Download

1 / 17

170 likes | 179 Views

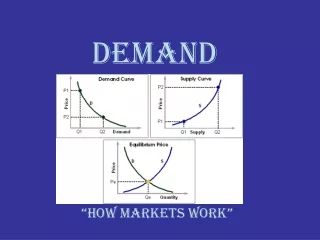

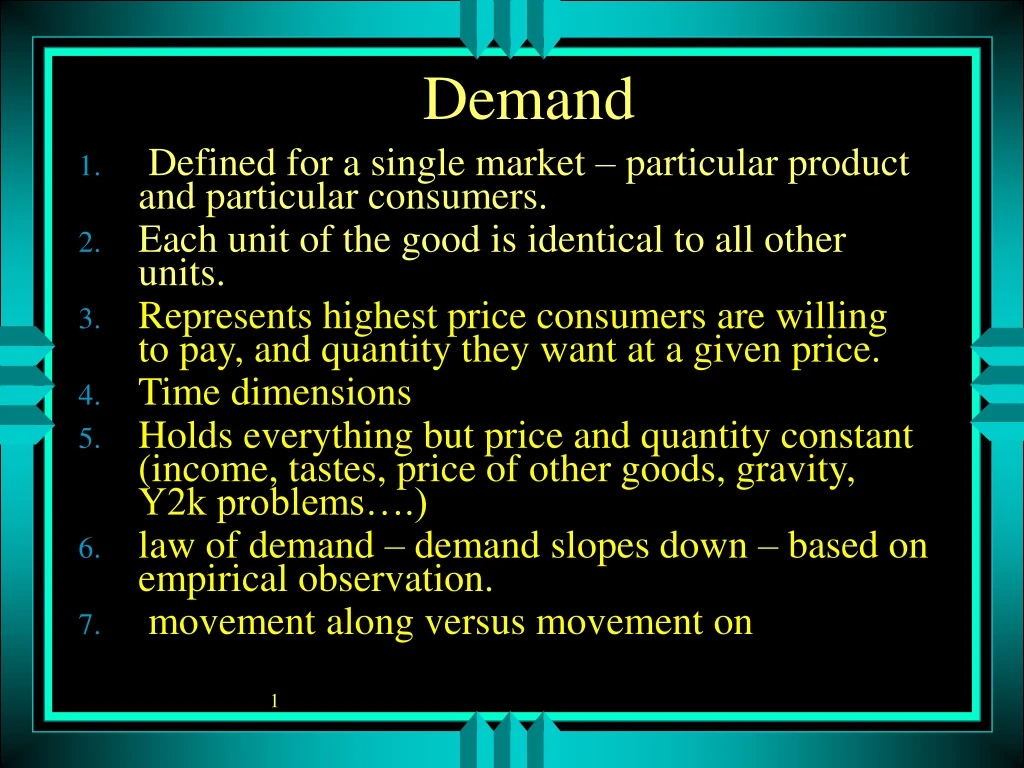

Demand. Defined for a single market – particular product and particular consumers. Each unit of the good is identical to all other units. Represents highest price consumers are willing to pay, and quantity they want at a given price. Time dimensions

E N D

Demand • Defined for a single market – particular product and particular consumers. • Each unit of the good is identical to all other units. • Represents highest price consumers are willing to pay, and quantity they want at a given price. • Time dimensions • Holds everything but price and quantity constant (income, tastes, price of other goods, gravity, Y2k problems….) • law of demand – demand slopes down – based on empirical observation. • movement along versus movement on

P Demand D Q

Demand • Defined for a single market – particular product and particular consumers. • Each unit of the good is identical to all other units. • represents highest price consumers are willing to pay. • Holds everything but price and quantity constant (income, price of other goods, gravity, Y2k problems….) • time dimensions • law of demand – demand slopes down – based on empirical observation. • movement along versus movement on

Demand for WLM* P1 P2 PWLM D Q2 QE Q1 *“Winners, Losers and Microsoft”

Shift in Demand for WLM D1 D P Perhaps a positive review in the Wall Street Journal leads to an increase in demand curve Q

Price Elasticity Of Demand • def: percentage change in quantity divided by percentage change in price • (ΔQ/Q)/(ΔP/P) or (ΔQ/ΔP) (P/Q) • measure of responsiveness • If Elasticity is >1 known as elastic (responsive customers) • If Elasticity is =1 ; unit elastic • If Elasticity is <1; inelastic (less responsive customers) • Infinite and zero elasticity

Illustrations of elasticity D with zero elasticity P D with infinite elasticity Q

Elasticity and TR • When elasticity is greater than 1 (elastic) increases in price lead to decreases in revenue and vice-versa • When elasticity is equal to 1, changes in price lead to no change in revenues • When elasticity is less than 1 (inelastic) increases in price lead to increases in revenue.

Implications of Elasticity • If Elasticity is <1, firm can always increase Profit by increasing price (revenues increase and costs decrease because output decreases) • If Elasticity =1, firm can always increase profit by increasing price • If Elasticity>1 firm can not necessarily increase its profits by a change in price. • Thus firms that maximize profits must have elasticities >1. • Example of VideoTape Sales Demonstrates Importance of knowing elasticity.

Long Run and Short Run Elasticities • Elasticity is greater in the long run • consumers have more time to react to price changes • For example, if the price of gasoline goes up, consumers at first can try to reduce the amount they drive, but this is often difficult. Over time, they can by more fuel efficient cars or move closer to their work.

P new higher price D after consumers have time to adjust to price change original price D before consumers have much time to adjust amount consumed after longer period of adjustment\ amount consumed after short period of adjustment\ Q

Supply: • Represents minimum price sellers require to voluntarily provide the product. • assume it slopes up for now. In reality it depends on the cost conditions of the firm. • Same assumptions as with demand: everything else is held constant.

Meaning of Supply S P2 minimum price firm is willing to accept. Should be equal to the cost of producing the additional output P1 Q1 Q2

Meaning of (Stable) Equilibrium • A situation such that the variables of interest remain at rest until disturbed by some outside force. For stability, the variables must return to the equilibrium after being disturbed by some force. • Gravity and the resting place of tennis balls. • We assume many producers and consumers to start the analysis. • Surplus and shortages take the place of gravity in these markets.

Illustration of Supply Demand Equilibrium S Surplus P1 Pe P2 Shortage D Q1 Qe Q2

Examples of changes in Equilibrium • Supply and Demand analysis assumes that market moves from one equilibrium position to another. • Shifts in D or S alter equilibrium. For example, how would you expect the price and quantity of Pepsi Cola to change when: • Price of Coca Cola falls. • Price of fructose goes up • Surgeon general warns of soda threat to health. • Winter changes to summer. • TV ads for cola banned • Answers on next slide.

Changing Equilibrium S1 2 P2 S2 4 P4 1 P1 D2 3 P3 D1 Q4 Q1 Q3 Q2