Download

1 / 16

180 likes | 356 Views

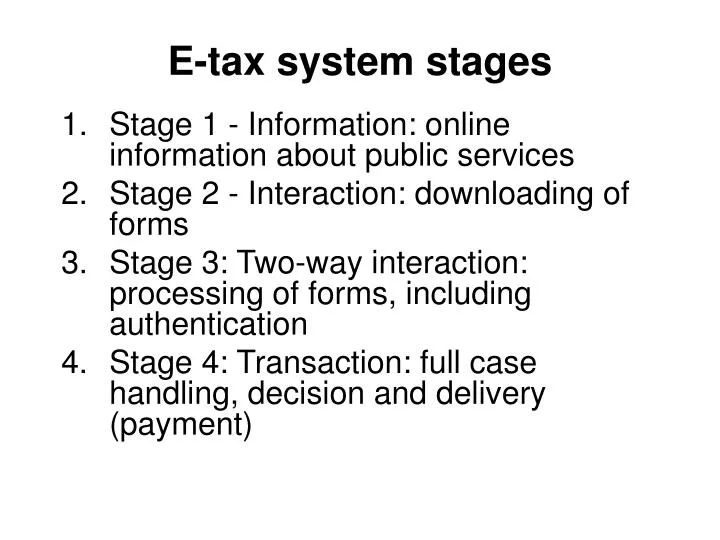

E-tax system stages. Stage 1 - Information: online information about public services Stage 2 - Interaction: downloading of forms Stage 3: Two-way interaction: processing of forms, including authentication Stage 4: Transaction: full case handling, decision and delivery (payment).

E N D

E-tax system stages Stage 1 - Information: online information about public services Stage 2 - Interaction: downloading of forms Stage 3: Two-way interaction: processing of forms, including authentication Stage 4: Transaction: full case handling, decision and delivery (payment)

E-tax system stages Latvia. Poland, Luxembourg. Hungary. Austria, Belgium, Cyprus, Czech Republic, Denmark, Estonia, Finland, France, Germany, Greece, Ireland, Italy, Lithuania, Malta, Netherlands, Portugal, Slovakia, Slovenia, Spain, Sweden, United Kingdom,

E-tax system (Poland) Information and forms to download. In April 2005 the Ministry of Finance unveiled plans for the introduction of e-tax filing services. The introduction of interactive and transactional tax e-services for corporate taxpayers is due to start in 2006, while for citizens the system is to be fully operational by the end of 2012.

E-tax system (Latvia) The Electronic Declaration System is designed to enable Latvian taxpayers to submit tax returns, declarations and other documents via Internet by filling in appropriate web form or by transferring XML file containing corresponding data. PIN codes and passwords are used to authenticate users, and information exchange is secured by SSL protocol. All the necessary checks of declarations data are performed and users are informed of the results of these checks online and by e-mail. 50 different types of declarations can technically be submitted via Internet, but as the regulations concerning the procedure of elaboration, processing, storage and circulation of electronic documents have not yet been adopted, these documents still have to be submitted also in paper form and the Electronic Declaration System is still in demo version. It is planned that it will become fully functional and transactional in 2005.

E-tax system (Slovenia) The eDavki (eTaxes) portal enables all legal and natural persons to conduct business with the Tax Office electronically. Since 2004, taxpayers can use it to submit their income tax returns online. 23,792 taxpayers submitted their income tax returns online in 2005, 42 % more than in 2004.

E-tax system (Slovenia) The Fisco Online service allows users to make income tax declarations and payments online.

E-tax system (Lithuania) 2005 17 per cent of the population used this service 2006 almost 46 per cent adult population submitted their declarations by EDS

Technical solution the subsystem for designing and creating declaration forms; the subsystem for recognizing scanned documents; the subsystem for recognition of scanned documents also has certain modules for the exportation of documents; the subsystem for archives where digital originals of documents are stored; the subsystem for integration; the module for administrating EDS forms; the external portal (EDS web site); the internal portal; the portal of accounts.

EDS operational possibilities Sending a ready-made file by EDS portal. Completion of declarations on-line in the EDS portal. Sending of a ready-made file by e-mail. Submission of a ready-made file in a data carrier.

Submission of declarations and notification to the taxpayers Rejected -some errors Submitted -i.e. there were no errors found in the declaration and a fact of submission of a declaration is registered in EDS. Later, when the analysis of data is completed in the system, this status will be changedto “Accepted”, “Accepted with errors” or “Not accepted”. Submitted, waiting for verifying of other declarations Accepted Accepted with errors Not accepted Cancelled -critical errors (indicated period is incorrect; sums indicated in fields have been calculated wrongly; incorrect codes are indicated)

The prospects of Electronics Declaration System installation of a web-service for the submission of e-form declarations - This prospective service would be assigned for large legal entities since the number of their submitted declarations can amount to hundreds of thousands of pages. Due to the success of this service, not only declarations but also declaration data sets will be produced. In order to make this system accessible to various social groups, it is indicated that EDS system should be adapted for use by those who are handicapped, as well as national minorities (speakers of other languages) by2008 The procedure of the STI password provision will be expanded for more convenient identification of the EDS users. E-signature identification technology could be incorporated in the process of user identification. the identification of foreigner nationals resident in Lithuania. The united system of identification should be established.

Taxation Principle of neutrality Principle of efficiency Principle of simplicity Principle of effectiveness Principle of fairness Principle of flexibility