Download

1 / 13

130 likes | 226 Views

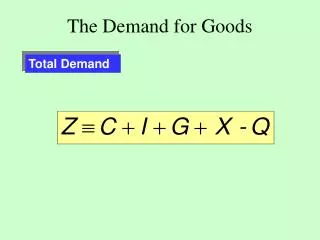

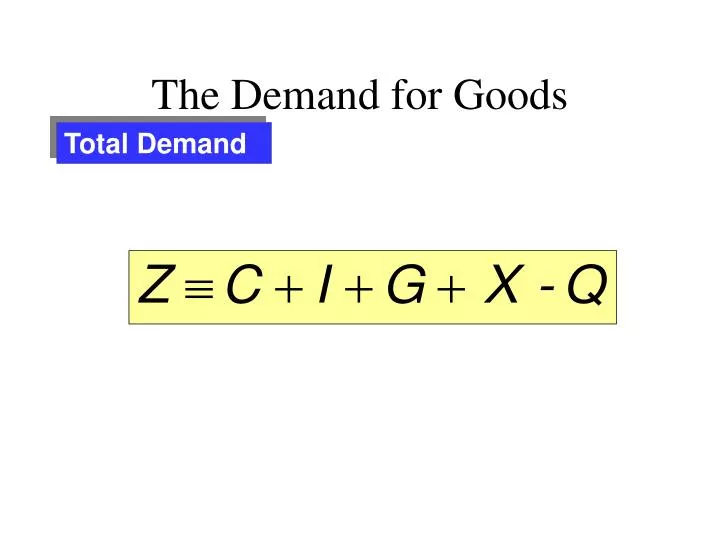

The Demand for Goods. Total Demand. The Demand for Goods. Consumption ( C ). C = C 0 + C 1 Y D C 1 = propensity to consume Change in C from a dollar change in income 0 < C 1 < 1. The Demand for Goods. Consumption ( C ). C = C 0 + C 1 Y D. The Demand for Goods. Investment ( I ).

E N D

The Demand for Goods Total Demand

The Demand for Goods Consumption (C) • C = C0 +C1YD • C1 = propensity to consume • Change in C from a dollar change in income • 0 < C1< 1

The Demand for Goods Consumption (C) • C = C0 + C1YD

The Demand for Goods Investment (I) Investment is an exogenous variable • Exogenous variables • Variables that are assumed to be given and are not explained within the model

The Demand for Goods • Endogenous Variables • Variables that depend on other variables in the model • C is endogenous because it responds to production (Y) C = C0 – C1 (Y – T)

The Demand for Goods Government Spending (G) • G & T are exogenous • no reliable behavioral role for G & T • G & T are determined outside the model

The Determination ofEquilibrium Output Demand for Goods (Z)

The Determination ofEquilibrium Output The Model and Equation Types • Identity Equations • Behavioral Equations • Equilibrium Equations

The Determination ofEquilibrium Output Three Steps to Solving a Model 1) Algebra to confirm the logic 2) Graphs to build the intuition (but we’ll skip the 45° - line diagram) 3) Words to explain the results

The Determination ofEquilibrium Output Finding Equilibrium • Y = supply • Z = Demand = • Y = Z @ equilibrium

The Determination ofEquilibrium Output The Algebra • Dividing both sides by (1 - C1) gives

The Determination ofEquilibrium Output The Algebra: Y=Z

The Determination ofEquilibrium Output Answers • The larger the propensity to consume, C1, the larger the multiplier • A change in autonomous spending will change output more than the direct change in autonomous spending