Download

1 / 19

190 likes | 405 Views

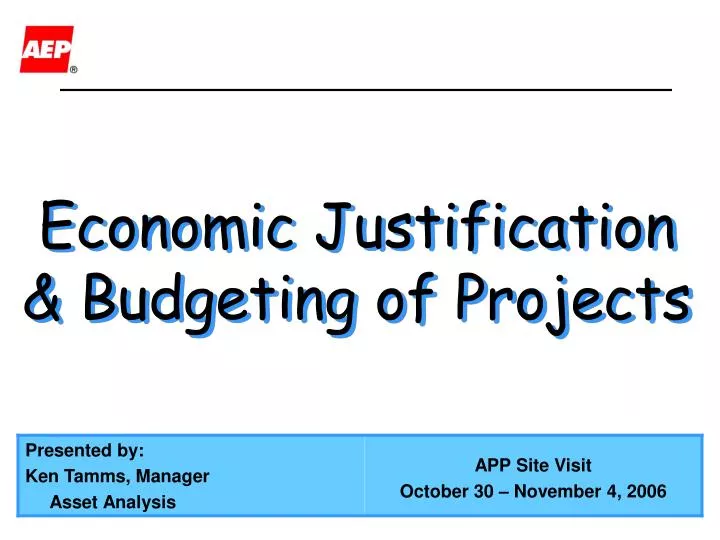

Economic Justification & Budgeting of Projects. Project Management Review Group (PMRG) Process Flow Chart. Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 . Plants identify projects and enter projects into the budgeting database (PBMS). Post Spend Opt. PMRG. LRP PMRG

E N D

Project Management Review Group (PMRG) Process Flow Chart Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Plants identify projects and enter projects into the budgeting database (PBMS) Post Spend Opt. PMRG LRP PMRG 10 yr review LRP PMRG 10 yr review LRP PMRG 10 yr review Planning & Budgeting Cycle Spend Opt. 2-3 yr review Spend Opt. 2-3 yr review Spend Opt. 2-3 yr review Budget 2 yrs data Budget 2 yrs data Budget 2 yrs data Capital Investments are Reviewed in PMRG Board Meetings (includes planned & emergent work) Meetings to be held at least 2 months prior to required equipment order date* Project Execution Final Authorization & Execution Post Project review (select projects) Indicates a single advisory meeting * - A process improvement is in development, whereby PMRG meetings will be scheduled at least two years prior to the required in-service date

Budget Detail - Categories • Capital Investments– Includes outage and non-outage investments including the cost of removal. • Non-Capital Expense • Expenses associated with operations and maintenance (O&M), administration & support • Expense or revenue associated with fuel handling and sales/disposal of by combustion products. • Fuel Forecasts- Cost of fuel (coal, gas, oil) used for generation. • All budget categories are forecast in detail by: • Specific project when known • Accounting classification, example, Federal Energy Regulatory Commission (FERC). • 511 (Maint of Structures) 512 (Maint of Boiler), etc. • Resource (e.g. labor, material, equip rental, etc.) • Project Type (grouping which aids in defining areas of spend)

Budget Detail - Groupings • Base Operating Cost, (Expense) • Daily operating, maintenance and fuel handling expense including plant personnel, chemicals, minor materials and routine outside services. • Non Outage Projects, (Expense) • Discretionary, defined maintenance projects which can be completed without removing a unit from service but which are NOT a typical daily operations & maintenance activity. • Example: pulverizer rebuild, pump rebuild • Outage Projects, (Expense) • Projects defined to be accomplished during a scheduled unit outage. • Blanket Projects-Outage & Non Outage, (Capital) • Defined capital projects, the estimated cost of which is less than $500k. • Discreet Investments in Equipment-Outage & Non Outage, (Capital) • Defined capital projects $500k or greater estimated cost

Budget Detail - Plant Support-(Overheads) Support group costs are assigned either on a “Direct” charge basis or are allocated based on a pre-defined methodology. Examples include: • Central & Regional Engineering • Labor (including staff augmentation) & expenses budgeted to specific projects when known otherwise to a generic support project • Other AEP Support Groups • Costs are allocated to each plant based on pre-defined attribution basis (e.g. rated megawatt capability, number of employees, etc.) • These groups include outage planning management, human resources, purchasing, accounting, legal, etc.

