Download

1 / 20

360 likes | 972 Views

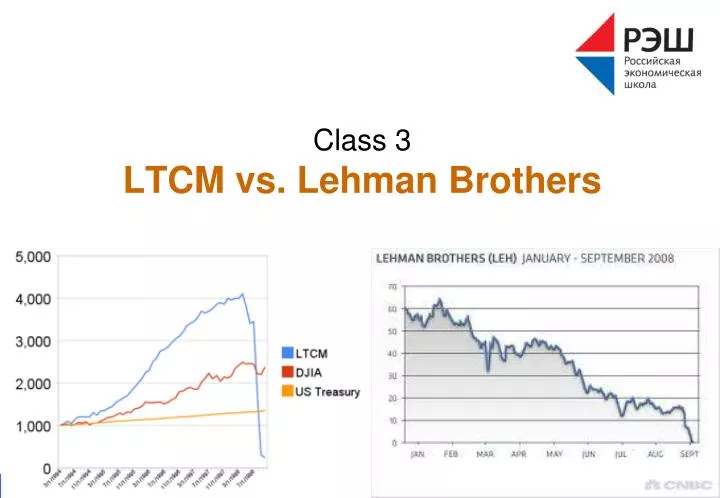

Class 3 LTCM vs. Lehman Brothers. LTCM: When genius failed. Hedge fund Long-Term Capital Management was founded in Feb 1994 by several partners, including John Meriwether from Salomon Brothers Myron Scholes and Bob Merton (Nobel prize, 1997)

E N D

LTCM: When genius failed • Hedge fund Long-Term Capital Management was founded in Feb 1994 by several partners, including • John Meriwether from Salomon Brothers • Myron Scholes and Bob Merton (Nobel prize, 1997) • Charging lofty fees: 2% of assets p.a. + 25% of profits • Starting with $1 bln, it provided net returns over 40% p.a. in 1995 and 1996, • …but lost $4.6 bln in 1998, • …was rescued by the consortium of banks with the aid of Fed • …and folded in early 2000. “LTCM collapsedemonstrates that modern financial risk management techniques do not work”

Was the strategy of LTCM closer to (quasi-)arbitrage or speculation? • Fixed income arbitrage (relative value / convergence trades) • Long off-the-run Treasury bonds, short on-the-run (recently issued and more liquid) Treasuries • The tiny difference of a few basis points is magnified by high leverage • Derivatives arbitrage • Swaps, futures, options, etc. • Merger arbitrage • Buying potential takeover targets • Investing in the sovereign debt • Italy, Russia, etc. • Selling options on S&P500 • Earning low stable income unless the index falls a lot

What were main risks for LTCM? • Market, liquidity and credit risk • What if spreads go up, volatility rises, bond defaults happen,…? • OTC derivatives positions are illiquid • …magnified by high leverage • Turning tiny profits (losses) to attractive returns (huge losses) • Large positions relative to the market • Followed by multiple imitators • Highly sensitive to market-wide liquidity Pickinguppenniesinfrontofa steamroller N. Taleb

How to manage risks for such a big portfolio? • LTCM’s position in January 1, 1998 • Balance sheet assets: $125B • Notional of the derivatives (off balance): over $1.25T • 7,600 positions • 55 counterparties • Own capital: $4.8B • 30 times leverage for balance sheet assets only! • Emergency funding • $230 mln unsecured 3y term loan • $700 mln unsecured line of credit, annual renewal • Equity lock up period for investors: 3 years • In 1997 LTCM earned ‘only’ 17% and returned at the end of the year $2.7 bln to investors (the new ones)

How could LTCM measure market risk? • Historical volatility • Could underestimate risk in a favorable market environment • Cannot fully account for the complicated derivatives positions • Exposure to relevant (secondary) factors • Volatility / liquidity / … • VaR adjusted for liquidity and correlation risk • Would give a rough estimate of the potential losses • Stress testing • Factor push: liquidity, correlations,… • Scenarios taking into account LTCM’s huge market position

LTCM early crisis management • May-Jun 1998: -16% return • SalomonBrothersbondarbitragedeskcloses its portfolio • LTCM liquidates least attractive (most liquid) positions to meet margin calls • Aug 17, 1998: Russian default caused flight to safety and rise in risk premiums • LTCM lost $550 mln in August 21 • YTD losses 40% ($1.8B), capital down to $3.0B • Sep 2, 1998: letter to investors • YTD losses 52% ($2.5B), capital down to $2.3B • 82% of losses in relative value trades

LTCM vs. the market, sep 1998 • Negative rumors • Fund raising fails • Bear Sterns (prime broker) demands more collateral • Some market participants liquidate similar positions • Some bet against LTCM: marking to worst “When it became apparent they were having difficulties, we thought that if they are going to default, we’re going to be short a hell of a lot of volatility. So we’d rather be short at 40 than 30 right? So it was clearly in our interest to mark to as high a volatility as possible. That’s why everybody pushed the volatility against them, which contributed to their demise in the end.” RISK, Oct 99

Should have regulators interfered in such a situation? • Sep 23: consortium of 16 banks (organized by Fed) offered $3.6B for 90% stake in the LTCM • In July 1999 the fund was closed with small profit (10%) • 88% of the original investors made a profit (around 18%) • Avoiding the financial crisis? • LTCM’s default could cause price collapse • …and trigger chain reaction (cross-defaults of counterparties) • Too many important people to bear the losses? • There was an alternative offer in Sep 22: $4B by W.Buffet(together withAIG & Goldman Sachs) for 95% stake in LTCM • What were the long-term consequences of Fed’s assistance?

