Download

1 / 13

130 likes | 411 Views

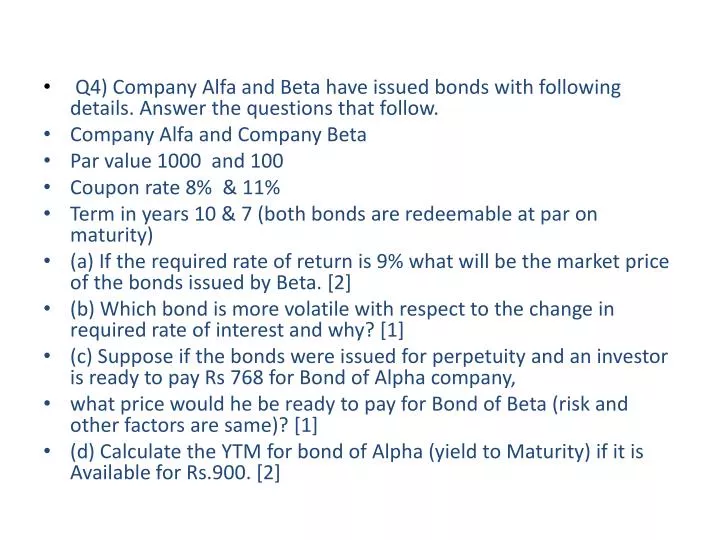

Q4) Company Alfa and Beta have issued bonds with following details. Answer the questions that follow. Company Alfa and Company Beta Par value 1000 and 100 Coupon rate 8% & 11% Term in years 10 & 7 (both bonds are redeemable at par on maturity)

E N D

Q4) Company Alfa and Beta have issued bonds with following details. Answer the questions that follow. • Company Alfa and Company Beta • Par value 1000 and 100 • Coupon rate 8% & 11% • Term in years 10 & 7 (both bonds are redeemable at par on maturity) • (a) If the required rate of return is 9% what will be the market price of the bonds issued by Beta. [2] • (b) Which bond is more volatile with respect to the change in required rate of interest and why? [1] • (c) Suppose if the bonds were issued for perpetuity and an investor is ready to pay Rs 768 for Bond of Alpha company, • what price would he be ready to pay for Bond of Beta (risk and other factors are same)? [1] • (d) Calculate the YTM for bond of Alpha (yield to Maturity) if it is Available for Rs.900. [2]

Price = PVIFA (9%,7yrs) x 11 + PVIF(9%,7yrs) x 100 =5.033 x 11 + 0.547 x 100 = 110.63 • Bond A is more volatile as bonds with low coupon rate and higher maturity period are more volatile • 80/768 = 11/Price => Price = 105.60 • Interpolation using 9% PVIFA(9%,10yrs) x 80 + PVIF(9%,10yrs) x 1000 = 935.44 Interpolation using 10% PVIFA(10%,10yrs) x 80 + PVIF(9%,10yrs) x 1000 = 877.60 (contd….)

9% + (10% - 9%) x 935.44 – 900 = 9.61% 935.44 – 877.60 • Or using direct formula • YTM = 80 + (1000 – 900)/10 0.4 x (1000) + 0.6 x 900 9.57%

Q5) • A person requires Rs.20,000 at the beginning of each year from 2025 to 2029. How much should he deposit at the end of each year from 2015 to 2020, if the interest rate is 12%. The discounted value of Rs.20,000 receivable at the beginning of each year from 2025 to 2029, evaluated as at the beginning of 2024 (or end of 2023) is: Rs.20,000 x PVIFA (12%, 5 years) = Rs.20,000 x 3.605 = Rs.72,100. The discounted value of Rs.72,100 evaluated at the end of 2020 is Rs.72,100 x PVIF (12%, 3 years) = Rs.72,100 x 0.712 = Rs.51,335 If A is the amount deposited at the end of each year from 2015 to 2020 then A x FVIFA (12%, 6 years) = Rs.51,335 A x 8.115 = Rs.51,335 A = Rs.51,335 / 8.115 = Rs.6326

(b) ABCD Corporation has provided the following information. Compute the Upper control limit (UCL) and return point (RP) using Miller and Orr Model. Take 1 year = 365 days [3] • Std deviation of company’s daily cash flow’s Rs.1,00,000. • Annual Yield on Marketable securities is 12%. • It maintains a minimum cash balance of 3,00,000. • Cost of buying or selling marketable security is Rs.1500 per transaction.

3 3 x 1500 x (100000)2 + 3,00,000 • RP = 4 x (0.12 ÷ 365) • = 3,24,660 • UCL = 3 x 3,24,660 – 2 x 3,00,000 • = 3,73,980

Q6) Attempt both the questions that follow • KC corporation requires certain raw material for the factory. The probability distribution of the daily usage rate and the lead time for procurement are given below. (These distributions are independent). Daily usage rate in Lead Time in Tonnes Probability Days Probability 2 0.2 25 0.2 3 0.6 35 0.5 4 0.2 45 0.3 The stockout cost is estimated at Rs 8,000 per tonne and the carrying cost is Rs. 2000 per tonne per year. • Calculate (a) the optimal level of safety stock. [3] • (b)Probability of stock out [1]

Normal Usage = 2(0.2) x 25(0.2) = 50 (0.04) • 2(0.2) x 35(0.5) = 70 (0.10) • 2(0.2) x 45(0.3) = 90 (0.06) • 3(0.6) x 25(0.2) = 75 (0.12) • 3(0.6) x 35(0.5) = 105 (0.30) • 3(0.6) x 45(0.3) = 135 (0.18) • 4(0.2) x 25(0.2) = 100 (0.04) • 4(0.2) x 35(0.5) = 140 (0.10) • 4(0.2) x 45(0.3) = 180 (0.06) • Weighted = 2 + 7 + 5.4 + 9 + 31.5 + 24.3 + 4 + 14 + 10.8 • = 108

The optimum level of Safety Stock = 27The probability of stockout when the safety stock is 27 tons is 6% + 10% = 16%

(b) Price of a company’s share is Rs.80, and the value of growth opportunities is Rs.20, what is the E/P ratio and how much is the earnings per share if market capitalization rate (r) is 15%? [2] EPS/Price = K(1 – PVGO/Price) => EPS/Price = 0.15(1 – 20/80) => E/P = 11.25% E/P = 11.25% and P = 80 EPS = 11.25% x 80 = 9

Q7) Attempt both the question that follow [3+3] • ABC Company is considering relaxing its collection effort. Its sales are Rs.40 million and average collection period is 20 days, its variable costs to sales ratio, V, is 0.80 and cost of capital is 12%, and its bad debt ratio is 5%. The relaxation will push up sales by 5 million and increase average collection period to 40 days and raise the bad debt ratio to 6%. Tax rate is 40%. What will be the effect on residual income if this change is implemented?

RI = [5,000,000 (0.2) – 700,000](0.6) – 0.12[40,000,000(40-20) + 5,000,000 x 40 x 0.80] 360 360 = - 140,000