Download

1 / 18

250 likes | 686 Views

Why use single index model?. (Instead of projecting full matrix of covariances) Less information requirements It fits better!. If we only knew α !. Maybe we do know α !. Two approaches: (i) security analysis (ii) efficient market theory (e.g. CAPM). CAPM - Assumptions.

E N D

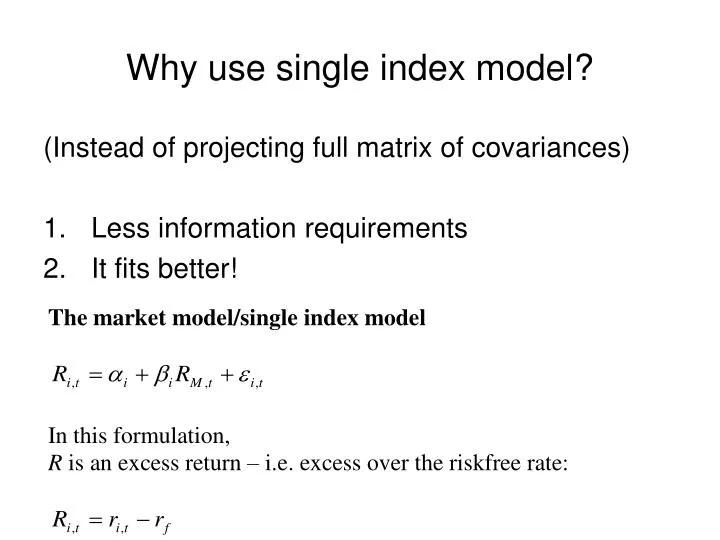

Why use single index model? (Instead of projecting full matrix of covariances) • Less information requirements • It fits better!

Maybe we do know α! Two approaches: (i) security analysis (ii) efficient market theory (e.g. CAPM)

CAPM - Assumptions • Lots of small investors (none dominant) • All have same holding period • All assets publicly traded • No taxes or transactions costs • All investors are MV optimizers • (e.g. optimizing U = μ – ½Aσ2) • Everyone shares same information (homogeneous beliefs)

CAPM - Implications • All investors hold risky assets in the same proportion (“market portfolio”) • The Capital Market Line is the best attainable capital allocation frontier • Risk premium on the market portfolio is proportionate to risk and degree of risk aversion • Risk premium on individual assets proportional to risk premium on the market portfolio and the beta of the security relative to market portfolio

CAPM - Implications • Implies that αi = 0 all I in the index model • CAPM: • Index model

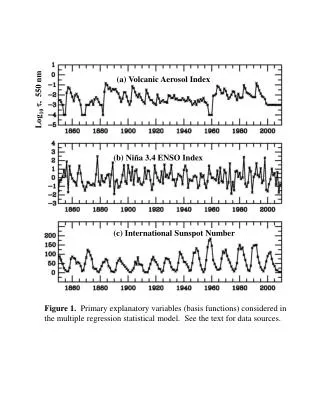

CAPM: Does it fit the data? Jensen, 1968

Private information and the security market line (SML) Expected return (market and private) SML Q (buy) R M P expected return T (sell) r actual return S (sell) Beta, bi 0.5 1 1.2 (The larger is bi, the larger is ERi)