Lessons of LTCM: was it bad luck or risk management failure? • Risk management at LTCM • Limitations of VaR and model risk • Risk management at LTCM broker (Bear Stearns) • Partner relations vs. low haircut (high leverage) • Risk management at LTCM counterparties • Interaction with a highly leveraged offshore institution • Risk management at other financial institutions • Citi, JP Morgan, Chase also suffered big losses in Aug-Sep 1998 • Regulation / supervision • Moral hazard: will the Fed save all big losers whose default can endanger the whole financial system? • Were LTCM managers and investors ready for such losses?

Lehman Brothers: from a major investment bank to the largest corporate bankruptcy • One of the oldest and most profitable investment banks • Founded in 1850 • Bought by AmEx in 1984, spun off in 1994 through an IPO • Traditional strength: • Fixed income underwriting and trading (39% of income, 59% of assets) • Change of strategy: moving from low-risk brokerage model to high-risk global banking model • Diversified to equity and advisory businesses • …and mortgages (29% of assets) • Market presence • One of the largest dealers in the commercial paper market • Top-10 counterparty in the CDS market ($800B notional)

Position of Lehman at the end of 2007:4th largest US securities firm • 2007 results: record profits $4.2B and revenues $19.3B • Total assets: $691B • $79B of mortgage-related securities incl. $5.3B subprime • Market cap: $35B (down from $60B in Feb 2007) • Equity: $22.5B • Over 1,000 subsidiaries and 28,000 employees • Leverage ratio = Assets/Equity = 30.7 • Funding went mostly via short-term repos ($215B with avg maturity 24d), no retail deposits • Liquidity management: the goal was to provide 12 months of funding under stress • $35B in cash and cash equivalents • $50B of high-quality assets that could be sold or used as collateral

Events: beginning of the end • July 2007: bankruptcy of two hedge funds managed by Bear Stearns • Highly leveraged investment into mortgages • By end-2007 the total losses of banks on MBS exceeded $100B • March 16, 2008: collapse of Bear Stearns • Acquired by JP Morgan at $2 per share (under Fed’s request) • Rumors about insolvency of Lehman using a similar business model (just like in 1998 during LTCM events) • March 18, 2008: earnings announcement by Lehman led to 46% share rise • $489M profit beating expectations ($4.7B losses offset by hedging) • The leverage increased to 31.6 despite $1.9B preferred shares issue • April 1, 2008: another $4B issue of preferred convertibles • Shares went up by 18%

Events: heading towards failure • April 8, 2008: David Einhorn (Greenlight Capital hedge fund) announced shorting Lehman • Lehman’s write-downs on mortgages should be larger • High leverage makes them vulnerable (they need 3-5 times more capital) • June 2, 2008: S&P downgraded Lehman’s rating from A+ to A (together with Merril Lynch and Morgan Stanley) • June 9, 2008: Lehman announced first ever quarterly loss as a public company, $2.8B • Total losses $17B partly offset by $7.5B hedging gains and asset sales • Leverage went down to 25 • Announcing sales of $6B stocks at 15% discount to market price • June 12, 2008: CFO and President were fired

Events: the end • August 2008: Lehman laid off 1,500 employees (6% workforce) • Sep 7, 2008: the gvt seized control over Freddy Mac & Fannie Mae • Sep 10, 2008: Lehman announced a second quarterly loss $3.9B • …along with intention to sell of most of its investment mgt business • This led to credit rating downgrade and stock price plunge • Sep 13, 2008: the Fed organized a meeting of bankers to discuss the future of Lehman • The gvt refused to bail out them, encouraged private buyout • Before that, Lehman tried to engage the Korea Development Bank, the Bank of America and Barclays, but with no success • Sep 15, 2008: Lehman filed for bankruptcy • The international offices were ordered to transfer money to NY, but chose to file for bankruptcy or liquidation • Later Lehman’s assets were sold to Barclays, Nomura, …

Consequences: the ‘perfect storm’ in the financial markets • The largest bankruptcy in the US history • Affecting company’s employees, counterparties, investors,… • Leading to chain reaction • Sep 15: BoA acquired Merrill Lynch for $50B • Sep 16: Fed announced $85B rescue package for AIG • Sep 22: Goldman Sachs & Morgan Stanley convert into bank holding companies • Dollar fell • Flight from corporate securities to Treasuries • CDS spreads widened • Money market funds faced heavy redemptions • Global equity markets lost trillions of dollars

LTCM vs. LB: what is the difference? • What was the main reason of the failure? • LB is a corporate governance case! • Using Repo 105 program, LB could hide its true leverage • LB accounted for repos as asset disposals (hiding the obligation to buy back the collateral) • $50B in sep08, reducing leverage from 13.9 to 12.1 • Why didn’t the Fed save LB like it saved LTCM?