Download

1 / 14

140 likes | 287 Views

Absa Investments THE CHALLENGING ECONOMIC ENVIRONMENT. Craig Pheiffer General Manager: Investments Absa Asset Management Private Clients. Global growth has slowed but country outlooks differ:. Least disruption from the crisis (slower growth but positive): China India

E N D

Absa Investments THE CHALLENGING ECONOMIC ENVIRONMENT Craig Pheiffer General Manager: Investments Absa Asset Management Private Clients

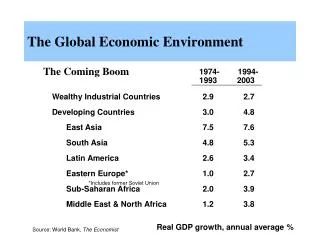

Global growth has slowed but country outlooks differ: • Least disruption from the crisis (slower growth but positive): • China • India • Peripheral to crisis, commodity-assisted rebound, some policy normalisation: • Russia • Brazil • Canada • At the centre of the crisis, meagre recovery: • Germany • United States • United Kingdom • Italy • Spain • Japan The strongest economies have the most scope to provide policy stimulus while the weakest have the least. Source: Barclays Capital Global Economics Weekly(20 July 2012)

The weakest economies have limited options: • Key Central Bank interest rates UK EU US JP The market seeks more quantitative easing (“QE”) with interest rates near zero but the impact of more QE in a weak demand environment is questionable. Source: Barclays Capital Global Economics Weekly(20 July 2012)

United States • Bernanke’s Senate testimony: • “Risks to the growth outlook lie to the downside” - leaves the bar to further policy easing low. • “Frustratingly slow” progress on reducing unemployment rate. • High probability of inflation < 2%. • Fiscal concerns! • Recent consumption data has been soft but there have been encouraging signs on manufacturing for Q3. • BarCap expectations: • A better H2 as lower energy prices boost disposable incomes and household consumption. QE3 still not the base case. • Stickier core inflation once lower energy prices have worked out of the system (plus higher rent payments). • Advance reading of Q2 GDP on Friday expected at 1.5%. Source: Barclays Capital Global Economics Weekly(20 July 2012)

Euro area • European Financial Stability Facility has committed up to €100bn to the Spanish government for recapitalising banks - Expectation is that €70bn- €80bn will be required. Should be at a favourable rate (±3.0%) with a favourable maturity. • Spain commits to new fiscal targets set by the EC and other macroeconomic conditions set by the IMF. Government appears willing to accept these (VAT rate hike, dropping housing subsidies). • Spain likely to need financial assistance in the bond market to finance budget deficits. Expect a primary surplus in 2.5 years with debt to GDP ratio peaking at 95% in 2015. • Greece under the spotlight again with the troika visit - “Grexit” - has the “horror” really faded? • Euro area concerns to linger: stronger dollar, risk “off”. Source: Barclays Capital Global Economics Weekly(20 July 2012)

United Kingdom • MPC split on use and effectiveness of additional quantitative easing (QE upped by £50bn to £375bn). • Alternatives policies being introduced such as the “Funding for Lending Scheme” (FLS) - likely to have limited effect in subdued demand environment. • Inflation has fallen but MPC looking through the inflation dip as a temporary phenomenon. [BarCap sees near-term inflation pressures well below target but inflation is expected to rise above target by mid-2013] • Expect Q2 GDP to have fallen by 0,2% q/q, a third consecutive quarterly contraction in economic output. Source: Barclays Capital Global Economics Weekly(20 July 2012)

Japan • Real GDP expected to slow in FY2013 as government-led post-earthquake reconstruction measures run their course. • Bank of Japan sees inflation nearing price stability goal (of around 1%) in 2014 even without further fiscal stimulus. Any response to calls for additional fiscal expansion could push prices higher. • Bill to raise consumption tax (VAT) from 5% to 8% in April 2014 and 10% in October 2015 could push prices higher. BarCap expects 60% of any VAT rate increase to filter through to CPI. Source: Barclays Capital Global Economics Weekly(20 July 2012)

China • Latest GDP growth data was broadly in line with most officials’ expectations. Most officials agree that some further policy measures may be required to stabilise economic growth at 7.5-8.5%. “Prudent” to “expansionary”? • Rapidly falling inflation from the 6.5% July 2012 high has opened the way for more central bank action. More reserve ratio cuts expected in H2 to stabilise liquidity + base interest rate cuts. • Officials argue that Chinese economic growth cannot rely purely on: • Public-led investment. • Credit expansion. • Liquidity injections. • The government is trying to strike a balance between falling property investment and surging housing prices. BarCap believes that some relaxation of housing purchase restrictions at the local level is likely to continue. Source: Barclays Capital Global Economics Weekly(20 July 2012)

Growth (GDP) Outlook Q/Q % Changes in GDP: DEVELOPED Y/Y % Changes in GDP: DEVELOPED Y/Y % Changes in GDP: DEVELOPING Source: Barclays Capital Global Economics Weekly(20 July 2012)

The SARB’s South African outlook (July vs May 2012) GDP 2012: 2.7% (2.9%) 2013: 3.8% (3.9%) 2014: 4.1% (4.1%) Inflation 2012: 5.6% (6.0%) 2013: 5.1% (5.5%) 2014: 5.1% (5.0%) Source: SARB MPC Policy Statement (19 July 2012) and SARB Monetary Policy Review (29 May 2012)

Household consumption slowing? Manufacturing on the up? • Real Retail Sales (%): 2004-2012 • Manufacturing (%): 2004-2012 May: 6.4% y/y May: 4.2% y/y • Mining production (%): 2004-2012 Retail sales has been erratic due to base effects but some evidence of a slowing trend in consumption. Recent manufacturing data has been better than expected. May: 0.8% y/y

South African outlook Quarterly data: Y/Y % Changes in GDP: Source: Barclays Capital Global Economics Weekly(20 July 2012)