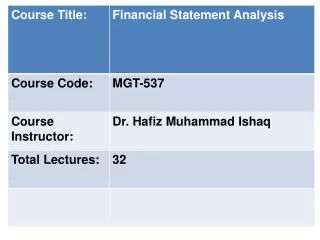

Download

1 / 40

410 likes | 597 Views

Previous Lecture. Uncollectible Accounts Reflecting Uncollectible Accounts in the Financial Statements The Allowance for Doubtful Accounts Writing Off an Uncollectible Account Receivable Recovery of an Account Receivable Previously Written Off. Previous Lecture.

E N D

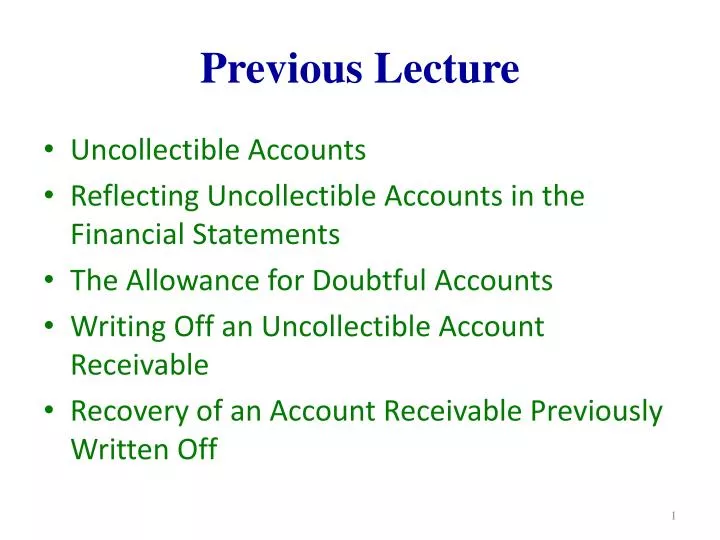

Previous Lecture • Uncollectible Accounts • Reflecting Uncollectible Accounts in the Financial Statements • The Allowance for Doubtful Accounts • Writing Off an Uncollectible Account Receivable • Recovery of an Account Receivable Previously Written Off

Previous Lecture • Monthly Estimates of Credit Losses • Estimating Credit Losses — The “Balance Sheet” Approach • An Alternative Approach to Estimating Credit Losses • Direct Write-Off Method • Income Tax Regulations and Financial Reporting

Previous Lecture • Internal Controls for Receivable • Management of Accounts Receivable • Ways to Minimize Amounts in Accounts Receivable • Evaluating the Quality of Accounts Receivable

SAFWAY, INC Having the right merchandise available at the right time and in the right place is critically important to all companies that sell products to their customers. These business include chain stores such as grocery store, drugstores, and department stores.

Consider Safeway Having 1700 stores nationwide When Customer shop at Safeway, theyexpect to find the items they want in stock and ready to purchase. If not, then they will find other place for shop. For this purpose Safeway store must stock more than 10,000 products Controlling such a diverse selection is big challenge in highly competitive environment

Goods ownedand held for saleto customers Current asset Inventory Defined Inventory

BALANCE SHEET Current assets: Inventory $ $ INCOME STATEMENT Revenue $ Cost of goods sold Gross profit Expenses Net income The Flow of Inventory Costs As purchase costs (or manufacturing costs) are incurred as goods are sold

The Flow of Inventory Costs In a perpetual inventory system, inventory entries parallel the flow of costs.

Which Unit Did We Sell? When identical units of inventory have different unit costs, a question naturally arises as to which of these costs should be used in recording a sale of inventory.

A separate subsidiary account is maintained for each item in inventory. Inventory Subsidiary Ledger How can we determine the unit cost for the Sept. 10 sale?

Average cost Specific identification FIFO LIFO Inventory Cost Flows We use one of these inventory valuation methods to determine cost of inventory sold.

Information for the Following Inventory Examples The Bike Company (TBC)

Specific Identification When a unitis sold, the specific cost of the unit sold is added to cost of goods sold.

Continue Specific Identification – Example On August 14, TBC sold 20 bikes for $130 each. Nine bikes originally cost $91 and 11 bikes originally cost $106.

Continue Specific Identification – Example The Cost of Goods Sold for the August 14 sale is $1,985, leaving $515 and 5 units in inventory. Let’s look at the entries for the Aug. 14 sale.

Retail Cost Continue Specific Identification – Example A similar entry ismade after each sale.

Continue Specific Identification – Example Cost of Goods Sold for August 31 = $2,610 Additional purchases were made on August 17 and 28. Costs associated with sales on August 31 were as follows: 1 @ $91, 3 @ $106, 15 @ $115, & 4 @ $119.

Specific Identification – Example Income Statement COGS = $4,595 Balance Sheet Inventory = $1,395

Not really. Specific identification is hard to use when we sell a lot of inventory that has lots of different costs. Since specific identification is so easy, can’t we use it all the time?

Cost of Goods Available for Sale Units on hand on the date of sale Average-Cost Method When a unit is sold,theaverage cost of each unitin inventory is assigned to costof goods sold. ÷

Continue Average-Cost Method – Example The average cost per unit must be computed prior to each sale. $100 = $2,500 25 On August 14, TBC sold 20 bikes for $130 each.

Continue Average-Cost Method – Example The average cost per unit is $100. $100 = $2,500 25 Let’s look at the entries for the Aug. 14 sale.

Retail Cost Continue Average-Cost Method – Example A similar entry ismade after each sale.

Continue Average-Cost Method – Example Additional purchases were made on August 17 and August 28. On August 31, an additional 23 units were sold.

Average-Cost Method – Example $114 = $3,990 35

Average-Cost Method – Example The average cost per unit is $114. $114 = $3,990 35

Income Statement COGS = $4,622 Average-Cost Method – Example Balance Sheet Inventory = $1,368 $114 × 12 = $1,368

Oldest Costs Recent Costs First-In, First-Out Method (FIFO) Costs of Goods Sold Ending Inventory

Continue FIFO – Example The Cost of Goods Sold for the August 14 sale is $1,970, leaving $530 and 5 units in inventory. On August 14, TBC sold 20 bikes for $130 each.

Retail Cost Continue FIFO – Example A similar entry ismade after each sale.

Continue FIFO – Example Additional purchases were made on Aug. 17 and Aug. 28. On August 31, an additional 23 units were sold. Cost of Goods Sold for August 31 = $2,600

FIFO – Example Income Statement COGS = $4,570 Balance Sheet Inventory = $1,420

Recent Costs Oldest Costs Last-In, First-Out Method (LIFO) Costs of Goods Sold Ending Inventory

Continue LIFO – Example The Cost of Goods Sold for the August 14 sale is $2,045, leaving $455 and 5 units in inventory. On August 14, TBC sold 20 bikes for $130 each.

Retail Cost Continue LIFO – Example A similar entry ismade after each sale.

Continue LIFO – Example Additional purchases were made on Aug. 17 and Aug. 28. On Aug. 31, an additional 23 units were sold. Cost of Goods Sold for August 31 = $2,685

LIFO – Example Income Statement COGS = $4,730 Balance Sheet Inventory = $1,260