Download

1 / 20

200 likes | 219 Views

Pre-treatment practices for Seasonal Adjustment Including Calendar Adjustment. Necmettin Alpay KOÇAK UNECE Workshop on Short-Term Statistics (STS) and Seasonal Adjustment 14 – 17 March 2011 Astana, Kazakhstan. 1. 4.1.2020. Introduction.

E N D

Pre-treatment practices forSeasonal Adjustment Including Calendar Adjustment Necmettin Alpay KOÇAK UNECE Workshop on Short-Term Statistics (STS) and Seasonal Adjustment 14 – 17 March 2011 Astana, Kazakhstan 1 4.1.2020

Introduction • Seasonal adjustment is a statistical procedure with the target of removing the seasonal (and calendar) component from a time series. • The idea behind is that a series is composed by unobserved components such as trend, cycle, seasonality, irregular • The seasonal component disturbs short-term analysis, so it is removed from the original series to facilitate the monitoring and interpretation of the economy by analysts 2 4.1.2020

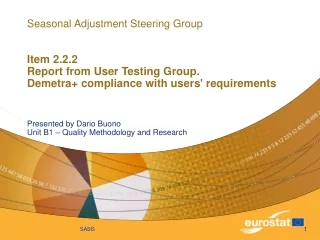

First step: the graph of the series Each series must be plotted against time to detect visually whether or not a seasonal component is present (but in some case it is not sufficient!) Example: Industrial production index - Total, Kazakhstan : Period: 2000M1-2010M10 3 4.1.2020

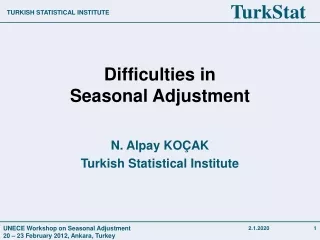

First step: the graph of the series Seasonal graphs are a special form of line graph in which you plot separate line graphs for each season in a regular frequency monthly or quarterly data. Example: Industrial production index - Total, Kazakhstan : Period: 2000M1-2010M10

Decomposition scheme • A time series yt can be decomposed in Yt = TCt +St+εt • A time series yt can also be decomposed in Yt = TCt×St×εt log(Yt)=log(TCt)+log(St)+log(εt) The Additive model Multiplicative model

The REG-ARIMA model • The REG-ARIMA model is a convenient way to represent a timeseries with deterministic and stochastic effects. Given theobserved time series zt , it is expressed as, zt = ytβ+xt Φ(B)δ(B)xt=θ(B)at • where • β is a vector of regression coefficients • yt denotes n regression variables • B is the backshift operator (Bkyt = yt-k ) • Φ(B), δ(B), and θ(B) are finite polynomials in B • at is assumed a normal independentlyidentically distributed(NIID)(0,σa2) white-noiseinnovation

The regression variables • The regression variables capture thedeterministic components ofthe series. In TS, these can be of different type: • Calendar effects • Trading day effect • Easter effect • Leap-year effect • Holidays • Intervention variables generated by the program • Regression variables entered by the user • Outliers

The ARIMA model • Model-based-pre-adjustment identifies and fits an ARIMA model on the linearized series (cleaned from deterministic effects). The ARIMA model is composed of three components: • the stationary AR component (polynomial Φ(B)) • the non-stationary AR component (polynomial δ(B)) • the invertible MA component (polynomial θ(B)) • For seasonal time series, the polynomials are given by: • Φ(B) = (1+ Φ1B + … + ΦpBp)(1+ Φ1Bs + …+ ΦPBs×P) • δ(B) = (1-B)d(1-Bs)D • θ(B) = (1+ θ1B + … + θpBp)(1+ θ1Bs + …+ θPBs×P) • A seasonal ARIMA model is identied by the order of itspolynomials: (p;d;q)(P;D;Q)

TRAMO / Reg-ARIMA • Program for estimation, forecasting, and interpolation ofregression models with missing observations and ARIMAerrors, with possibly several types of outliers • The program is aimed at monthly or lower frequency data(quarterly, semester, 4-month, bimonth, semester, year) • Performs a pretesting to decide between a log transformationand no transformation

TRAMO / Reg-ARIMA • Identifies the ARIMA model through anAutomatic ModelIdentification (AMI) procedure • Interpolates missing values • Detects outliers • Estimates the REG-Arima model • Computes forecasts

Automatic model identication • The ARIMA model can be automatically identified by theprogram • Two steps • Obtains the order of differencing • max order ∆2 ∆s • Obtains the multiplicative stationary ARMA model • 0<=(p;q)<=3 • 0 <=(ps;qs )<=1 • Chosen with the BIC criterion, favors balanced model (similarorders of AR and MA parts) • Otherwise, it can be input by the user (parameters P,D,Q, BP,BD, BQ) • It works jointly with the Automatic Outlier Detection andCorrection (AODC)

Outliers • They represent the effect on the time series of some special events(new regulation, major political or economical reform, strike,natural disaster). Three possible forms of outliers: • Additive outliers (AO) • Level Shift (LS) • Transitory Changes (TC)

Calendar effects • Calendar adjustment removes those non-seasonal calendar effectsfrom the series, for which there is statistical evidence and aneconomic explanation. Four possibilities in TS: • Trading days (working/non-working, 6 regressors)) • National and moving holidays ((provided by the user)) • Leap-year (TS versus X-12-ARIMA) • Easter • A pre-testing on the presence of theseeffects. • If trading days are significant, adding the holidays variableimproves significantly the results!

Trading/Working Day Adjustment • Aims at a series independent of the length and the composition in days • Length of month, number of working days and weekend days, composition of working days (Monday/Friday) • Working or trading-day adjustment is recommended for series with such effects • If effects not present –Regressors should not be applied • Compile, maintain and update national calendars! • A historical list of public holidays including information on compensation holidays

Correction for Moving Holidays • Occur irregularly in the course of the year • Correct for detected moving holidays in series • Not removed by standard filters • If effects not present –Regressors should not be applied • These effects may be partly seasonal: • The Catholic Easter, for example, falls more often in April than in March • Since the seasonal part is captured by seasonal adjustment filters, it should not be removed during the calendar adjustment