Download

1 / 5

50 likes | 135 Views

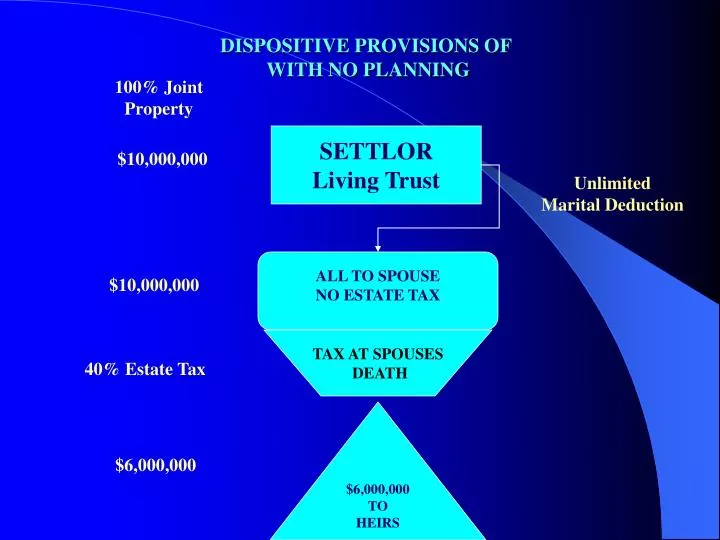

DISPOSITIVE PROVISIONS OF WITH NO PLANNING. 100% Joint Property. SETTLOR Living Trust. $10,000,000. Unlimited Marital Deduction. ALL TO SPOUSE NO ESTATE TAX. $10,000,000. TAX AT SPOUSES DEATH. 40% Estate Tax. $6,000,000 TO HEIRS. $6,000,000.

E N D

DISPOSITIVE PROVISIONS OF WITH NO PLANNING 100% Joint Property SETTLOR Living Trust $10,000,000 Unlimited Marital Deduction ALL TO SPOUSE NO ESTATE TAX $10,000,000 TAX AT SPOUSES DEATH 40% Estate Tax $6,000,000 TO HEIRS $6,000,000

DISPOSITIVE PROVISIONS OFPROPOSED ESTATE PLANTESTAMENTARY $10,000,000 Credit Shelter Amount SETTLOR Living Trust Unlimited Marital Deduction $1,500,000 $8,500,000 MARITAL QTIP/QDOT TRUST TO SPOUSE NO ESTATE TAX 40% ESTATE TAX AT SPOUSES DEATH FOR LIFE LIMITED BY CERTAIN STANDARD $5,100,000 $6,600,000 TO HEIRS 100% TO HEIRS

DISPOSITIVE PROVISIONS OFPROPOSED ESTATE PLANTESTAMENTARY ILIT $10,000,000 SETTLOR Living Trust $2,000,000 JSWL $5 Million Death Benefit IRREVOCABLE LIFE INSURANCE TRUST Gifting Unlimited Marital Deduction Credit Shelter Amount $1,500,000 MARITAL QTIP/QDOT TRUST $6,500,000 TO SPOUSE NO ESTATE TAX TAX AT SPOUSES DEATH Net $3,900,000 FOR LIFE LIMITED BY CERTAIN STANDARD $5,400,000 + $5 Mil. DB. = $10,500,000 TO HEIRS 100% TO HEIRS $5,000,000 100% TO HEIRS $1,500,000

Charitable Remainder Annuity Trust John Jones - Age 74 Mary Jones - Age 70 6.38% Annuity Trust Property Value $1,000,000 Cost $100,000 Gain $900,000 Principal $1,000,000 Charity/Family Foundation Annual Annuity Income $63,800 Estimated Income for 2 lives over 20.2 years $1,228,760 Transfer and sell tax-free. Bypass up to $900,000 gain may save $135,000. Income tax deduction of $272,825 may save $95,489. If trust earns 7.81%, pays 6.38% annuity, trust value increases. After two lives, trust passes without probate to charity.

PROPOSED ESTATE PLANTESTAMENTARY ILIT + Charitable Trust/Family Foundation $10,000,000 SETTLOR Living Trust $2,000,000 JSWL $5 Million Death Benefit IRREVOCABLE LIFE INSURANCE TRUST Gifting Unlimited Marital Deduction Credit Shelter Amount $1,500,000 MARITAL QTIP/QDOT TRUST $5,500,000 TO SPOUSE NO ESTATE TAX TAX AT SPOUSES DEATH Estate Tax reduces to 37% Net $3,465,000 CRAT $1,000,000 $3,465,000 + $5 Mil. DB. = $8,465,000 TO HEIRS $5,000,000 Family Foundation Heirs Are Directors $1,667,073 100% TO HEIRS $1,500,000

![Stamp Duty (Special Provisions) Act No.12 of 2006 [Main provisions]](https://cdn0.slideserve.com/167840/stamp-duty-special-provisions-act-no-12-of-2006-main-provisions-dt.jpg)