Download

1 / 11

110 likes | 139 Views

This study employs linear regression to examine home lending trends in Worcester, MA, focusing on potential racial bias. Utilizing univariate and multivariate analyses at the Census Tract level, factors such as foreclosure rates, median income, and tenure are considered. While initial results suggest limited explanatory value in race-based lending patterns compared to economic indicators, the study recommends expanding Community Reinvestment Act (CRA) mandates to address issues of geographical discrimination and support lending in underprivileged areas.

E N D

Analyzing Home Lending Patterns for Discrimination in Worcester, MA with Linear RegressionCurtis WiemannPresented with assistance by Kathryn Madden, AICP, Faculty at Clark University

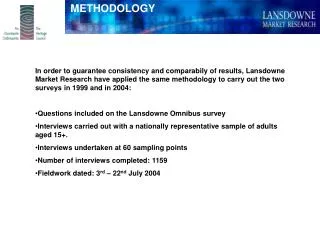

Methodology • Utilize linear regression to depict and analyze trends in home lending in Worcester, MA to determine if lending exhibited racial bias • Begin with univariate analysis of mortgage lending (measured in dollars per capita of conventional/FHA loans originated) and race/ethnicity (measured in % Hispanic [all races] and African-American) • Analyzed at Census Tract level (smallest unit of measurement possible for HMDA data publications) • Null hypothesis: no correlation between borrower race/ethnicity and home lending • Home lending influenced by many legitimate factors – to model risk and stock by Census Tract, rates of foreclosure (HUD, % of total), median income (Census, Table DP03 [Household Median Income]), and tenure (Census, Housing Characteristics [% Owner-Occupied]) were added in multivariate linear regression

Results • Univariate regression returned statistically-significant linear relationships between race and home lending, but these relationships were ultimately found to have limited explanatory value in comparison to foreclosure rates and median income rates by census tract. • Conjecture based on result: Race/ethnicity shares a linear relationship with median income and foreclosure rates, which indirectly shapes its linear relationship with mortgage lending. • Market conditions allow for inequitable lending that, while not directly correlated with race, nevertheless leads to fewer home lending dollars in mortgages originated to borrowers of color • Missing from this analysis: other racial/ethnic groups, analysis of home prices (which in turn affects mortgage origination values)

Limitations • Inappropriateness of linear regression • Linear regression best for controlled experiments; complexity of human factors influencing mortgage lending leads to low P-values throughout = low predictive value (~ 0.3, up to ~ 0.5) • Linear regression more useful the more points added; with 54 Census Tracts analyzed, outliers more influential • Data • Relatively small number of home loans covered under HMDA • Relatively small number of loans per tract (6 tracts with no conventional lending whatsoever – outliers) • Missing information: average home valuation by tract, other economic/social characteristics that could legitimately shape access or desire to conventional home borrowing • Approach • Aggregate view by tract imperfect method to evaluate existence/impact of discrimination

Recommendations • Expand the mandate of the CRA • “The Performance and Profitability of CRA-Related Lending,” 2000 Report to Congress: 30% of home lending activities are subject to the CRA • CRA mandates a slate of community reinvestment actions that may no longer reflect realities of geographical discrimination • Support lending in weak market tracts • If foreclosure and median income correlate with low lending, provide fiscal support to underwrite inherent risk of lending • Already mission of CDCs in Worcester; broadly mission of federal HUD • Possible to create municipal/state funding mechanisms to augment HUD/CDC mandate in Worcester and elsewhere