: V $40,000,000 P = = 174 contracts V (920) ($250) F where: V = value of portfolio P V = value of one futures contract F

hedge initiated November 15, 2001, with Index at 900. If S&P drops 5% by 2/2/02 to 855, predicted portfolio change is 1.20 (-5%) = -6.0%, a loss of $2.4 million But: portfolio has higher volatility than S&P 500 Index ( portfolio beta=1.20) Date Index Spot position (equity) futures position 11/15/01 900 $40,000,000 short 174 contracts 2/2/02 855 $37,600,000 futures drop 45 points -45 -$2,400,000 gain = (174)(45)(250) = $1,957,500 Net loss = $ 442,500 Assumes: 1) portfolio moves exactly as predicted by beta 2) futures moves exactly with spot

Estimate Following regression: Estimating Minimum Variance Hedge ratio spot returnt = a + bSFFutures ‘return’t + et Portfolio Return x x xx x x x x x intercept = a{ x xxx x x Futures ‘return’ (% change) x x x xx x x x x xx x line of best fit (slope = bSF )

Hedge using June 02 S&P 500 contract, currently priced at 920 [ 920 900 ( 1 + r - d)t ] Calculating number of contracts for minimum variance hedging Minimum variance hedge number of contracts: VP $40,000,000 = 208 contracts bPF = (1.20) VF (920) ($250) where: VP = value of portfolio V = value of one futures contract F bPF = beta of portfolio against futures

hedge initiated November 15, 2001, with Index at 900. If S&P drops 5% by 2/2/02 to 855, predicted portfolio change is 1.20 (-5%) = -6.0%, a loss of $2.4 million Minimum variance hedging results Date Index Spot position (equity) futures position 11/15/01 900 $40,000,000 short 208 contracts 2/2/02 855 $37,600,000 futures drop 45 points -45 -$2,400,000 gain = (208)(45)(250) = $2,340,000 Net loss = $ 60,000 Assumes: 1) portfolio moves exactly as predicted by beta 2) futures moves exactly with spot ( note: futures actually moves more than spot : F = S (1+c) )

DefinebPFas portfolio beta (against futures) Altering the beta of a portfolio Change market exposure of portfiolio tobnew by buying (selling): VP (bnew - bPF ) contracts VF VF = value of one futures contract VP = value of portfolio where:

Return on Portfolio Original Expected exposure Impact of synthetic beta adjustment Expected exposure from reducing beta Return on Market Expected exposure from increasing beta

Begin with $40,000,000 portfolio:bPF = 1.20 Prefer a portfolio with 50% of market risk (bNew=.50) Hedge using June 02 S&P 500 contract, currently priced at 920. Changing Market Exposure: Example V $40,000,000 P (bNew- bPF) = (.50 - 1.20) V (920) ($250) F = - 122 contracts

hedge initiated November 15, 2001, with Index at 900. If S&P drops 5% by 2/2/02 to 855, predicted portfolio change is 1.20 (-5%) = -6.0%, a loss of $2.4 million. predicted loss for bP =0.5 is (-2.5% of $40 m) = $1 million Reducing market exposure: results Date Index Spot position (equity) futures position 11/15/01 900 $40,000,000 short 122 contracts 2/2/02 855 $37,600,000 futures drop 45 points -45 -$2,400,000 gain = (122)(45)(250) = $1,372,500 Net loss = $ 1,027,500 Assumes: 1) portfolio moves exactly as predicted by beta 2) futures moves exactly with spot ( note: futures actually moves more than spot : F = S (1+c)

Portfolio manager expects sector to outperform rest of market ( a> 0) Sector "alpha capture" strategies Portfolio Return x x xx x x x x x intercept = a{ x xxx x x Futures ‘return’ (% change) x x x xx x x x x xx x line of best fit (slope = b )

Expected exposure with "hot" market sector portfolio Return on Sector Portfolio "Alpha Capture" } a > 0 0 Return on Market Slope = bSF = beta of sector portfolio against futures

Expected exposure with "hot" market sector Return on Asset "Alpha Capture" Expected return on short hedge } expected gain on alpha 0 Return on Market

Assume $10 m sector fund portfolio withb = 1.30 You expect Auto sector to outperform market by 2% Eliminate market risk with minimum variance short hedge. (using the June 02 S&P 500 contract, currently priced at 920) Alpha Capture example The desired beta is zero, and the number of contracts to buy (sell) is: V $10,000,000 P (bNEW- bSF) = (0 - 1.30) V (920) ($250) F = - 56 contracts

hedge initiated November 15, 2001, with Index at 900. If S&P drops 5% by 2/2/02 to 855, predicted portfolio change is 1.30(-5%) + 2% = -4.5%, a loss of $450,000. Alpha capture: market down 5% Date Index Spot position (equity) futures position 11/15/01 900 $10,000,000 short 56 contracts 2/2/02 855 $9,550,000 futures drop 45 points -45 - $450,000 gain = (56)(45)(250) = $630,000 Net GAIN = $ 180,000 Assumes: 1) portfolio moves exactly as predicted by beta 2) futures moves exactly with spot ( note: futures actually moves more than spot : F = S (1+c))

hedge initiated November 15, 2001, with Index at 900. If S&P rises 5% by 2/2/02 to 945, predicted portfolio change is 1.30( 5%) + 2% = 8.5%, a gain of $850,000. Alpha capture: market up 5% Date Index Spot position (equity) futures position 11/15/01 900 $10,000,000 short 56 contracts 2/2/02 945 $10,850,000 futures rise 45 points 45 $850,000 loss = (56)(45)(250) = $630,000 Net GAIN = $ 220,000 Assumes: 1) portfolio moves exactly as predicted by beta 2) futures moves exactly with spot ( note: futures actually moves more than spot : F = S (1+c))