Download

1 / 16

160 likes | 486 Views

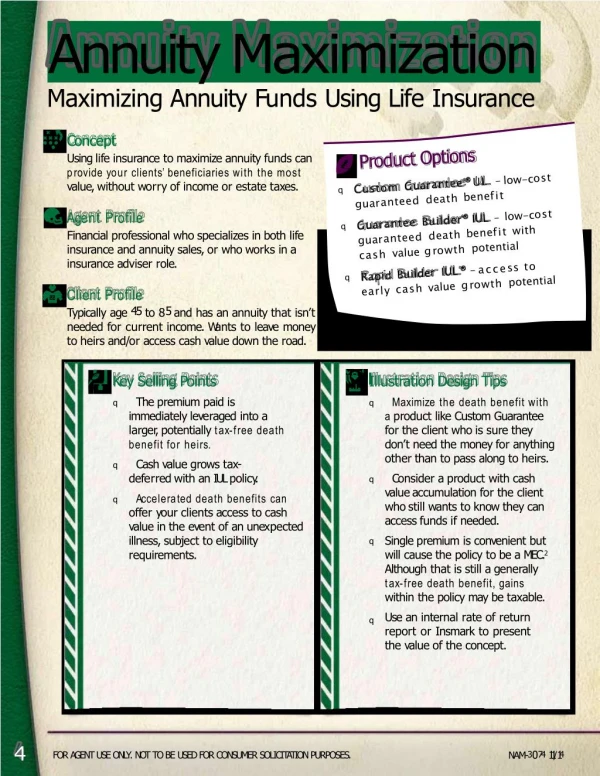

Annuity Maximization . . . A strategy designed to maximize the wealth transferred to heirs. Initial Client Presentation This Presentation has been prepared Expressly for: Client Name Date By Producer or Member Firm. Deferred Annuities. Are an excellent wealth accumulation vehicle

E N D

Annuity Maximization. . . A strategy designed to maximize the wealth transferred to heirs Initial Client Presentation This Presentation has been prepared Expressly for: Client Name Date By Producer or Member Firm

Deferred Annuities • Are an excellent wealth accumulation vehicle • Investment gains accumulate tax-deferred until distributed • Are a tax-inefficient wealth transfer vehicle • Death benefit is includable in taxable estate • Death benefit over basis is income in respect of a decedent (IRD) and subject to income tax • The combined tax effect may consume 70% or more of the annuity’s value

Case Study • Male age 65, preferred non-smoker • $1,000,000 deferred annuity • $650,000 cost basis • Client in 48% estate tax bracket • Heirs in 35% income tax bracket

Current Situation at Death Value of Annuity $1,000,000 Estate tax liability ( 480,000) Income tax liability ( 63,700)* Net estate to heirs $ 456,300 *This figure takes into account the income tax deduction available for the portion of estate tax attributable to gain in the contract.

Strategy Requirements • Must have sufficient assets to support living expenses without the existing annuity • Do not plan on using the annuity for retirement income • Should be age 60 or older and in good health

Strategy Overview • Use deferred annuities to provide cash flow under one of three methods: • Annuitize the existing deferred annuity • Purchase a Single Premium Immediate Annuity (SPIA) using a 1035 exchange • Take annual withdrawals from the existing annuity

Strategy Overview • Gift the after-tax income to an Irrevocable Life Insurance Trust (ILIT)* • The ILIT is owner and beneficiary of a life insurance policy on the client’s life • Upon death the ILIT can distribute the life insurance proceeds free of income and estate taxes to heirs** * The gifts may be subject to gift taxation if they exceed the client’s available annual gift exclusions and lifetime exemption. ** If the withdrawal version is used, the remaining annuity value net of estate and income taxes will pass to heirs as well.

Benefits of Funding Alternatives • SPIA / Annuitization Version • Income stream is guaranteed for the client’s lifetime* • Tax favored income – a portion of each annuity payment is treated as a tax-free return of principle • Withdrawal Version • Maintain control and liquidity of assets** * Any guarantees offered are subject to the claims paying ability of the issuing insurance company. ** Contingent deferred sales charges may apply for withdrawals.

Proposed Strategy • Existing deferred annuity is exchanged into a single premium immediate annuity (SPIA) • Investment in SPIA = $1,000,000 • Annual annuity income = $77,288 • Initial net income and gift to ILIT = $61,328 • ILIT purchases life insurance policy with death benefit = $2,334,542

Invests in a SPIA. Annuity Provider Provides annual distributions for Client's life. Annuity Max Strategy Sample Client (1) $1,000,000 SPIA purchase

Invests in a SPIA. Annuity Provider Provides annual distributions for Client's life. Annuity Max Strategy Sample Client (1) $1,000,000 SPIA purchase (2) Receives $77,288 annually for life

Irrevocable Life Insurance Trust (ILIT) Invests in a SPIA. Acquires $2,334,532 policy on Sample Client Annuity Provider Provides annual distributions for Client's life. Annuity Max Strategy (3) Annual gifts to ILIT to pay premiums. Sample Client (1) $1,000,000 SPIA purchase (2) Receives $77,288 annually for life

Irrevocable Life Insurance Trust (ILIT) Invests in a SPIA. Acquires $2,334,532 policy on Sample Client Annuity Provider Provides annual distributions for Client's life. Annuity Max Strategy (3) Annual gifts to ILIT to pay premiums. Sample Client (4) Proceeds pass estate tax free at death (1) $1,000,000 SPIA purchase (2) Receives $77,288 annually for life Heirs Receive death benefits according to terms of ILIT

Benefit to Heirs • Estate and income tax liability of the existing deferred annuity asset is reduced or eliminated • Wealth transferred to heirs is maximized

Benefit to Heirs The Annuity Max benefits will be both estate and income tax free if structured properly within an ILIT. The current investment is subject to both estate and income taxes.

Steps to Implement Annuity Max • Provide your financial advisor with information on your • Current deferred annuity • Estate & your heir’s income tax bracket • Have your advisor prepare a custom analysis in order to determine • Cash flow required to fund the life insurance • Whether the strategy creates sufficient leverage • Determine whether to proceed • Create an ILIT • Have the Trustee apply for and be the beneficiary of life insurance on your life • Transfer/withdraw funds (annuity) to fund the premiums