Download

1 / 13

520 likes | 2.84k Views

CREDIT CREATION BY COMMERCIAL BANKS. MEANING OF COMMERCIAL BANK: A COMMERCIAL BANK IS THAT FINANCIAL INSTITUTION WHICH ACCEPTS DEPOSITS FROM THE PEOPLE AND GIVES LOANS FOR THE PURPOSE OF CONSUMPTION OR INVESTMENT MEANING OF CREDIT :

E N D

MEANING OF COMMERCIAL BANK: • A COMMERCIAL BANK IS THAT FINANCIAL INSTITUTION WHICH ACCEPTS DEPOSITS FROM THE PEOPLE AND GIVES LOANS FOR THE PURPOSE OF CONSUMPTION OR INVESTMENT • MEANING OF CREDIT: • A contractual agreement in which a borrower receives something of value now and agrees to repay the lender at some later date

Types of BANKS • There are various types of banks which operate in our country to meet the financial requirements of different categories of people. • Central Bank (RBI, in India) • Development Bank • Commercial Bank • Co-operative Bank • Specialized Banks(NABARD) • Foreign Banks(EXIM Bank)

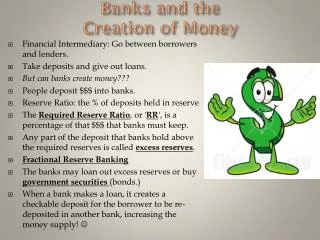

Credit Creation of Commercial Bank • The commercial banks are the second most important sources of money supply. The money that commercial banks supply is called credit creation. • The process of ‘Credit Creation’ begins with banks lending money out of primary deposits. Primary deposits are those deposits which are deposited in banks. • After maintaining the required reserves, the bank can lend the remaining portion of primary deposits. Here bank’s lend the money and the process of credit creation starts.

Process of Credit Creation • Suppose there are a number of commercial Banks in the Banking system-Bank 1, Bank 2, Bank 3, & so on. • To begin with let us suppose that an individual “A” makes a deposit of Rs.100 in Bank 1. Bank “1” is required to maintain a cash reserve Requirement of 5% which is decided by RBI’s monetary Policy from the deposits made by ‘A’ Bank ‘1’ is required to maintain a cash reserve of Rs.5(5% of 100). The bank has now lendable funds of Rs.95(100-5). Lets the Bank “1” lends Rs.95 to a borrower; say B. The method of lending is the same that is bank 1 opens an account in the name of the borrower cheque for the loan amount. At the end of the process of deposits & lending, the balance sheet of bank read

Now suppose that money B borrowed from bank “1” is paid to individual “C” in settlement of his past debts. The individual “C” deposits the money in his bank say Bank “2”. Now bank 2 carries out its banking transaction. It keeps a cash reserve to the extend of 5% that is Rs.4.75(5% of 95) and lend Rs.90.25 to a borrower D. at the end of the process the balance sheet of Bank 2 will be look like:- Balance sheet of Bank “2”

The amount advanced to D will return ultimately to the banking system, as described in case of B and the process of deposits and credit creation will continue untill the reserve with the bank is reduced to zero The combined balance sheet of Banks

Deposit Multiplier • The total deposit created by the commercial banks constitutes the money supply by the banks. Credit creation of commercial banks depends upon deposit multiplier. • Deposit multiplier= 1/CRR (5%) = 1/0.05=20 In this example primary deposit is Rs.100/- deposit multilier is 20. hence total credit creation of commercial banks equal to 100×20=2,000.

Reserve Bank of India • The reserve bank of india established in April 1935 on the recommendation of the Hilton Young Commission. • It was nationalized in the year 1949. Function of Reserve bank of India. • Bank of Issue • Banker to Government • Banker’s Bank & lender of last resort. • Controller of Credit

Reserve Bank of India- Credit Control Types of credit control: • Quantitative methods. • Bank Rate • Open market operation • CRR(cash reserve ratio) • SLR(Statutory Liquidity Ratio)

II. Qualitative Methods • Fixation of Margin Requirement • Rationing of credit • Moral suasion • Direct action • Guidelines

THANK YOU Ravi Sohpaul PGT.Economics KV. NO.1 Srinagar