Project Management Review Group • The Project Management Review Group (PMRG) process was created to manage the company’s resources and to optimize the performance of the Fossil & Hydro Generation Fleet • The process addresses several key management issues: • Promotes a more forward looking planning process • Improves project assumptions and estimate quality • Challenges project inputs and creates accountability for project performance / results • Drives more efficient and timely resource management, including material procurement • Facilitates communication of issues, lessons learned, best practices, etc. PMRG Process fosters planning, accountability and communications.

Spend Optimization - Overview • Objective – As part of the PMRG process, the Spend Optimization process assists management with the allocation of capital resources across AEP’s fleet of generating units and includes a three year planning horizon. • Process Scope -To review and prioritize all capital projects greater than $500,000 based on their Financial and Non-Financial Risk impacts. • Project Scoring: • Financial Scoring is based on Net Present Value, Internal Rate of Return and Simple Payback, using discount periods of 10, 15, and 20 years depending on certain factors. • Risk Scoring includes an evaluation of the probability of negative outcomes occurring and assess the consequences associated with either deferring, accelerating or canceling the project. • Safety and/or Regulatory projects are scored outside of the financial analysis and are generally approached on a “lowest cost” basis. • For 2007, about 500 projects with a projected spend of $1.9 billion were screened through the spend optimization process.

Resource Allocation/Prioritization Process • The project justification tool is designed to work within the PMRG framework. Specific objectives are to: • Utilize the the raw budget data and identify those projects which add incremental value. • Provide input to a project ranking system, based on certain economic metrics, (Net Present Value, Internal Rate of Return and Simple Payback), which helps Management determine which capital projects should be selected. • Augment certain Business Education initiatives

Assumptions for the Prioritization Process • The Base Assumption is that the budget is linked to asset performance and ultimately rolls up to the Corporate financial forecasting model. • The analysis, as to whether the project adds value is determined by looking at the prospect of deviating from the Base Assumption versus making a planned investment in the asset. For example, consider the fact that if an investment in a particular asset is deferred, the unit will not be able to meet its performance target. In this instance, AEP would need to “replace” that asset’s contribution from the market in order to meet its Corporate projection.

Unit Input Targets • The justification tool requires that specific unit Input Targets be introduced: • Unit Characteristics • Availability (% available) • Heat Rate (MMbtu/MWh) • Unit Emission Rates, SO2, Nox, Hg, CO2, (lb/Mmbtu) • Unit Operating Range, full load, minimum load, seasonal de-rates • Variable Operating Costs • Fuel, including fuel handling, ($/mmbtu) • Emission Costs, ($/mmbtu) • Non-fuel fixed costs • Base Operating Costs • Non-Outage Costs • Outage Costs • Capital Blankets • Capital Investment Projects

Market Based Inputs • Forecasted power price curves, updated quarterly. • Forecasted replacement fuel, (coal and gas) cost curves, updated quarterly. • Forecasted credit cost projections for Nox and SO2, updated quarterly. Forecasts of power prices, replacement fuel and emission credit costs, while developed by internal experts, and shared within the organization, are developed independent of the originating group responsible for the project input assumptions.

Project Input Template • The Project Data Sheet is prepared by the originating group using a prescribed format: • Requires thought and analysis of alternative solutions, presents the probability of certain outcomes and includes a failure analysis. • Provides a concise summary of project technical assumptions and serves as a basis for screening and challenging the performance improvement and other economic impacts. • Maintains consistency among facilities.

Example Project Input Template Performance inputs are developed by Engineering using historical data analysis, experience and computer based simulation techniques.

Project Results- Output Reports • Output Reports Include: • Net Present Value, (NPV), of Incremental After Tax Cash Flow using 10, 15 & 20 year discount periods. • Internal Rate of Return, (discount rate that yields zero NPV), using 10, 15 & 20 year discount periods. • Project output and unit summary tables • Graphical representations of going forward dispatch costs and gross margins. • Incremental project summary provides the economic impact of the capital investment compared with a host of alternatives in the areas of: • Availability improvements • Efficiency improvements • Incremental Emission costs • Cost reduction improvements

Example – Project Results Following the investment in this unit, a favorable relationship is shown to exist between the market price for energy and variable operating costs suggesting long term asset viability.

2006 Capital Spend (As of January, 2006) On a per MW basis, as of January, 2006, the capital budget is focused on Nuclear and large coal plant projects