Download

1 / 12

120 likes | 136 Views

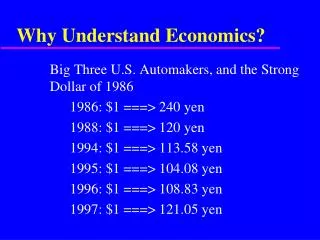

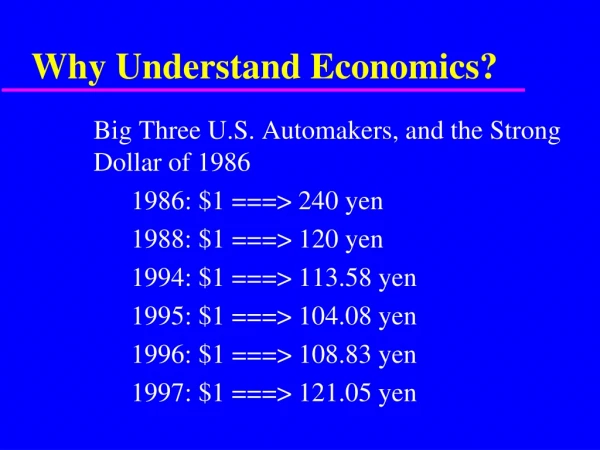

6.02 Understand economic indicators to recognize economic trends and conditions. 6.02-D Explain the economic impact of interest-rate fluctuations. 6.00 Understand economics trends and communication. 5-176 5-177 Define 6.02-D. Interest rate:

E N D

6.02 Understand economic indicators to recognize economic trends and conditions.6.02-D Explain the economic impact of interest-rate fluctuations. 6.00 Understand economics trends and communication.

5-176 5-177 Define 6.02-D • Interest rate: • The interest rate is the yearly price charged by a lender to a borrower in order for the borrower to obtain a loan. This is usually expressed as a percentage of the total amount loaned called annual percentage rate (APR). Nominal interest rate: • one where the effects of inflation have not been accounted Changes in the nominal interest rate often move with changes in the inflation rate, as lenders not only have to be compensated for delaying their consumption, they also must be compensated for the fact that a dollar will not buy as much a year from now as it does today. • Real interest rate: • is one where the effects of inflation have been factored.

For Example: Nominal vs. Real • Suppose we buy a 1 year bond for face value that pays 6% at the end of the year. We pay $100 at the beginning of the year and get $106 at the end of the year. Thus the bond pays an interest rate of 6%. This 6% is the nominal interest rate, as we have not accounted for inflation. Whenever people speak of the interest rate they're talking about the nominal interest rate, unless they state otherwise. • Now suppose the inflation rate is 3% for that year. We can buy a basket of goods today and it will cost $100, or we can buy that basket next year and it will cost $103. If we buy the bond with a 6% nominal interest rate for $100, sell it after a year and get $106, buy a basket of goods for $103, we will have $3 left over.

5-176 5-177 Define 6.02-D • Interest-rate fluctuation: Is a change in the interest rate. • Liquidity risk: The uncertainty associated with the ability to sell an asset on short notice without loss of value. • Default risk : The uncertainty associated with the payment of financial obligations when they come due. Put simply, the risk of non-payment.

5-176 5-177 Define 6.02-D • Maturity risk, price risk: • The greater the maturity of an investment, the greater the change in price for a given change in interest rates. The uncertainty associated with potential changes in the price of an asset caused by changes in interest rate levels and rates of return in the economy. This risk occurs because changes in interest rates affect changes in discount rates which, in turn, affect the present value of future cash flows. The relationship is an inverse relationship. If interest rates (and discount rates) rise, prices fall. The reverse is also true. Since interest rates directly affect discount rates and present values of future cash flows represent underlying economic value, we have the following relationships.

5-176 5-177 6.02-D • Discuss causes of interest-rate fluctuations. • The Fed rate is the most important factor that affects interest rates. If short-term interest rates are lowered or increased, then the costs of inter-borrowing between banks changes accordingly. This is reflected in the interest rates charged by banks from their customers. • However, various other economic factors also have an impact on interest rates. Short-term interest rates are the first to get affected by these factors, while long-term interest rates, like those charged on a mortgage, catch up with the changes slowly and they are determined by the long term outlook of the economy. That is why there is always more certainty about the returns from your investments if you invest for a longer time frame.

5-176 5-177 6.02-D • Explain the impact of interest rate fluctuations on an economy. • The impact of falling interest rates is that it is less costly to get credit. However, the returns on your savings would also be lower. Similarly, if interest rate increases, then loans become costlier, but you earn more on your savings.

5-176 5-177 6.02-D • Describe the relationship between interest rates and the demand for money. • Money is a narrowly defined term which includes things like paper currency, traveler's checks, and savings accounts. It doesn't include things like stocks and bonds, or forms of wealth like homes, paintings, and cars. Since money is only one of many forms of wealth, it has plenty of substitutes. The interaction between money and its substitutes explain why the demand for money changes. • A reduction in the interest rate will increase the Demand for Money and a rise in the interest rate causes the demand for money to fall.

5-176 5-177 6.02-D • Describe the relationship between inflation and interest rates. • There is typically an inverse relationship, high interest rates equals low inflation, low interest rates = high inflation.

5-176 5-177 6.02-D • Discuss factors that create differences in the amount of interest charged on credit transactions (e.g., levels and kinds of risk, borrowers’ and lenders’ rights, and tax considerations). • To mitigate the impact of default risk, lenders often charge rates of return that correspond the debtor's level of default risk. The higher the risk, the higher the required return, and vice versa. • Standard measurement tools to gauge default risk include FICO scores for consumer credit, and credit ratings for corporate and government debt issues. Credit ratings for debt issues are provided by Nationally Recognized Statistical Rating Organizations (NRSROs), such as Standard & Poor's, Moody's and Fitch Ratings.

5-176 5-177 6.02-D • Describe kinds of risk associated with variances in interest rates (i.e., default, liquidity, and maturity). • default risk, interest rate risk, price risk, reinvestment rate risk, liquidity risk, inflation risk, purchasing power risk, market risk, firm specific risk, project risk, financial risk, business risk, foreign exchange risk, translation risk, & transaction risk.

5-176 5-177 6.02-D • Explain how fiscal policies can affect interest rates. • Fiscal policy has a clear effect upon output. But there is a secondary, less readily apparent fiscal policy effect on the interest rate. • Basically, expansionary fiscal policy pushes interest rates up, while contractionary fiscal policy pulls interest rates down. The rationale behind this relationship is fairly straightforward. When output increases, the price level tends to increase as well. This relationship between the real output and the price level is implicit. According to the theory of money demand, as the price level rises, people demand more money to purchase goods and services. Given that there is no change in the money supply, this increased demand for money leads to an increase in the interest rate. The opposite is the case with contractionary fiscal policy. When output decreases, the price level tends to fall as well. Again, this relationship between the real output and the price level is implicit. According to the theory of money demand, as the price level falls, people demand less money to purchase goods and services. Given that there is no change in the money supply, this decreased demand for money leads to a decrease in the interest rate. This is how fiscal policy affects the interest rate.