Download

1 / 9

180 likes | 398 Views

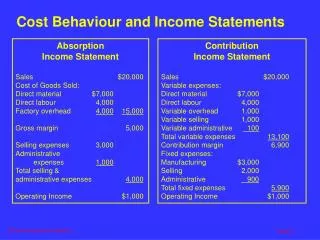

Measurement of Cost Behaviour. 3. $. Volume. $. Volume. $. Volume. Measurement of Cost Behavior. Cost Driver an activity which influences a cost Relevant Range range over which we can assume that the cost behavior is linear Variable Costs

E N D

$ Volume $ Volume $ Volume Measurement of Cost Behavior Cost Driver • an activity which influences a cost Relevant Range • range over which we can assume that the cost behavior is linear Variable Costs • vary in proportion to changes in their cost driver Fixed Costs • are not affected by changes in the cost driver

Variations in Cost Behaviour • Step Costs • change abruptly at intervals of activity because the resources and their costs come in indivisible chunks • supervisory salaries • Mixed Costs • contain both variable and fixed cost elements • e.g. maintenance costs $ Volume $ Volume

Management’s Influence on Cost Functions Capacity Costs • fixed costs related to being able to achieve a desired level of production or service • setting capacity is very important if long-run demand fluctuates Committed Fixed Costs • arise from the possession of facilities, equipment, and a basic organization • large, indivisible chunks of cost that the organization is obligated to incur and usually would not consider avoiding • mortgage, lease payments, property taxes, insurance, salaries of key personnel • committed fixed costs can only be changed by changing the basic philosophy, scale or scope of the organization's operations

Management’s Influence on Costs Functions II Discretionary Fixed Costs • each planning period, management will determine how much to spend • advertising, promotion, research and development, employee training • the amount of spending may vary, but only because management has decided to spend more or less • management can influence spending on these costs in the short run

Measuring Cost Behaviour Cost Function • algebraic equation of the cost and its cost driver • linear cost function is as follows: Y = F + VX where • F is the intercept of the vertical axis or the fixed cost • V is the slope or the variable cost per unit of activity Total Maintenance Costs per month = fixed cost per month + variable cost per unit = $10,000 + $5.00 per unit Criteria for Choosing A Cost Function • Use activity analysis to determine which cost driver best explains how the cost behaves • Economic plausibility (it must make sense that X causes Y) • Reliability (the estimates derived by the cost equation must conform with actually observed costs)

Methods of Measuring Cost Functions Engineering Analysis • systematic review of costs based on past experience Account Analysis • review of accounting records and the subjective determination of cost behavior patterns High-Low Analysis • use of simple linear algebra to determine variable and fixed costs • may yield unreliable results Visual Fit Analysis • fit a representative line to the data as shown in a scatter diagram Regression Analysis • using mathematical formula, determine the cost equation which best fits the data • may be simple least squares regression with one X variable or multiple least squares regression with more than one X variable • enables user to measure the "quality" of the predictive equation

High-Low Approach to Cost Analysis Facilities Maintenance Department Costs Equation: Y = F + VX Variable cost = change in cost / change in volume = $30,000 / 3,700 = $8.108 per patient-day Fixed cost = total mixed cost - variable cost = $47,000 - ($8.108 x 4,900) = $47,000 - $39,730 = $7,270 per month Maintenance Costs = $7,270 + $8.108 per patient-day x x x x x x x x Number of Patient-Days

Regression Analysis Check for Economic Plausibility • Does it make sense that X and Y are related? Plot the data • to see if basic relationship is linear and identify "outliers" Generate Regression Output Constant $9,329 Std Error of Y Estimate $2,145 Observations 12 R-Squared 0.954 Degrees of Freedom 10 X Coefficient(s) $6.95 Std Error of Coefficient 0.479 Interpret Regression Output • R-squared (R2) varies between 0 and 1 • The closer to R2 is to 1 the more X explains the changes in Y • Standard error of Y estimate and standard error of X coefficient(s) can be used to set confidence intervals for the cost function estimates and the predicted value of the variable cost per unit