Download

1 / 29

290 likes | 416 Views

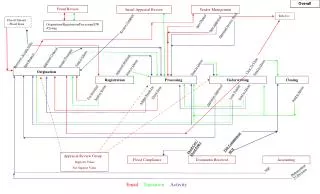

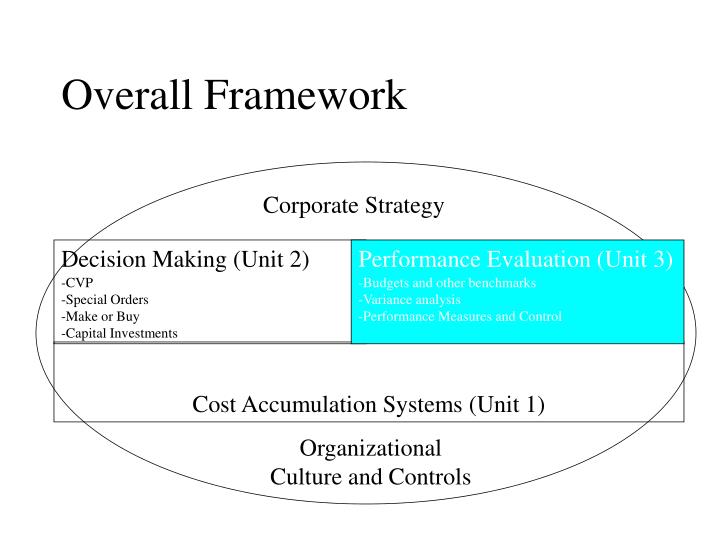

Overall Framework. Corporate Strategy. Decision Making (Unit 2) -CVP -Special Orders -Make or Buy -Capital Investments. Performance Evaluation (Unit 3) -Budgets and other benchmarks -Variance analysis -Performance Measures and Control. Cost Accumulation Systems (Unit 1).

E N D

Overall Framework Corporate Strategy Decision Making (Unit 2) -CVP -Special Orders -Make or Buy -Capital Investments Performance Evaluation (Unit 3) -Budgets and other benchmarks -Variance analysis -Performance Measures and Control Cost Accumulation Systems (Unit 1) Organizational Culture and Controls

Budgeting and Variance Analysis • Terminology (today) • Standards (today) • Master Budgets (today) • Flexible Budgets (today and Thursday) • Variances (Thursday and beyond) • Production Variances • Sales Variances

Some Critical Terms • Standards • An expected, or planned, amount of something • The standard price for a raw material is what we expect to pay our suppliers per unit of the material • The standard rate for direct labor is what we expect to pay our workers on an hourly basis • The standard machine time per unit is how long we expect each part to take on a given machine • The standard market share is the percent of the market that we expect our products to capture • We eventually “dollarize” most standards into an amount per unit of our product

Some Critical Terms • Master Budget • An aggregate representation of the firm’s expected activity over some future time period • Calculated at one activity level (the most likely) for sales and production • Assumes all activity occurs at standard expectations (selling, producing, capital spending, cash collecting, etc.)

Some Critical Terms • Flexible Budget • Imagine a master budget set for production of 1,000 units. • Imagine that actual production was 1,100 units because of high demand • Imagine comparing master budgeted materials costs to actual materials costs • Would the manager look good?

Some Critical Terms • Flexible Budget • The flexible budget adapts the master budget based on actual activity levels (in sales and production) • The flexible budget depicts what the master budget would have looked like had we accurately estimated activity levels. • The flexible budget is still based on standards

Some Critical Terms • Variance Analysis • The comparison of actual activity and resource consumption to expected amounts • VERY FEW such calculations are appropriately done using master budget information • ALMOST ALL such calculations are appropriately done using FLEXIBLE budget information

Determination of Standards • Standards are (per unit) expected levels of resource consumption • “Ideal” standards assume 100% utilization and perfect implementation • “Currently attainable” standards set at achievable work pace • include breaks, “normal” mistakes

Sources of Standards • Activity analysis • Historical data • Benchmarking • Market information • quality expectations • target costs • Can be mandated or negotiated

