Download

1 / 16

160 likes | 195 Views

Detailed survey findings from 11 countries, showcasing agreement and divergence, emphasizing professional sharing of experiences within the PEMPAL community. Results encompass responses, comments, and potential questions for improvement and benchmarking. Insights on performance budgeting from OECD and important factors to consider for effective implementation in government contexts.

E N D

Survey Results PEMPAL Budget Community of Practice Tbilisi, Georgia

The BCOP Survey • 11 countries responded • Both great agreement (5-11) • And divergence (4-0) • This professional sharing of experience is the essence of PEMPAL THANK YOU

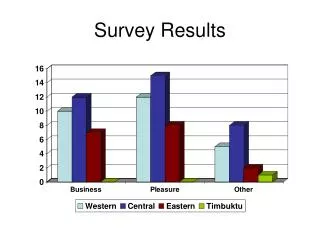

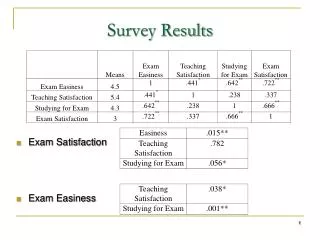

Survey Results: Responses Total 10 0 1 2 5 0

Survey Results: Comments Slovenia 4. Programs are established according… 5. Functional classification is used… 7. Program classification was used… Slovakia 10. NUMBER OF GOALS WAS LIMITED TO … 12. SLOVAK NATIONAL AUDIT OFFICE IS…

Questions/statements that might be generated: • Why did Hasobonia say “yes” on Question 6.b.? • Why are we the only one saying “yes” on Question 10.k.? • Can we use these as benchmarks? • Do we want to? • I don’t agree with some responses for our country.

In Draft Mission Statements for BCOP • Reference to working with OECD countries to identify good practices in Program Budgeting

OECD Meeting on Performance Budgeting – June 11-12, 2007 • Performance Budgeting reform: to improve decision making by providing more concrete information on what is accomplished with the money

OECD Definition • Form of budgeting that is based on a relationship between allocation and results • Beyond this there is little agreement on: • Type of information • At what stage of budgeting it should be introduced • How to relate performance information and resource allocation

Important Factors to Keep in Mind • There is no single model – countries need to adapt to relevant political and institutional contexts • Whole-of-government planning and reporting framework is important • Performance Information should be integrated into the budget process

Important Factors to Keep in Mind • Systems that automatically link performance results to resource allocation should be avoided – may distort incentives • It is often difficult to identify causes of poor performance • Must update output data continuously • Evaluations and assessments should be independent

Important Factors to Keep in Mind • It is vital to have support of political and administrative leaders • Staff capacity at the MOF and spending ministries is critical • Reforms must adapt to evolving circumstances • There must be incentives for civil servants and politicians to change behavior

3 Categories of Performance Budgeting • Presentational: • Simple display of allocation and results (targeted or realized) • Purpose: accountability • Performance-informed: • Performance information along with other factors is taken into account • Purpose: planning and accountability

3 Categories of Performance Budgeting • Direct/formula: • Funding is based on results achieved • Purpose: resource allocation and accountability [Note: Used only in specific sectors in a limited number of OECD countries. Acts like a contract]

Let's Move Ahead ! Managing Public Expenditure A Reference Book for Transition Countries Edited by Richard Allen and Daniel Tommasi PERFORMANCE BUDGETING IN OECD COUNTRIES(PRELIMINARY VERSION)ANNUAL MEETING OFTHE OECD SBO NETWORK ON PERFORMANCE AND RESULTSWASHINGTON DC11-12 JUNE 2007