Download

1 / 16

160 likes | 169 Views

Learn about the key provisions and effects of the Tax Cuts and Jobs Act 2018 one year after its implementation. Discover changes in tax rates, deductions, and credits, as well as the impact on Affordable Care Act, AMT, estate taxes, education expenses, and pass-through entities.

E N D

Tax cuts and jobs act 2018 Public Law No. 115-97

One Year Later… • When will this Reform take effect?? • From the 2018 tax year • We file the tax returns in 2019 calendar year • Most Individual tax provisions are set to expire in January 2025 • We expect that they will be extended (similar to Bush Tax Cuts) • Immediate Changes Noticed? • By end of February 2018, withholding on paychecks will change • Reflects New Tax Rate Schedule • General: Take-Home pay should be an increase for most

Major changes for individuals Four Major Sections

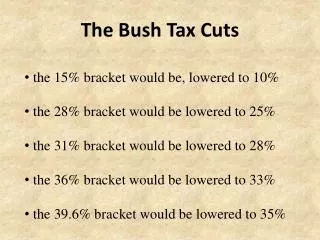

Tax Rates for Individuals • Maximum Tax Rate: • Highest bracket decreased from 39.6% to 37% • 7 bracket structure: 10%, 12%, 22%, 24%, 32%, 35%, 37% • Approximate 2-3% decrease in rates from old to new • General: Positive effects seen across the board (Decrease overall tax)

Deductions & Tax Credits Changes • Standard Deduction: • Increased Single: $12,000 MFJ: $24,000 • Expecting more people to choose this over Itemized Deduction • Personal Exemption: • Suspended Larger families affected • Child Tax Credit: • Increased $2,000 per child, maximum $1,400 is refundable • ”Refundable” – you can take the credit even if you don’t owe any tax ($0 liability) • AGI limitation “phase-out”: $200,000/$400,000 • Moving Expenses & Alimony Payments: • Eliminated

Itemized Deductions • Charitable Contributions: • Increased Now AGI limitation is 60% • General: Decrease tax savings for low-bracket individuals; Similar/Greater tax saving appeal for high-bracket individuals • Medical Deductions: • TemporaryIncrease Allowed expenses in excess of 7.5% AGI • From 2019 Tax Year, back down to 10% AGI floor • Mortgage Interest: • Limited Up to $750,000 of Home Acquisition Debt allowed • Allowed for New Primary or Secondary Homes • Home Equity Debt Eliminated unless used for Home Improvement

Itemized Deductions • Miscellaneous 2% Deductions: • Eliminated Tax Prep Fees, IRA Custodial Fees, Investment Advisory Fees, Home Office Deduction, Employee Business Expenses • Casualty & Theft Losses: • Eliminated • Exception: Federally Declared Disasters • State and Local Taxes: • Limited $10,000 aggregate • State/Local Property Taxes + Income Tax (or Sales Tax) • General: Affects more expensive property, higher-income areas, individuals working/living in higher state tax rates

Affordable Care Act • Health Insurance: • Required Coverage in 2018 tax year • Suspended as of 01/01/2019 • They have NOT actually eliminated the requirement • They have reduced the Responsibility Payment to $0 in 2019 • The Penalty: • The Greater of: • 2.5% Household Income (Above Tax Filing $ Limit) • $695 per person. $347.50 per child (Individuals Not Covered) • Please note: Amounts are 2017 figures and indexed for inflation

Additional changes for individuals AMT Estate Tax Education

AMT and Estate Taxes • Alternative Minimum Tax: • What is it?? • It’s an alternative tax assessed which disallows and/or limits certain deductions a taxpayer can take advantage of on their federal return • Taxpayers pay the higher of Regular Tax or AMT • Not Repealed (Darn it!!) • Increased Exemption amount to $109,400 MFJ, Phase-Out Levels to $1 Million • Estate Taxes: • Increased Personal Exemption essentially Doubled • $10 Million per person, subject to inflation • Annual Gift Exclusion: $15,000 (2018)

Education Expenses • Education Expenses: • 529 Plan: Increased use Now allowable for Private Schools, Elementary, Secondary, or Higher Education • Tax Free Earnings on 529 Plans • A max $10,000 withdrawal per pre-college beneficiary per year • No limits on withdrawals for college beneficiaries per year • Graduate Student Benefits: • Tax Free Graduate Funding: Education Grants received • Corporations can give Annual Benefit of ~$5,250 to Employees • Student Loan Interest: • Retained $2,500 Interest paid is Deductible

Small businesses Entity Choices & Structure Pass-Through Entities

Entity Choices • C – Corporation: • Pays Taxes at Entity Level – Double Taxation impact to Shareholders • Decreased Now 21% Flat tax rate • S-Corporation, Partnership, Sole Proprietorship: • Pass-Through Entities • Profits and Losses flow through to Owners/Shareholders • New Tax Law Intent is to help Small Business Owners

Pass Through Entities & Schedule C (Sec 199A) • General: 20% deduction on Business Income for Pass-Through Entities • Limitations for certain “Personal Service Businesses” • Accountant, Attorney, “Provides Services” may not be eligible • Limitations on thresholds, phase-ins, phase-outs • “Qualified Business Income”: • Huge Calculation to figure this amount out • Takes into account W-2 wages and qualified property • Real Estate Professionals may be eligible for this deduction • Personal Service Income Exception

Kershaw K. Khumbatta PLLC Kershaw K. Khumbatta, CPA Mitra K. Khumbatta, CPA, MSA Kershaw@KhumbattaPC.com Mitra@KhumbattaPC.com Phone: 281-313-8006 The topics discussed in this presentation should not be used for anything other than informational purposes only. The items discussed do not constitute tax or legal advice. If there are items requiring additional clarification, please consult with your tax advisor.