Download

1 / 4

40 likes | 49 Views

If you want to decrease your debt-to-income ratio, focus on paying your bills on time. At the same time, pay down your credit card balance to improve your qualifying chances and get a low mortgage rate.

E N D

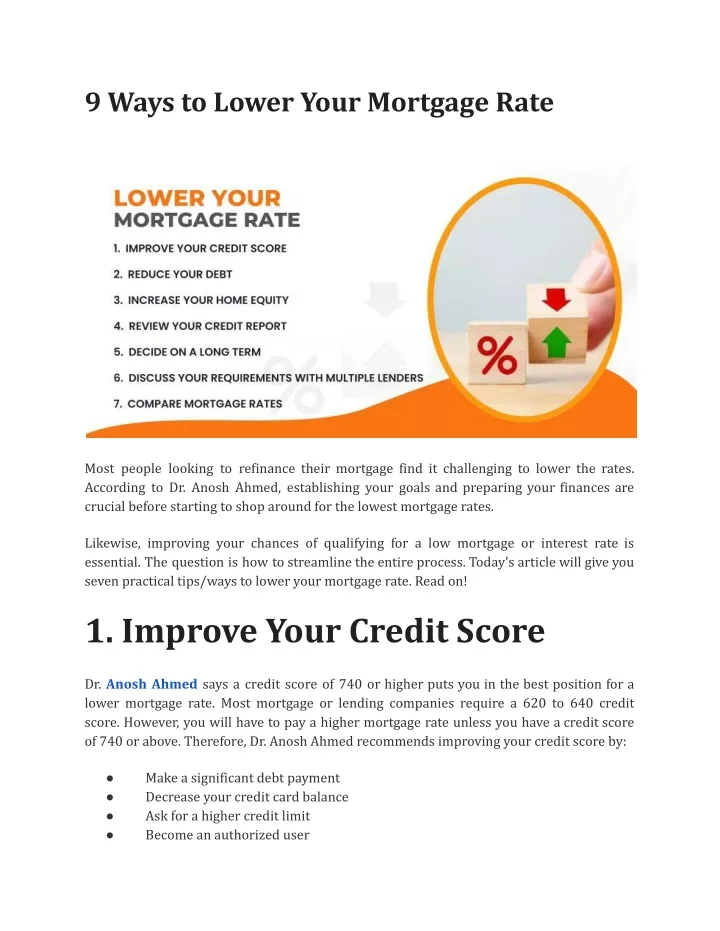

9 Ways to Lower Your Mortgage Rate Most people looking to refinance their mortgage find it challenging to lower the rates. According to Dr. Anosh Ahmed, establishing your goals and preparing your finances are crucial before starting to shop around for the lowest mortgage rates. Likewise, improving your chances of qualifying for a low mortgage or interest rate is essential. The question is how to streamline the entire process. Today’s article will give you seven practical tips/ways to lower your mortgage rate. Read on! 1. Improve Your Credit Score Dr. Anosh Ahmed says a credit score of 740 or higher puts you in the best position for a lower mortgage rate. Most mortgage or lending companies require a 620 to 640 credit score. However, you will have to pay a higher mortgage rate unless you have a credit score of 740 or above. Therefore, Dr. Anosh Ahmed recommends improving your credit score by: ● ● ● ● Make a significant debt payment Decrease your credit card balance Ask for a higher credit limit Become an authorized user

2. Reduce Your Debt If you want to decrease your debt-to-income ratio, focus on paying your bills on time. At the same time, pay down your credit card balance to improve your qualifying chances and get a low mortgage rate. Dr. Anosh Ahmed says having a debt-to-income ratio below 36% is crucial. However, if you can lower it further, you will have increased chances of qualifying for the lowest possible mortgage rate. For instance, avoid purchasing a new car, fill out multiple credit applications, and save more money to improve your credit profile. If your debt-to-income ratio is higher than average, the lender can deny a low mortgage rate even if you have a better credit score-Articlesoul.. 3. Increase Your Home Equity Your mortgage-articlesoul rate. For instance, you will get a more expensive mortgage and interest rate when you have a higher loan-to-value and lower-than-average credit score. In that case, you can a HARP loan is an optimal option. property’s loan-to-value ratio and credit score substantially impact your 4. Review Your Credit Report Dr. Anosh Ahmed suggests getting your credit reports from the three bureaus and reviewing the information. The purpose is to check the reports for mistakes and make necessary corrections before applying for a mortgage. Collecting these documents can speed up the loan process and prevent the risk of paying an additional amount for your rate lock. Look for changes to your personal and financial information, including: ● ● ● Account details Public record data Financial inquiries

5. Decide on a Long Term Consider crucial financial plans and obligations before deciding on a long-term mortgage. For example, if you have $20,000 in credit card debt without any savings for future endeavors, you can go for a 20-year loan to keep the payments low. According to Dr. Anosh Ahmed, some people look for a short-term mortgage to build equity efficiently and quickly. However, Dr. Ahmed says borrowing a mortgage for the long term is better because it keeps your tax deductions for a prolonged period. 6.Discuss YourRequirements with Multiple Lenders Research loan products or services available from a community bank, regional bank, credit union, or direct lender. The purpose is to determine the special programs each organization offers. Find a trustable and reliable mortgage lender instead of selecting a company based on the current rates-Articlesoul.. 7. Compare Mortgage Rates Mortgage rates advertised by companies are primarily based on paying points. Therefore, Dr. Anosh Ahmed recommends comparing loans with zero points and shopping for the same mortgage loan on the same day to get realistic comparison results. Remember, mortgage rates undergo changes every second day. So, explain the criteria for your mortgage refinance and ask each officer about the loan processing times. 8. Shorten Your Loan Financial organizations like it as home buyers repay debts quickly. Try taking out a 10-year and 15-year mortgage for a fewer mortgage price. Even, any loan with a term less than 30 years should lower the interest rate you’ll pay. A lower interest rate means your loan balance will fall faster and you’ll be able to put more money away for a down payment on a home-Articlesoul..

9. Put more money down Fifth, consider how much money you plan to put down on your home purchase. If you go over a certain amount, your loan will be considered a jumbo loan, which carries more risk for the bank. These usually carry a higher interest rate too. By putting enough money down to lower the interest rate of your jumbo loan, you could save thousands of dollars over the life of that loan-Articlesoul. Final Words Getting a lower mortgage rate offers various benefits. For instance, you can refinance your mortgage, purchase a house, choose a fixed rate, buy another home, refinance your car/student loan, and consolidate your debt. Follow these steps or ways to lower your mortgage rate, avoid risks, and achieve peace of mind.