Types of Standards • Direct Materials • Usage: units of RM per unit of product • Price: cost of RM per unit of product • Direct Labor • Usage: labor hours per unit of product • Rate: labor cost per unit of product • Mix of materials inputs • Mix of labor inputs

Types of Standards • Variable Overhead • Usage: Amount of VOH charged per unit of product • Rate: VOH PDOR • Some VOH items, like electricity, may be more traceable than others • Budgeted Fixed Overhead • Fixed Overhead PDOR

Types of Standards • Standards also exist for the selling side of the business • Prices and volumes • Sales mix • Market share • Market size

Standard Cost Card Resource Quantity Unit Cost Subtotal Total Direct Materials X 4 lb $25/lb Y 1 lb 40/lb Direct Labor 5 DLH $40/hr VOH 5 DLH $12/DLH FOH 5 DLH $24/DLH

Why Budget? • Planning • Helps identify resource requirements • Coordinating • Communication tool across company units • Motivation • Targets for performance • Evaluation • Compare actual to expected performance

Strategic Planning External Scan Internal Scan Threats and Opportunities Strengths and Weaknesses Best Opportunities Strategy

Overall Budget Framework Strategic Goals Long Term Objectives Long Term Plan Capital Budget Short Term Objectives Master Budget Internal Controls Operations

Budget Process Timeline Ongoing Negotiations • Guidelines from top management • Initial proposal: bottom or top? • Factors: volume changes, new products • Review, revise, review, approve (iterative) Year Being Budgeted June Nov Jan Dec

Master Budget Framework Strategic Objectives (Short- and Long-Term Capital Budget Cash Collections Sales Forecasts Sales Budget Production Budget Administrative Budgets Direct Labor Direct Mats. Mfg. OH Sales & Mktg. Res. & Dev. Corp. OH Cash Budget

Purposes of Specific Budgets • Capital Budget • Ensure funding for long-term projects • Ensure capacity requirements met • Production Budget • Ensure demand and inventory goals met • Materials • Ensure required materials available • Allow planning for purchasing contracts

Purposes of Specific Budgets • Labor Budget • Ensure labor capacity adequate • Allow for informed choices among alternatives (e.g., overtime versus new hires) • Cash Budget • Ensure enough cash for all activities • Avoid emergency borrowing • Plan investment of excess cash

Approaches to Budgeting • Incremental • Ratchet up (or down) from previous year • Zero-based • Budget as if current operation did not exist • Activity-based • Budget based on activity transactions

Approaches to Budgeting • Unilateral • Top management sets budget • Top-Down • Top management makes initial proposal, negotiation occurs • Bottom-Up • Operations-level employees make initial proposal, negotiation occurs

Budget Target Level • Assume you are a worker and you can comfortably complete 100 units per day. At what level would you like your daily budget to be set? • 60 90 110 150 • Goal congruence

Budget Shenanigans • Budgetary Slack • Expect 100, budget for 125 (expenses) • Expect 125, budget for 100 (sales) • “Spending” the Budget • Budget for 125, spend 110, 15 left • Spend it or lose it (?)

Flexible Budgets • Master Budget Process is “Static” • One level of activity • Can show how well firm is meeting production goals • Flexible budgets are “dynamic” • “Flex” with level of activity • Can help show how well the firm is controlling its costs

Flexible Budget Preparation • Determine relevant activity range • Separate costs by behavior pattern • Prepare Master Budget at expected activity level • Prepare Flexible Budget at actual activity level • What MB would have looked like had the expected level been the actual level

Example Flexible Budget • Master Budget at 8,000 units Revenues @ $21 $168,000 Materials @ 1.6 12,800 Labor @ 7 56,000 VOH @ 3.15 25,200 Total VC @ 11.75 94,000 CM @ 9.25 $74,000

Example Flexible Budget • What if we actually sell 7,000? Actual Sales 7,000 Revenues @ $21 Materials @ 1.6 Labor @ 7 VOH @ 3.15 Total VC @ 11.75 CM @ 9.25

What About Fixed Costs? • Not expected to change across activity levels • Reasons for inclusion: • Overall performance evaluation • Product costing • Profit planning (must remember to cover FC) • Use amount of allocation base at most likely activity level to determine PDORs