Download

1 / 11

110 likes | 250 Views

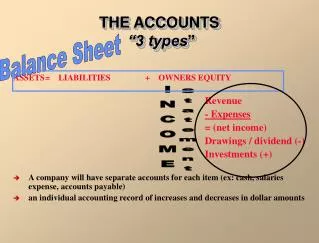

Chapter 3 Adjusting the Accounts. Part 1 of 3. Concepts to Be aware of:. Time Period Concept A business lifecycle can be divided into artificial time periods. Time periods less than a yr. Interim Periods Revenue Recognition Service Sector – earned when service is preformed

E N D

Chapter 3Adjusting the Accounts Part 1 of 3

Concepts to Be aware of: Time Period Concept • A business lifecycle can be divided into artificial time periods. • Time periods less than a yr. Interim Periods Revenue Recognition • Service Sector – earned when service is preformed • Manufacturing Sector – earned when goods are delivered

Revenues earned this month expenses incurred in earning the revenue are offset against.... Cont.... Matching Principle • dictates that efforts (expenses) be matched with accomplishments (revenues). Why is this important?

Accrual vs. Cash Accounting Accrual Basis of Accounting • Follows all GAAP Principles • All revenues and expenses are accounted for when they happen. Cash Basis of Accounting • Are only recorded when cash is received (revenue) or paid (expenses) Example Work: E3-2

Why use adjustments? • Adjusting entries are needed to ensure that revenue recognition and matching principle GAAP concepts are taken into account. • Keeps statements up-to-date. • Some accounts are allowed to become “inaccurate” between fiscal periods. • Adjustments help ensure that statements are brought up-to-date.

Prepayments Prepaid Expenses: • Expenses that are paid before they are consumed • These are considered an ASSETS (WHY?) • Adjusting Entry for Prepaid supplies: Prepaid Supplies Expense XXX Supplies XXX NOTICE: we are not using the cash account!

Example of Supplies Exp • A physical inventory count is done we found that only $1500 worth of supplies are left, when on the books it is recorded at $2000. Supplies Expense $500 Supplies $500

Example for Insurance: Insurance was purchased on Sept 1 for $1800, and the end of the fiscal year is Dec 31. How do we figure out how much we have used up for the fiscal year?

Prepayments cont... Unearned Revenue: • Revenues that are paid for before the work is actually completed. • These are considered a LIABILITY • Adjustment Entry for Unearned Rev: Unearned Rev. XXX Service Rev. XXX NOTICE: we are not using the cash account!

Work for this Section Brief Exercise: • 3-3, 3-4 Exercise: • 3-3