Download

1 / 17

170 likes | 369 Views

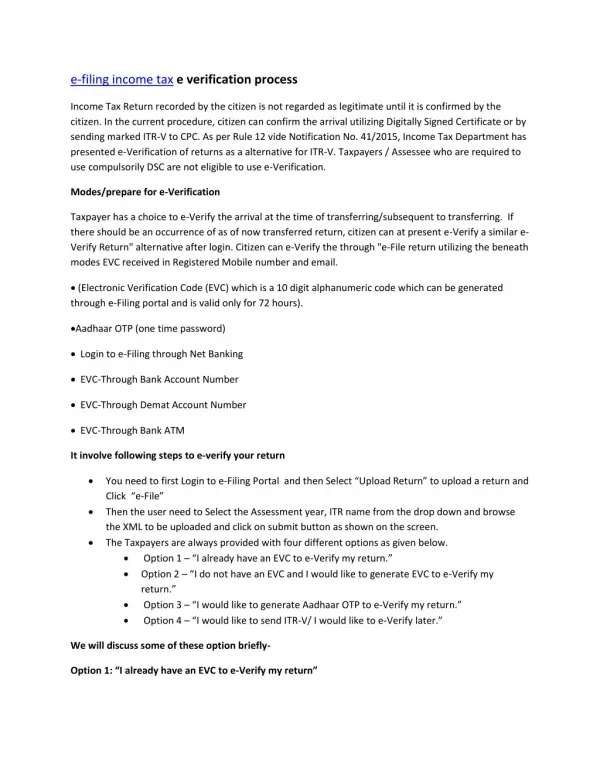

Bringing XBRL tax filing to the UK. Jeff Smith, Customer Contact, Online Services,. Agenda. Why XBRL? External review of HMRC Online Services. The Company Tax Return. XBRL progress to date. Next steps. Lessons learned. Why XBRL?. HMRC first became aware of XBRL in 2001.

E N D

Bringing XBRL tax filing to the UK Jeff Smith, Customer Contact, Online Services,

Agenda • Why XBRL? • External review of HMRC Online Services. • The Company Tax Return. • XBRL progress to date. • Next steps. • Lessons learned.

Why XBRL? • HMRC first became aware of XBRL in 2001. • What attracted us: • vision of streamlining the end to end financial reporting process - linking business, accounting and tax software. • access to data - rather than everything on paper. • picking up an external initiative - origins within the financial community, not Government driven. • possible data standard in a wider government context.

External review of HMRC online services • July 2005 - UK Government asked Lord Carter to advise on measures to increase the use of HMRC’s key online services, in order to ensure sustainable and efficient service delivery for taxpayers, while continuing to support compliance. • March 2006 - UK Government accepts recommendations in full.

Key recommendations (for XBRL): • “All companies should be required to file their company tax returns online, using XBRL …….. for returns due after 31 March 2010.” • “Our view is that HMRC should not require online submission of company tax returns until XBRL has been implemented and has bedded down.” • “We also recommend that they [HMRC & Companies House] should work towards providing a joint filing facility so that companies and their agents only have to submit the same information once.”

Return form (CT600) Accounts Computations Need ALL three components to make up a valid return Complex information Difficult to put together Company Tax Return- scope for a simplerapproach

Computations are complex • Accounts figure of profit adjusted for tax purposes • capital allowances • depreciation etc • Often 30 pages + • Free format • No standard layout • Paper documents • usually produced using specialised software • information inaccessible • no data flow to HMRC systems

Accounts are currently paper based • We require full accounts including Profit & Loss • Again all held on paper with little data flow to HMRC systems • Limited information available for risk assessment and for Government financial planning • Companies required to submit accounts separately to other Government Departments

XBRL e-filing progress • Late 2001 - Workshops with accountants and software vendors agreed a phased approach to CT e-filing with XBRL seen as an integral part from the outset. • Phase 1 - delivered in March 2003 • XML based CT600 Return + computations + accounts (as pdf’s). • enabled proving of the basic service before moving on to Phase 2. • Phase 2 - delivered in February 2006 • allows computations to be submitted in XBRL format • HMRC have developed the underlying data structure in conjunction with accountants and software vendors. Complex task as there is no standard format for computations and need to avoid any constraints in how information is presented on screen or when printed.

Next steps - XBRL accounts • Will be able to accept XBRL accounts as soon as suitable accounts taxonomies are available: • UK Companies House (small, audit exempt companies later in 2006 and full accounts in 2007) • UK GAAP (HMRC are assisting with development) • IFRS, US GAAP etc • Straightforward task for HMRC to link to new taxonomies. • HMRC XBRL service designed to interact with third party software systems only • HMRC’s own online application does not include an XBRL capability (although could be made to do so if customers need it).

Next steps - working towards mandatory XBRL e-filing in 2010 • Technical specification is already published. • work closely with software vendors and accountants to help them adopt XBRL (main task is mapping our taxonomy to their products). • encourage accountants to start XBRL filing early - working collaboratively to prove and fine-tune the service, especially for the more complex cases (e.g. use of taxonomy extensions). • Widening the net. • joint workshops with software vendors on online services? • how do we reach the smaller accountancy firms? May not be represented by professional bodies. • software availability for very small companies?

Lessons learned • CT Computation - Taxonomy development - 4000+ items • Large scale data analysis exercise - requires an iterative approach. • lack of any existing structure (free-format) main reason for complexity • but feasiblewith assistance from accountants and software vendors. • started with Excel, but soon required specialist XBRL support and benefited from XBRL software tools (ensuring conformant to standards and internal consistency and validation). • Try to keep it simple! • taxonomy itself and XBRL features • e.g. limited use of computational and formula linkbases.

Lessons learned • Display (rendering) of XBRL submissions (on screen and printed) is a key business requirement, both for HMRC, accountants and company directors. • clients need to approve what is to be submitted - a string of data is not enough! • stylesheets have proved to be very difficult to create, even for simple accounts and computation - now an XBRL Domain Working Group issue. • US Securities & Exchange Commission share our concerns about rendering.

Lessons learned • Consider use of software tools for both taxonomy creation AND review when external organisations join in.

Lessons learned • Provide comprehensive documentation

Bringing XBRL tax filing to the UK The End!